Optimism on Middle East truce mixed with uncertainty

USD: USD reverses course after sell-off on optimism

Yesterday, while US and UK markets were closed, news of a peace deal had helped fuel a notable bout of optimism. Crude oil prices fell over 7% and the US dollar dropped with the Swedish krone and the Australian dollar the top performing G10 currencies as global growth optimism improved. However, strikes by the US in the region overnight has undermined this optimism and created elevated uncertainty. The retracement of moves yesterday fuelled by the optimism have not been fully complete today with US officials still indicating that negotiations are ongoing for a deal to be made. With only a moderate rebound so far today, the drop in crude oil is meaningful – from the start of last week, Brent crude oil is now down nearly 15% underlining the level of optimism now priced for some deal to be reached.

Marco Rubio has played down the US attacks stating that the talks would “take a few days” while President Trump posted that the talks were “proceeding nicely”. US Central Command described the strikes as defensive and had targeted launch sites and boats trying to place mines. The negotiations also appeared stuck on certain aspects like Iran’s ability to control traffic through the Strait of Hormuz and how to deal with Iran’s stocks of enriched uranium. These are the issues that have long been the source of disagreement and hence there must be a degree of scepticism over the imminence of a deal being announced. While President Trump has been keen to highlight the progress and an imminent deal, Iran have been actively countering the news of a deal being close. An Iranian spokesperson acknowledged the progress but dismissed the view of a deal being close.

That would suggest, especially after the US strikes, that there is a risk of a further unwind of the move in markets yesterday. The FX moves yesterday were more subdued than the moves in crude oil or in rates – the 2-year German bund yield fell 10bps but EUR/USD had a range of only 30 pips, perhaps reflecting the fact that UK and US markets were closed. The big moves were SEK and AUD and there is certainly scope for a bigger retracement to unfold in those pairs if a deal is not announced soon. EUR/USD could underperform with expectations that we could see a significant escalation in the Russia/Ukraine conflict after reports that Russia has requested the US to evacuate its diplomats from Kyiv ahead of a planned escalation in attacks. The euro performance has lagged trading toward the bottom of the G10 performance table relative to last Friday.

US yields look set to continue to provide support for the dollar with Fed officials more aligned with focusing on inflation risks. Fed Governor Waller’s speech last week underlined the shift with a signal of a potential rate hike if “inflation does not abate soon”. We do not believe a rate hike is coming this year and indeed if a credible peace deal is achieved a rate cut this year is still feasible. But until both sides formally announce a deal, investors will likely trade cautiously given the inflationary pressures that are building.

