JGB demand picks up but US yield again key for USD/JPY

JPY: Yen stable after solid JGB auction as Ueda highlights inflation risks

USD/JPY is close to unchanged, reflecting the general stability in foreign exchange bar the New Zealand dollar which is the top performing G10 currency today following the RBNZ meeting, which signalled the need for more rate hikes than previously thought and for action to come sooner – a rate hike at the next meeting in July is now very likely and close to fully priced. Yields in Japan have gone the other way with JGB yields down across the curve in part helped by a renewed decline in crude oil prices helping the front-end and a stronger than expected 40-year JGB auction helping the long-end. The bid-to-cover ratio of 2.7 compared to 2.54 at the last auction and a 12-month average of 2.47. Again, we have more evidence of improved underlying demand, likely reflecting the more attractive yield level. A 20-year auction last week saw a bid-to-cover of 4.01, easily surpassing the 12-month average of 3.43.

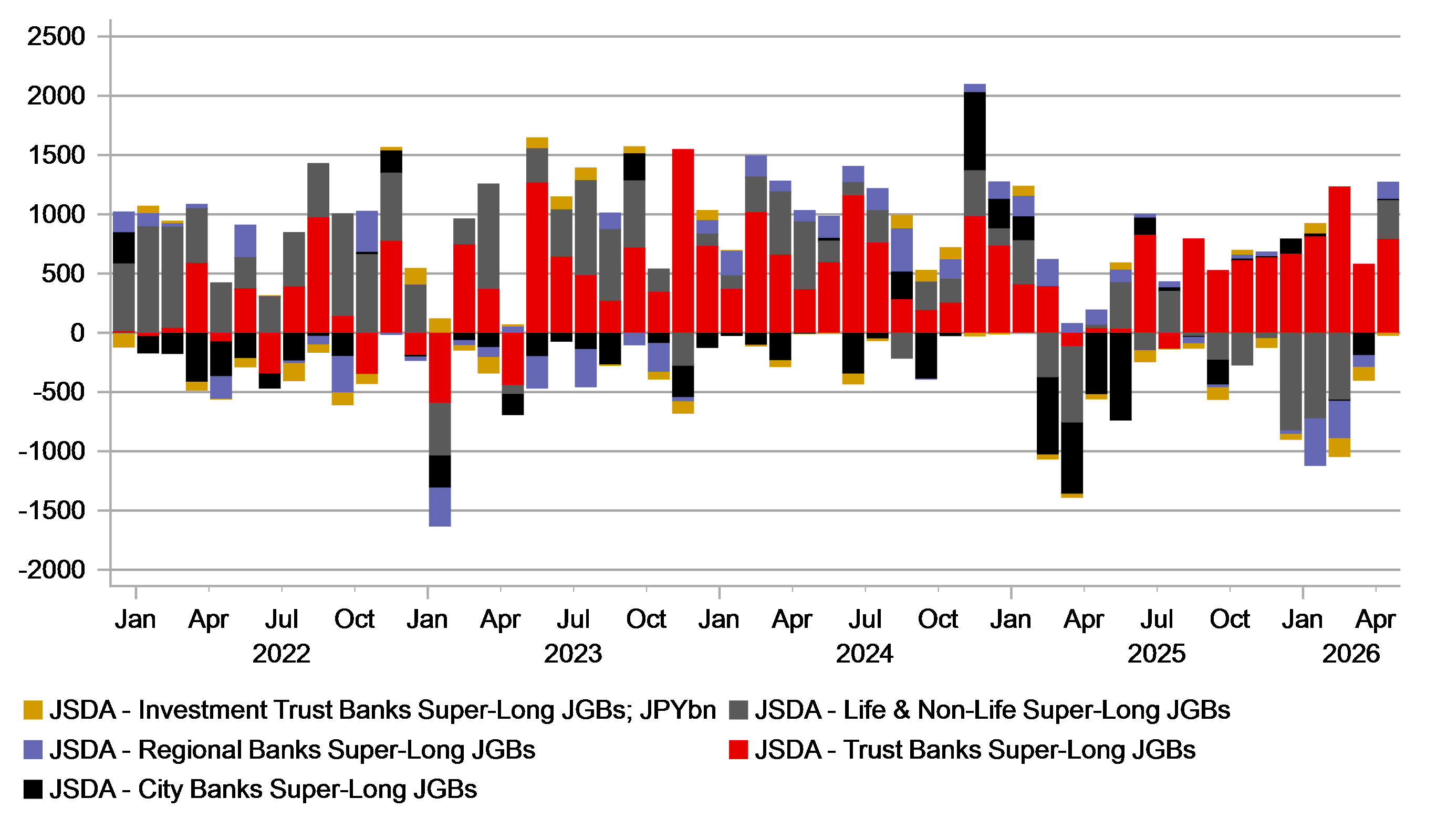

The evidence of improving underlying demand for JGBs at recent auctions is also evident in the flow data. The monthly JSDA flow data for the month of April was released last week and revealed much better broad-based buying of super-long JGBs by Japanese investor types. Trust banks were continued buyers, but lifers and regional banks turned buyers as well and total buying of five key investor types combined was the largest since December 2024. It’s too soon to conclude that domestic buying of the long-end will pick up more consistently but there are early signs that underlying demand will improve. We would still argue that improved BoJ credibility and reduced fears of the BoJ being behind the curve would help demand at the super-long end of the curve.

In that context, BoJ Governor Ueda gave a speech in Tokyo today when he opened a two-day international banking conference and stated that the current oil price shock was a “test of the entire inflation regime”. Governor Ueda did not talk specifically on the outlook for monetary policy but did emphasise where the risks lie adding that a temporary shock “can become persistent if it changes wages, expectations and price-setting behaviour”. While there is no specific evidence of that now, we would argue that since the covid shock and the Russia/Ukraine energy shock there have been changes in wage growth that therefore warrant greater vigilance as we deal with another energy shock again now. Given the current favourable risk backdrop globally, the improved prospects of some form of peace deal and the continued weakness of the yen, we see it as very likely that the BoJ will hike at the next meeting in June. About 19bps of a rate rise is currently priced for that meeting.

