USD rebound is supported by higher price of oil & hawkish Fed update

USD: Higher energy prices & hawkish Fed communication provide support

The US dollar has continued to rebound overnight resulting in the dollar index rising above the 99.000-level. The stronger US dollar has been encouraged by the rising price of Brent crude oil which hit a fresh high overnight of USD126.41/barrel. Upward price momentum accelerated after the previous high of USD119.50/barrel from 9th March was taken out. The latest developments clearly highlight the risk that the energy price shock will continue to get worse for the global economy if the Strait of Hormuz remains effectively closed. At the same time, the higher price of oil has been encouraged by an Axios report stating that President Trump is slated to receive a briefing on new plans for potential military action in Iran later today. The report goes on to add that the briefing signals that President Trump is seriously considering resuming major combat operation either to try to break the logjam in negotiations or to deliver a final blow before ending the war. CENTCOM has reportedly prepared a plan for a “short and powerful” wave of strikes on Iran, likely to include infrastructure targets, with the hope that Iran would then return to the negotiating table showing more flexibility on the nuclear issue.

In addition, the US dollar has derived support from the Fed’s relatively more hawkish policy update overnight. The Fed decided to leave their policy rate unchanged and maintained an easing bias, but indicated that they are moving towards more neutral policy stance. The decision to leave rates on hold was not unanimous. Dovish Fed Governor Stephen Miran dissented again in favour of a 0.25 point rate cut. More surprising were the dissents from hawkish Fed Presidents Beth Hammack, Neel Kashkari and Lori Logan against maintaining an easing bias in the policy guidance although they did support leaving rates on hold. In the press conference Fed Chair Powell stated that there had been a “vigorous discussion” about rate guidance and the decision to maintain an easing bias was a “much closer thing” than in March. He added rate guidance could conceivably change at the next meeting in June. He emphasized though that the policy stance is currently in a “very good place to wait” to see how the US economy is impacted by the fallout from the Middle East conflict. The shift towards a more neutral policy stance reflects more confidence that the US labour market is stabilizing. In response the US rate market has moved to price out further rate cuts from the Fed in the year ahead with rates expected to remain on hold for longer.

One important caveat is that it was the last FOMC meeting under Fed Chair Powell with Kevin Warsh likely to be in place to lead the Fed at the next policy meeting in June. The upcoming change in leadership may mean that last night’s policy update is a less useful guide than normal for potential policy changes ahead. Kevin Warsh could persuade the FOMC to maintain an easing bias. It was also notable that the Fed Chair Powell stated that he plans to stay on and serve as a governor on the Fed board for a period of time after he steps down as Fed Chair. He welcomed the Department of Justice’s recent decision to drop their criminal investigation but is waiting for the investigation to be well and truly over before leaving. He emphasized though that he plans to keep a low profile as a governor and it is not his intention to interfere. His decision to remain as a governor for now curtails the Trump administration’s ability to affect decision making in the near-term but with rates likely to remain on hold in light of the energy price shock, the actual policy impact could be limited.

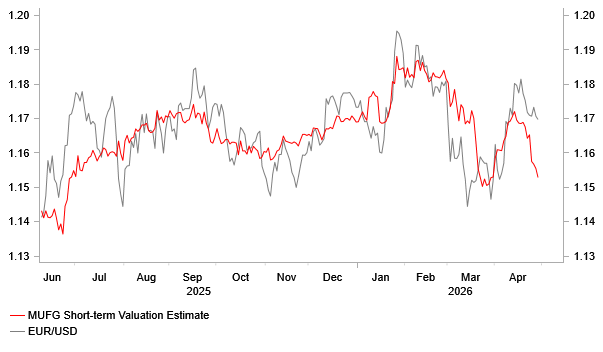

EUR/USD IS CORRECTING LOWER AHEAD OF ECB

Source: Bloomberg, Macrobond & MUFG GMR

EUR: Rising oil prices are moving ECB closer to adverse scenario & hikes

The euro has dropped backed below the 1.1700-level overnight hitting a low of 1.1655. The euro is correcting lower ahead of today’s ECB policy meeting after recently rising to a high of 1.1849 on 17th April. The euro has come under renewed selling pressure triggered mainly by the rising energy prices that are increasing the risk of a bigger stagflationary shock for European economies. The release this morning of the latest euro-zone GDP reports for Q1 will reveal how economies were performing at the start of this year prior to the energy price shock. It has already been revealed that France’s economy unexpectedly stagnated in Q1 which is weaker than expected starting point heading into the energy price shock. Still, the euro is holding up better than we had initially anticipated in response to the energy price shock. Based on past price action, we would have expected the euro to weaken by around -0.7% for every 10% increase in the price of oil. So far the price of Brent has increased by just over 70% since the conflict started but EUR/USD has only declined by just over 1% (rather than by around -5.0%). It highlights the disappointing performance of the US dollar but still makes us wary that the euro could weaken much further if the energy price shock continues to intensify.

One reason why the euro has held up better than expected against the US dollar has been the narrowing of yield spreads the euro-zone and US. Market participants expect the ECB to be more active in tightening policy than the Fed in response to the energy price shock. The euro-zone rate market is pricing in between 3-4 hikes from the ECB in the year ahead prior to today’s ECB policy meeting with the first hike expected to be delivered in June. President Lagarde recently stated that the euro-zone economy was somewhere between their baseline and adverse scenarios. The continued closure of the Strait of Hormuz and rising oil prices are moving the economy closer to the adverse scenario. The ECB has clearly laid out that in the adverse scenario, measured policy tightening is likely to be required. It supports our forecast for 50bps of rate hikes. We expect today’s policy update to leave policy guidance unchanged and tee up a hike at the next policy meeting if the situation in the Middle East does not improve quickly.

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

DE |

08:55 |

German Unemployment Change |

(Apr) |

4K |

0K |

!! |

|

DE |

09:00 |

German GDP (QoQ) |

(Q1) |

0.1% |

0.3% |

!!! |

|

EU |

10:00 |

GDP (QoQ) |

(Q1) |

0.2% |

0.2% |

!! |

|

GB |

12:00 |

BoE Interest Rate Decision |

(Apr) |

3.75% |

3.75% |

!!! |

|

GB |

12:30 |

BoE Gov Bailey Speaks |

- |

- |

- |

!!! |

|

EU |

13:15 |

Deposit Facility Rate |

(Apr) |

2.00% |

2.00% |

!!! |

|

US |

13:30 |

GDP (QoQ) |

(Q1) |

2.2% |

0.5% |

!!! |

|

US |

13:30 |

Initial Jobless Claims |

- |

213K |

214K |

!!! |

|

CA |

13:30 |

GDP (MoM) |

(Feb) |

0.2% |

0.1% |

!! |

|

US |

13:30 |

Employment Cost Index (QoQ) |

(Q1) |

0.8% |

0.7% |

!! |

|

EU |

13:45 |

ECB Press Conference |

- |

- |

- |

!!! |

|

GB |

14:15 |

BoE Gov Bailey Speaks |

- |

- |

- |

!!! |

Source: Bloomberg & Investing.com