Focus on earnings & Fed as energy supply concerns rise

USD: No sign of re-opening Strait of Hormuz as Fed assesses risks

The US dollar is broadly unchanged today with Asian equities mostly higher today despite the declines recorded in the US yesterday. There is a distinct lack of appetite to sell US equities with a heavy schedule of corporate earnings announcements today and tomorrow. As of last Friday, according to Factset, 28% of companies have reported and the earnings annual growth rate is currently at 15.1%, which if realised would make Q1 the sixth consecutive quarter of double-digit corporate earnings growth. Alphabet, Microsoft, Amazon and Meta all report this evening after the close and then Apple reports tomorrow. Given the resilience of corporate earnings growth, it is understandable why investors are willing to make optimistic assumptions over how the Middle East conflict will play out over the coming weeks and months. Favourable risks conditions appear to us to be a factor weighing on US dollar performance.

And the news related to the Middle East doesn’t sound particularly positive. The Wall Street Journal is reporting today that President Trump has instructed his key aides to prepare for an extended blockade of the Strait of Hormuz as Trump has concluded that it was less of a risk than either restarting military action or accepting the terms of the latest Iranian offer that would have ultimately seen the US walk away. Crude oil is again trading back above the USD 110pbl level with potential economic consequences over the summer period becoming more severe. Europe and Asia will be more severely hit and if this drags on there will be increased downside pressure on the euro and Asian currencies. Diesel supplies have been helped by a notable pick-up in output from the Amsterdam-Rotterdam-Antwerp (ARA) hub encouraged by widening refined fuel margins. But according to Insights Global, inventories are now falling more notably and have reached an 8-month low.

This is the backdrop for this evening’s FOMC meeting, and we should expect to hear a key message from Fed Chair Powell that the monetary stance is well placed currently given the level of uncertainty. There are unlikely to be any strong message on guidance specifically with Powell likely to emphasise there being available time to assess the risks. The incoming economic data since the last meeting has generally been favourable with resilient retail sales and an NFP report that revealed stronger than expected jobs growth. Market-based inflation expectations have also been remarkably stable with the 5y5y inflation swap up a mere 2bps since the conflict began.

However, at the margin we would expect Fed Chair Powell to come across more hawkishly than at the last press conference in March. There are signs emerging of inflation risks and with the economy resilient and US equity markets remaining resilient, inflation risks are surely building. The ISM manufacturing prices paid index has now surged 19.3pts in two months, the largest gain since 2016. The one-month ISM services prices paid increase (7.7pts) was larger than any period post-covid and the largest since 2012. While we doubt Powell will be aggressively hawkish (given its probably his last press conference) there is a case for emphasising building price stability risks and that will likely see a jump in yields at the front-end of the US curve that should reinforce the emerging signs of improving US dollar demand. EUR/USD downside risks and USD/JPY upside risks are building.

