Deal agreed will pressure front-end yields lower

USD: The Fed could find scope for easing by year-end

From having lurched back to escalation of military attacks from both the US and Iran we now have credible reports that a deal is imminent with President Trump expected to sign off on a Memorandum of Understanding that will see the current ceasefire being extended for a further 60 days in order for more meaningful negotiation on the main contentious issues to take place. Axios has reported that the deal includes a commitment to reopen the Strait of Hormuz and that the flow of traffic would be “unrestricted”. All mines planted by Iran would have to be removed within 30 days. In addition, the issue of Iran’s enriched uranium and Iran’s right to enrich in the future will be negotiated in tandem with negotiations on sanction relief and the unfreezing of Iranian assets. The financial markets are now likely to consolidate as investors await news on whether President Trump will accept the terms of the MoU. No doubt some within the administration will be opposed to moving this forward.

If the reported details are true and if President Trump does accept these conditions and we have a 60-day extension with, crucially, the Strait of Hormuz reopened we certainly would expect further near-term downside pressure on front-end rates and for the US dollar to weaken further. At this juncture it is difficult to know how quickly traffic through the Strait of Hormuz could normalise. If Iran has mines to clear and has 30 days to do so, we will see only a partial and gradual return of traffic. A high level of uncertainty is going to continue to exist throughout this negotiation period and hence the scope for a notable extension lower in crude oil prices is likely limited. Good news is already well priced with Brent crude oil now down close to 18% from the high on Monday of last week. But supply constraints are already building. US data released yesterday revealed that in the week to 22nd May, crude oil exports fell by 1mn barrels/day to 4.4mn barrels/day, the lowest since early April as crude gets diverted to domestic refineries. That will start to have a knock-on effect globally.

Will central banks like the ECB, who are indicating plans to hike reverse those plans at this stage with risk set to remain so high? We think that’s quite unlikely especially if crude oil prices settle not too much lower than here which seems reasonable. But for the Federal Reserve which the curve shows is priced for hikes much later, investors will be more likely to reverse that pricing which points to the potential for 2-year yields to potentially move lower in the US than in Europe or the UK. Refined fuel shortages is a bigger risk in Europe and if the resumption of Strait of Hormuz traffic does not go smoothly, further price rises is a notable risk, especially if US crude exports fall further to meet domestic refinery demand.

We may tweak our near-term US dollar forecasts a little weaker if this news is confirmed but given we are already expecting US dollar depreciation over the second half of the year and into Q1 2027 the broader forecast profiles and extent of US dollar depreciation across G10 will not change much at this early stage.