So, with a June BoJ rate hike well priced, a hike is unlikely to be the catalyst for a sudden revival of the yen from current weak levels although it would certainly help curtail yen selling through the 160-level, especially given the credible threat of intervention. A more hawkish Fed does for now limit the scope for a correction lower and while the front-end US-JP yield spread has not been a reliable driver of USD/JPY, the correlation has picked up over the last six weeks. Therefore, US data next week will be important in determining whether we see another move higher to test the resolve of the MoF to halt yen depreciation.

JAPANESE INVESTOR DEMAND FOR SUPER-LONG JGBS PICKED UP IN APRIL

Source: Bloomberg, Macrobond & MUFG Research

EUR: The message is clear

The rebound in crude oil prices yesterday after the plunge of over 7% on Monday saw yields retrace with yields in Europe higher – the 2-year yield in Germany jumped 6bps recouping more than half the 10bp drop on Monday. The 2-year yield is now around the 2.55% level which could quickly be deemed as too low if the ECB follows through on the clear communication of late that suggests a 25bp policy rate hike on 11th June is very likely. That meeting will include an update on the forecasts provided in March when the ECB laid out three scenarios for how the Middle East conflict would influence energy prices and inflation. Chief Economist Philip Lane spoke yesterday and confirmed that the ECB would be raising further its inflation projections under the baseline scenario – in March the baseline scenario inflation projection for 2026 was 2.6% (the projections for adverse and severe were 3.5% and 4.4% respectively). Lane added that the energy shock shifting into a broader inflation problem would be a “major issue” for the ECB. Lane wouldn’t be drawn on the decision in June, but Executive Board member Isabel Schnabel was more willing to do just that stating in a separate interview that “looking through is no longer an option” given her view of the size and persistence of the current shock.

The prospect of the shock becoming broad-based and therefore a “major issue” still looks remote in our view. An ECB blog posted yesterday went into some detail on the impact of the conflict in the Middle East on reshaping euro-zone firms’ expectations and cited data including from the Survey on the Access to Finance of Enterprises and the conclusion was clear – euro-zone firms have raised their short-term cost, price and inflation expectations but have marked down expectations on factors driving economic growth. However, wage expectations and long-term inflation expectations remain stable and hence the current shock is unlikely to become persistent.

So that likely means limited action will be required from the ECB but with the baseline inflation projection set to rise, not hiking rates would certainly be questioned and difficult to explain. A hike is fully priced with a second hike nearly fully priced by September. EUR/USD downside risks from here on rate spread moves should be limited given the Fed is unlikely to hike rates in 2026.

