USD/JPY rises above July 2024 high adding to intervention risks

USD/JPY: Intervention risk & US Supreme Court ruling in focus

The US dollar has continued to strengthen overnight hitting fresh highs against the yen. USD/JPY has extended its upward trend after breaking above the high from July 2024 at 161.95. The weaker yen has drawn more concern from Japanese policymakers overnight. Finance Minister Katayama stated that Japan will respond to FX appropriately at any time. She added that Japan confirmed with the US that bold actions are included as an option, and that it all comes down to taking the right FX steps when needed. While it continues to signal that Japan is prepared to intervene again to support the yen, the comments fall short of strongly signalling that intervention is imminent based on past rhetoric. It follows comments as well from Chief Cabinet Secretary Minoru Kihara overnight who stated that Japan will take appropriate action on foreign exchange as required. The current fundamental backdrop is challenging for Japan to push back against the move higher in USD/JPY given the Fed’s hawkish policy shift has lifted both US yields and the US dollar. As we saw back in late April/early May, record intervention from Japan only briefly strengthened the yen but failed to reverse the weakening trend for long. As a result, Japan may maybe more tolerant of yen weakness in the near-term as long as the pace remains gradual. At the same time, recent yen weakness has been mainly focused against the US dollar while other yen crosses have remained relatively stable. The heightened risk of intervention has been helping to at least slow the pace of yen weakness.

The US dollar continues to trade on a stronger footing since the Fed’s last policy update. It avoided one potential banana skin yesterday after the US Supreme Court denied an appeal by the Trump administration against a lower court ruling allowing Fed Governor Lisa Cook to stay in office while litigation continues over the President’s attempt to dismiss ger on the basis of alleged mortgage fraud. The ruling narrowly sided in Fed governor Cook’s favour by 5-4 votes helping to protect the Fed’s monetary policy independence. The Court ruled that Governor Cook had not been afforded the “notice and some opportunity to respond” to the charges that could be inferred from the statute that created the Federal Reserve. However, it has been reported that the Department of Justice could still have another go at trying to unseat governor Cook by putting in place some form of process for her to answer the charges made against her. Chief Justice Roberts did emphasize that the Federal Reserve is a “special arrangement sanctioned by history” which requires a substantial cause for dismissal.