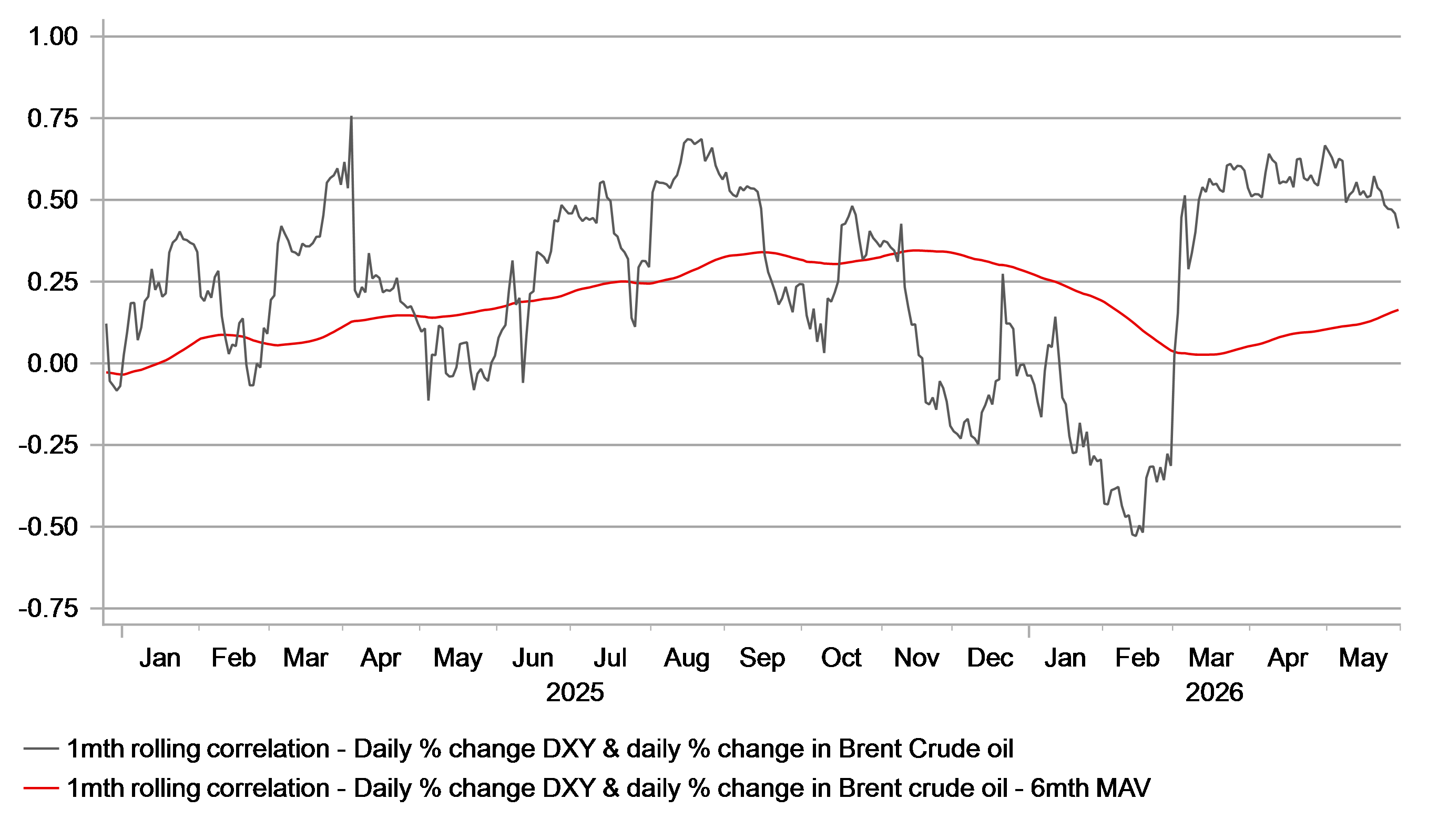

USD / OIL CORELATION WEAKENING BUT STILL ELEVATED

Source: Bloomberg, Macrobond & MUFG Research

JPY: Katayama remains markets of intervention threat

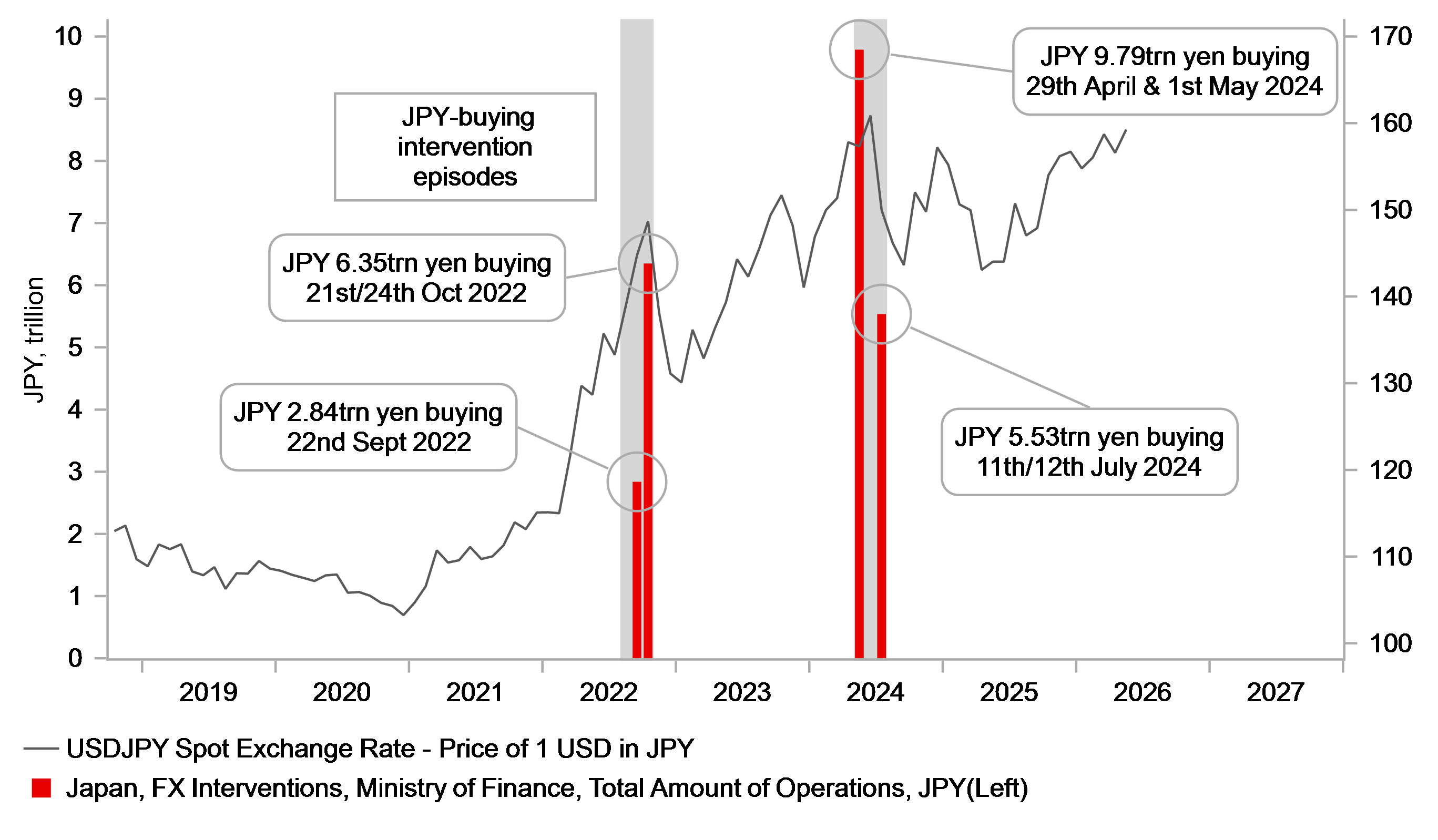

The reaction so far in the rates and FX markets to the widely reported news that a deal between the US and Iran is just awaiting President Trump’s sign off has been muted. DXY is roughly unchanged and the only G10 mover is the New Zealand dollar following RBNZ Assistant Governor Silk’s comment that the option of a 50bp hike in July is on the table. USD/JPY is unchanged today but has been drifting higher and is once again approaching the key 160-level. A credible 60-day extension to the ceasefire with the Strait of Hormuz reopening would be good news for the MoF in their attempts to curtail USD/JPY moves higher. Finance Minister Katayama today reiterated that the MoF can step in in circumstances of increased volatility and/or signs of speculative selling. There really wasn’t much evidence of increased volatility in yen trading ahead of intervention on 30th April and arguments made on speculative selling are difficult given how subjective that is when volatility is relatively low. Looking at 1-month USD/JPY implied vol, there was signs of the opposite – falling vol. On 28th April, 1-month implied vol fell to the lowest level since March 2024. That same measure has now dropped further, to a level not seen since before Russia invaded Ukraine in February 2022. The justification for intervention on grounds of volatility has never been weaker since yen buying intervention was first undertaken in September 2022.