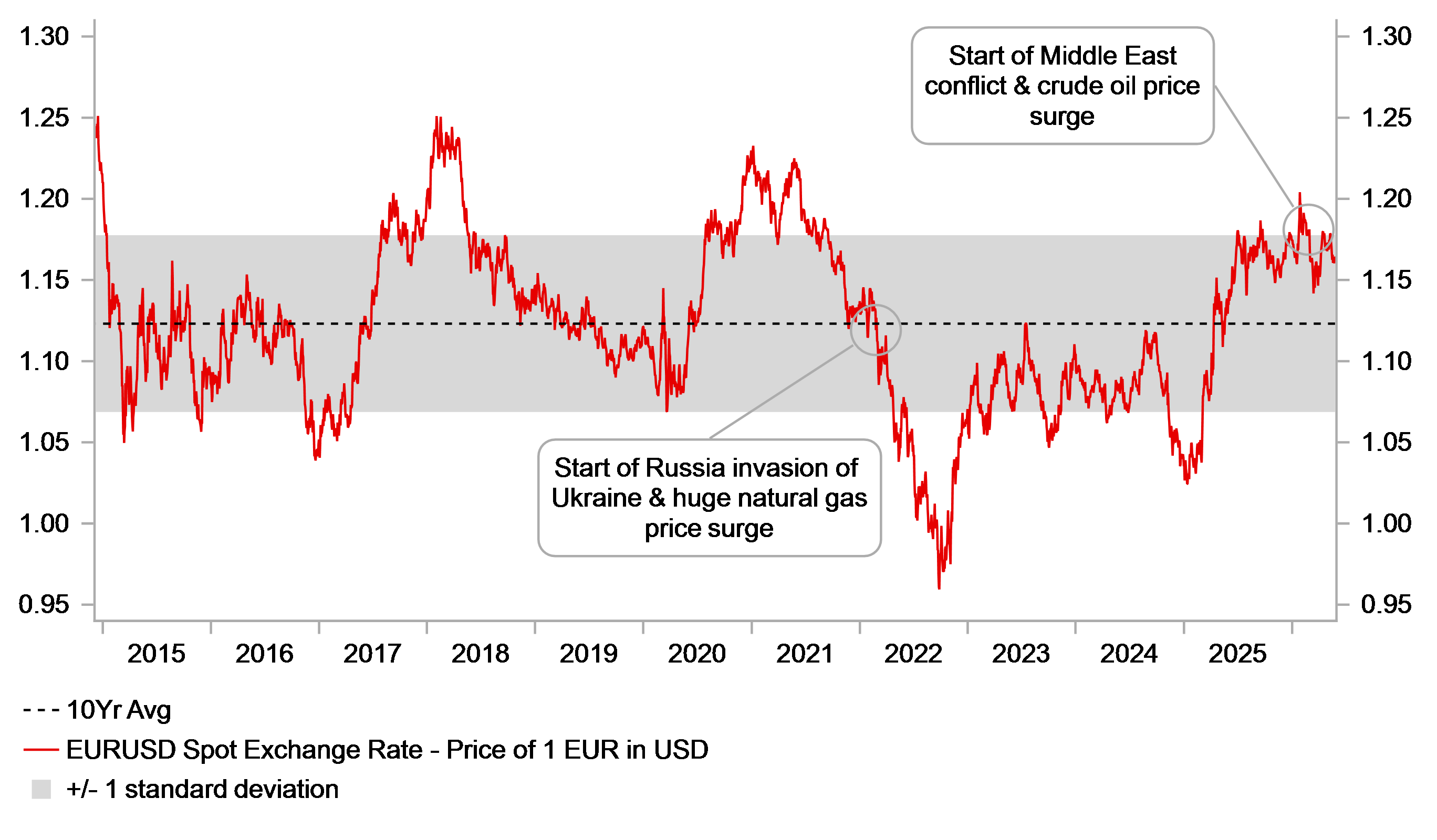

EUR/USD REMAINS CONSOLIDATED WELL ABOVE 10-YEAR AVERAGE

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 09:00 | ECB Financial Stability Review | - | - | - | !! |

CH | 09:00 | ZEW Expectations | (May) | - | -30.3 | ! |

US | 09:00 | Fed Logan Speaks | - | - | - | !!! |

US | 12:00 | MBA Mortgage Applications (WoW) | - | - | -2.3% | ! |

US | 15:00 | Richmond Manufacturing Index | (May) | 4 | 3 | ! |

US | 15:00 | Richmond Manufacturing Shipments | (May) | - | -2 | ! |

US | 15:30 | Texas Services Sector Outlook | (May) | - | -9.9 | ! |

US | 18:00 | 5-Year Note Auction | - | - | 3.955% | !! |

US | 20:55 | Fed Governor Cook Speaks | - | - | - | !!! |

Source: Bloomberg & Investing.com