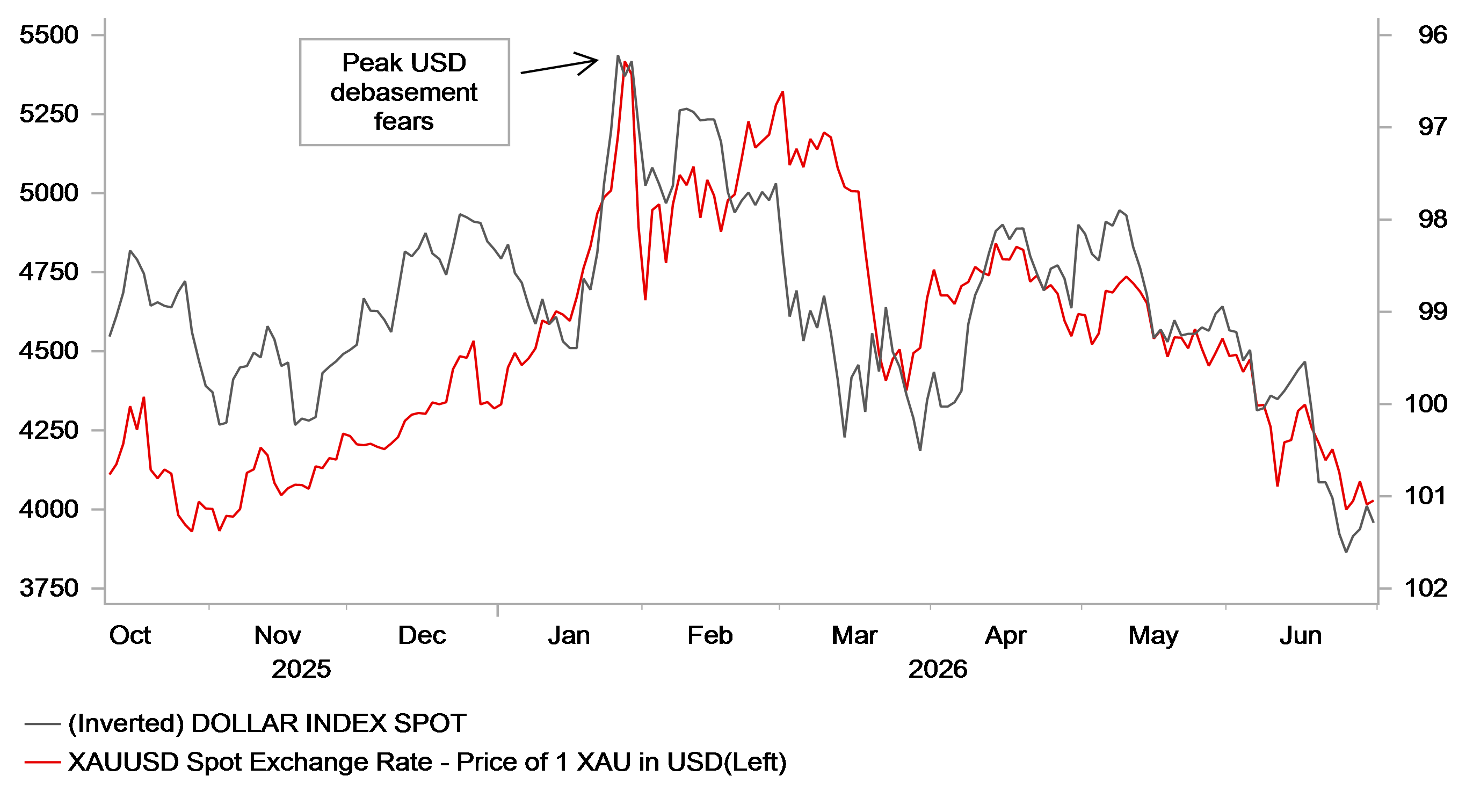

The Supreme Court ruling adds to the recent hawkish rhetoric from new Fed Chair Kevin Warsh who emphasized the need to meet the price stability part of the Fed’s dual mandate at his first press conference. Together the developments have helped to dampen investor concerns over threats to the Fed’s independence under President Trump; and have triggered a further reversal of popular US dollar debasement trades from earlier this year. After hitting a high of USD5,595.5/ounce at the end of January, the price of gold has fallen back below USD4,000/ounce over the past week having lost around 30% of its value over the last five months.

USD DEBASEMENT FEARS HAVE EASED

Source: Bloomberg, Macrobond & MUFG Research

EUR: Slowing cyclical growth momentum remains headwind for euro

The euro continues to trade close to recent lows against the US dollar and pound. Cable is threatening to break out of the bottom of the 1.1400 to 1.1800 trading range that has been in place over the past year, while EUR/GBP is similarly moving closer to the bottom of the narrower trading range 0.8600 and 0.8800 that has held over the same period. The euro has come more selling pressure in recent months as evidence has been building over the negative impact from the energy price shock on European economies. Economic data surprises from the euro have been surprising on the downside on balance since April although the worst point for negative data surprises has now passed in late May.

In contrast, the US economic data surprise index recently rose to its highest level in almost three years reinforcing the impression among market participants that the US economy is proving resilient in the face of the energy price shock. The release at the end of last week of soft US consumer spending for Q1 has cast some doubt on that view helping to dampen the US dollar’s upward momentum. Softer growth in Europe in Q2 remains a headwind for euro performance in the near-term although if energy prices stabilize at lower levels going it will help to encourage a pick-up in cyclical momentum later this year providing more support for the euro.

Softer growth and lower inflation are both encouraging market participants to scale back ECB rate hike expectations. The euro-zone rate market is fully pricing in one more hike by year end. ECB Chief Economist Philip Lane acknowledged that the oil market has moved “quite a bit” since their last policy meeting but highlighted that oil prices are still above pre-war levels in 2027 and 2028 with inventory restocking helping to keep higher oil prices. When asked about the June rate hike decision he said it was “not a tiebreaker or insurance hike”. He is watching closely to assess second-round inflation effects which are probably going to take some time, while stating that they won’t be boxed into a rate path. We still expect one final hike in September, but lower energy prices are creating more room for the ECB to leave rates on hold.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

DE | 08:55 | German Unemployment Rate | (Jun) | 6.3% | 6.3% | !! |

DE | 08:55 | German Unemployment Change | (Jun) | 7K | -12K | !! |

EU | 10:40 | ECB's Schnabel Speaks | - | - | - | !! |

GB | 11:40 | BoE Breeden Speaks | - | - | - | ! |

EU | 12:30 | ECB's Lane Speaks | - | - | - | !! |

DE | 13:00 | German CPI (YoY) | (Jun) | 2.6% | 2.6% | !! |

CA | 13:30 | GDP (MoM) | (Apr) | 0.4% | -0.1% | !! |

EU | 14:30 | ECB's Lane Speaks | - | - | - | !! |

US | 14:45 | Chicago PMI | (Jun) | 55.7 | 62.7 | !! |

US | 15:00 | JOLTS Job Openings | (May) | 7.280M | 7.618M | !!! |

Source: Bloomberg & Investing.com