Today, at 11am BST, the MoF will release the intervention data covering the period from 28th April to 27th May. Based on the BoJ daily current account data tracking bank reserves data, the estimate for yen buying intervention was put at around JPY 10trn, combining the two probable episodes of intervention – 30th April and 6th May. If the confirmed total is in that ballpark we will likely have confirmation of the largest combined two-day episode of intervention since yen buying intervention began. It would be similar in size to April-May 2024 when intervention totalled JPY 9,789bn. The speed in which USD/JPY has returned close to the levels when intervention took place means this latest intervention, while possibly the largest, was also the least successful. Getting USD/JPY lower from here will still be more about this potential Middle East deal and if global yields do fall on reduced inflation fears then that will likely prove the key development for a lower USD/JPY.

YEN BUYING INTERVENTION IN TODAY’S DATA COULD BE LARGER THAN RECENT PAST YEN BUYING OPERATIONS

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

GE | 08:55 | German Unemployment Rate | (May) | 6.4% | 6.4% | !! |

GE | 08:55 | German Unemployment Change | (May) | 11K | 20K | !! |

EU | 09:00 | Private Sector Loans (YoY) | (Apr) | - | 3.0% | ! |

UK | 09:20 | BoE Gov Bailey Speaks | - | - | - | !!! |

US | 11:50 | Fed's Schmid speaks | !! | |||

GE | 13:00 | German HICP (MoM) | (May) | 0.2% | 0.5% | ! |

GE | 13:00 | German HICP (YoY) | (May) | 2.9% | 2.9% | ! |

CA | 13:30 | GDP Annualized (QoQ) | (Q1) | 1.5% | -0.6% | !!! |

CA | 13:30 | GDP (MoM) | (Mar) | 0.1% | 0.2% | !! |

US | 13:30 | Goods Trade Balance | (Apr) | -86.70B | -87.45B | !! |

US | 13:30 | Wholesale Inventories (MoM) | (Apr) | 0.6% | 1.3% | ! |

US | 14:10 | Fed's Bowman Speaks | - | - | - | !!! |

US | 14:15 | Fed's Paulson speaks | !!! | |||

US | 14:45 | Chicago PMI | (May) | 50.6 | 49.2 | !! |

CA | 16:00 | Budget Balance | (Mar) | - | 5.66B | ! |

CA | 16:00 | Budget Balance (YoY) | (Mar) | - | -25.55B | ! |

US | 17:40 | Fed's Daly Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com