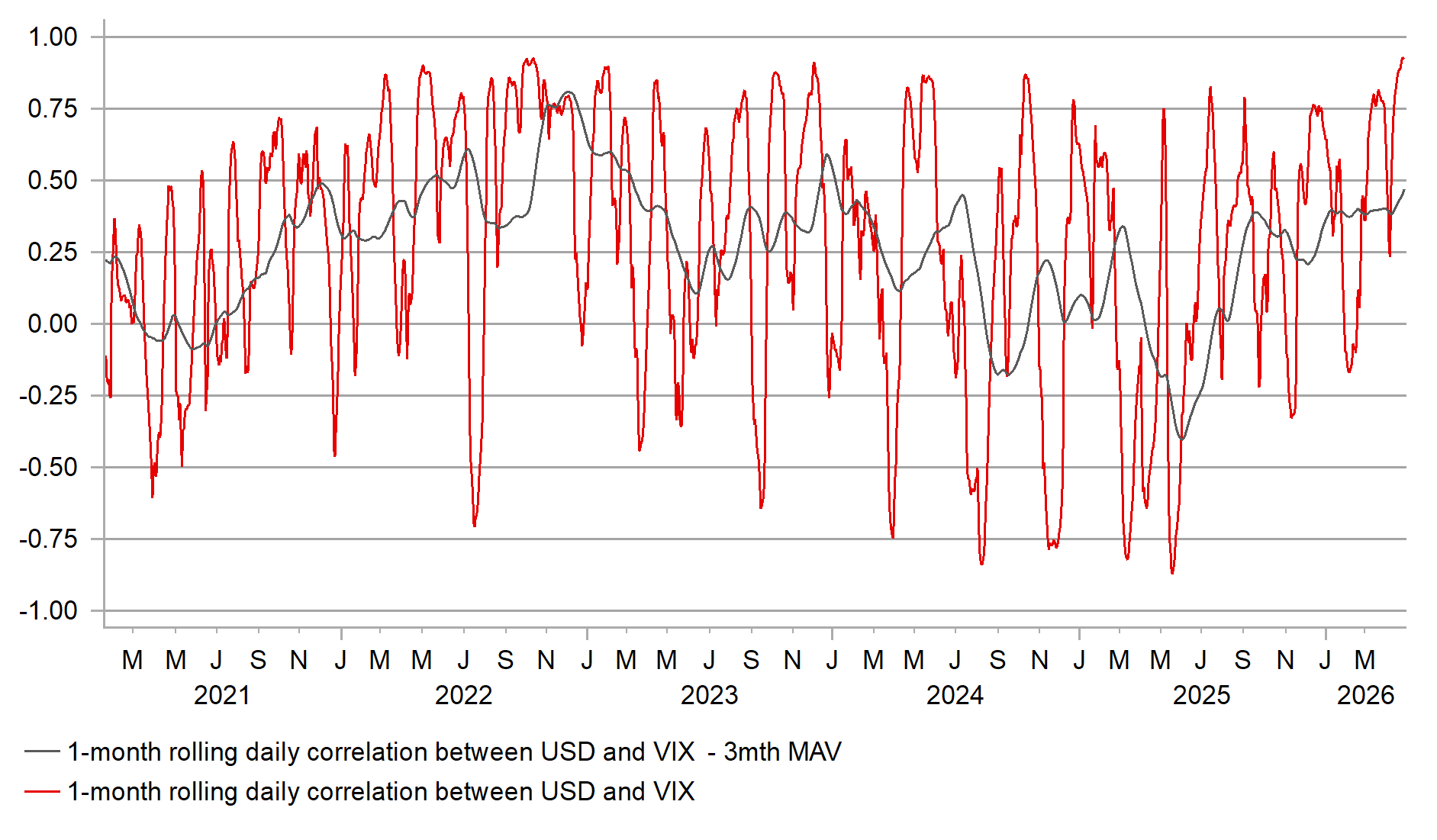

EQUITY VOL / USD CORRELATION AT STRONGEST IN POST-COVID PERIOD

Source: Bloomberg, Macrobond & MUFG GMR

CAD: BoC to hold with a more hawkish tone

The Canadian dollar is close to unchanged versus the US dollar since the conflict in the Middle East began and is the fourth best performing currency alongside the US dollar with the Norwegian krone, Australian dollar and pound outperforming. In addition to the FOMC, the Bank of Canada meets today and an unchanged monetary stance is widely expected. We also get the release of the Monetary Policy Report and we will likely see a downward revision to GDP growth for this year along with an upward revision to inflation. Any downgrade to the BoC’s GDP forecast for this year will likely reflect the impact of the start of the war and should be modest. Given the high level of uncertainty related to the conflict these updated forecasts are unlikely to have the market impact they sometimes can have.

The same can be said in relation to the higher inflation forecasts although we see greater risks of a more lasting impact on inflation. In a de-escalation scenario it seems reasonable to us to assume that a retracement in energy prices will be to levels that are still higher than pre-conflict levels if you assume some amount of additional geopolitical risk premium is likely to remain. That means a higher level of inflation than assumed prior to the conflict that may become difficult to look through. The BoC indicated in March at the last meeting that it would focus more initially on downside growth risks that upside inflation risks. That in part reflects the fact that inflation was a little lower than expected at the start of the conflict.

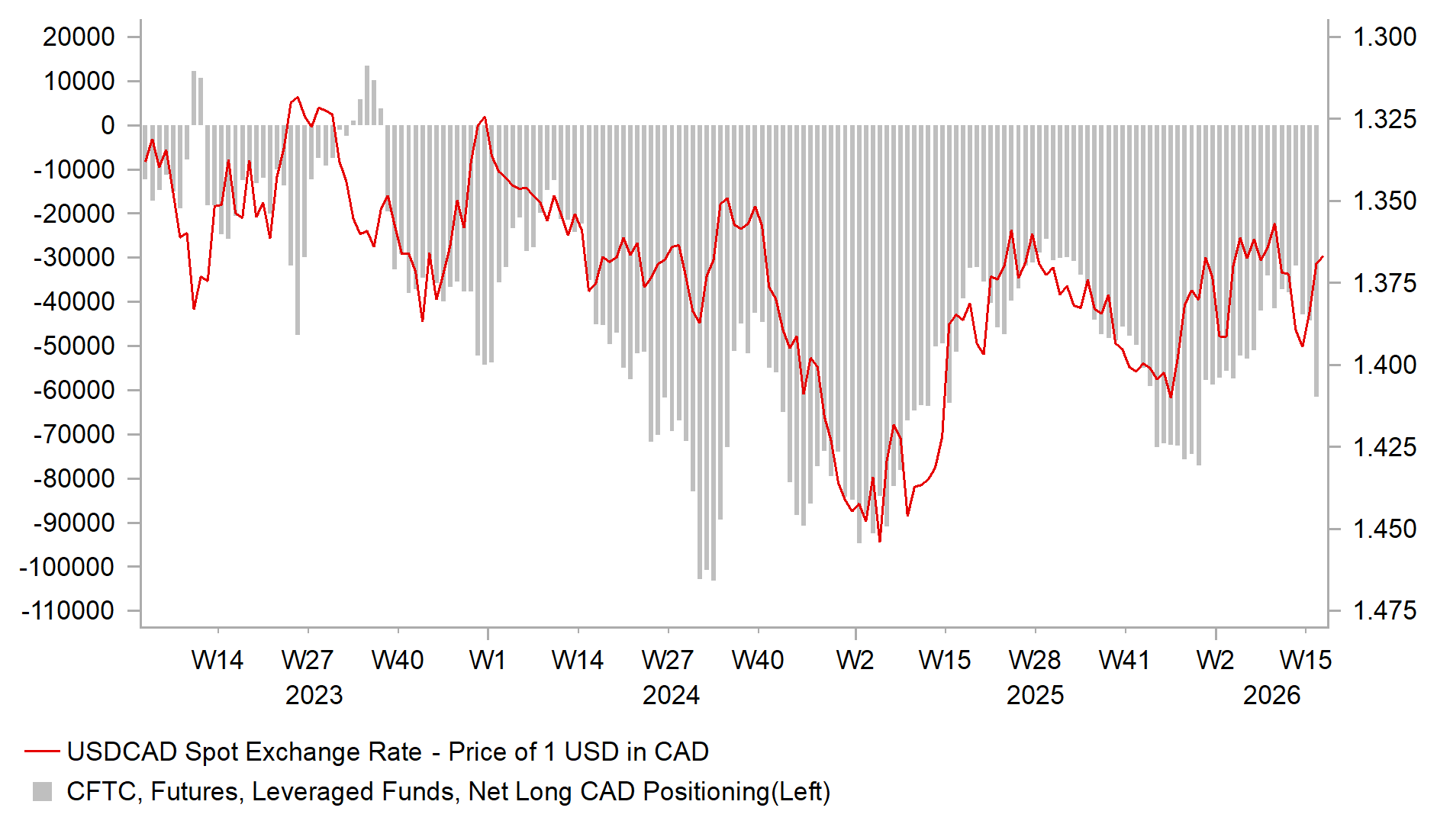

However, at today’s meeting the backdrop will be no end in sight to the closure of the Strait of Hormuz while risk assets have remained resilient. We expect the BoC to therefore be certainly more hawkish than in March with some signs of a shift in focus toward upside inflation risks. However, the Fed also could be more hawkish and US yields could move higher resulting in limited moves in US-CA spreads. Our short-term bias favours the US dollar based on the increasing prospect of re-escalation of the conflict and a further rise in crude oil prices. The latest IMM positioning data saw the largest week of CAD selling by Leveraged Funds since July 2024. While the Canadian dollar could underperform the US dollar in a re-escalation scenario, we would expect moves to be more modest and for CAD to outperform other energy import-dependent G10 currencies.

LEVERAGE FUNDS REMAIN SHORT CANADIAN DOLLARS WITH A RECENT PICK-UP IN CAD SELLING

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EU |

09:00 |

Loans to Non-Financial Corporations |

(Mar) |

- |

2.9% |

! |

|

EU |

09:00 |

M3 Money Supply (YoY) |

(Mar) |

3.1% |

3.0% |

! |

|

EU |

10:00 |

Industrial Sentiment |

(Apr) |

-7.2 |

-7.0 |

! |

|

EU |

10:00 |

Services Sentiment |

(Apr) |

3.5 |

4.9 |

! |

|

EU |

10:00 |

Consumer Confidence |

(Apr) |

-20.6 |

-16.3 |

! |

|

DE |

13:00 |

German CPI (MoM) |

(Apr) |

0.7% |

1.1% |

!!! |

|

DE |

13:00 |

German CPI (YoY) |

(Apr) |

3.0% |

2.7% |

!!! |

|

US |

13:30 |

Housing Starts |

(Mar) |

1.380M |

1.487M |

!! |

|

US |

13:30 |

Building Permits |

(Mar) |

1.390M |

1.386M |

!! |

|

US |

13:30 |

Goods Trade Balance |

(Mar) |

-87.50B |

-83.50B |

! |

|

US |

13:30 |

Durable Goods Orders (MoM) |

(Mar) |

0.4% |

-1.3% |

! |

|

US |

13:30 |

Goods Orders Non Defense Ex Air (MoM) |

(Mar) |

0.5% |

0.6% |

!! |

|

CA |

14:45 |

BoC Interest Rate Decision |

- |

2.25% |

2.25% |

!!!! |

|

CA |

14:45 |

BoC Monetary Policy Report |

- |

- |

- |

!! |

|

CA |

15:30 |

BOC Press Conference |

- |

- |

- |

!!! |

|

US |

19:00 |

Fed Interest Rate Decision |

- |

3.75% |

3.75% |

!!! |

|

US |

19:30 |

FOMC Press Conference |

- |

- |

- |

!!!!! |

Source: Bloomberg & Investing.com