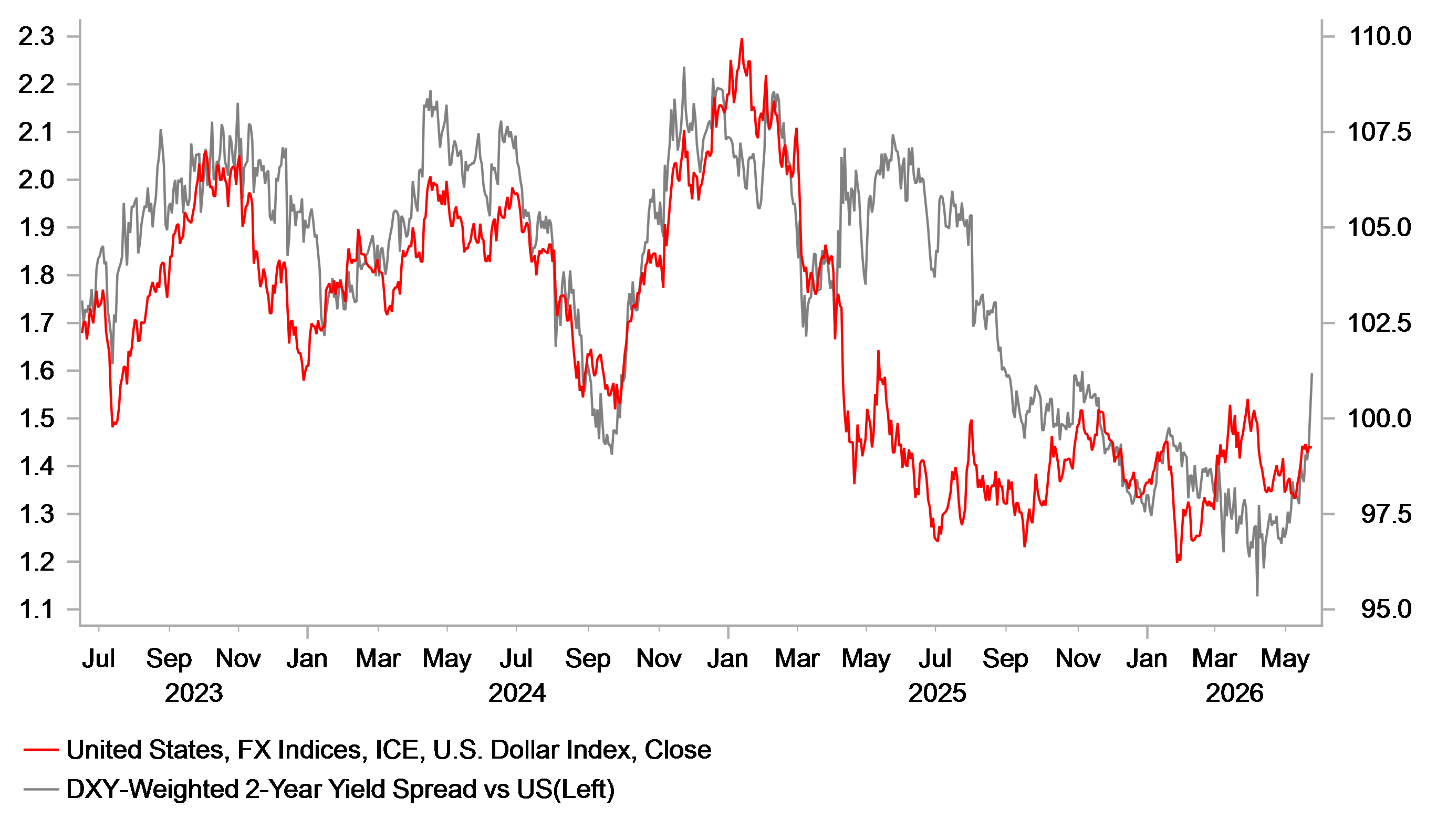

USD LAGGING MOVE HIGHER IN YIELD SPREADS

Source: Bloomberg, Macrobond & MUFG Research

NZD: RBNZ in focus

The RBNZ will meet later tonight with little priced and a strong likelihood that there will be no change in the key policy rate, currently at 2.25%. But based on current market pricing there may well need to be some hawkish indications provided by the RBNZ in terms of the outlook for monetary policy given the scale of tightening currently priced. Even after the positive news in recent days that may result in the Strait of Hormuz reopening, the OIS market indicated nearly five rate hikes by the RBNZ over the next 12mths. The pricing has been influenced by the signals from the RBNZ and at the last policy meeting on 8th April, the RBNZ made clear it that it had discussed the merits of a “relatively early” rate hike. Governor Breman did clarify those comments stating that there was no intention to hike at that meeting. Still, the RBNZ estimated that inflation would accelerate to 4.2% in Q2, well above the 1%-3% inflation target range. Since that meeting, Q1 inflation was released showing headline CPI at a stronger YoY rate of 3.1% although business and consumer confidence readings have declined notably. Q1 employment growth was also weaker than the market consensus at 0.2% Q/Q and credit card spending fell 1.6% MoM in April. However, overall retail sales data, released last week revealed a 0.9% Q/Q increase in real terms that was stronger than expected. Overall, the data has been mixed but definitely not weak enough to warrant caution in communication.

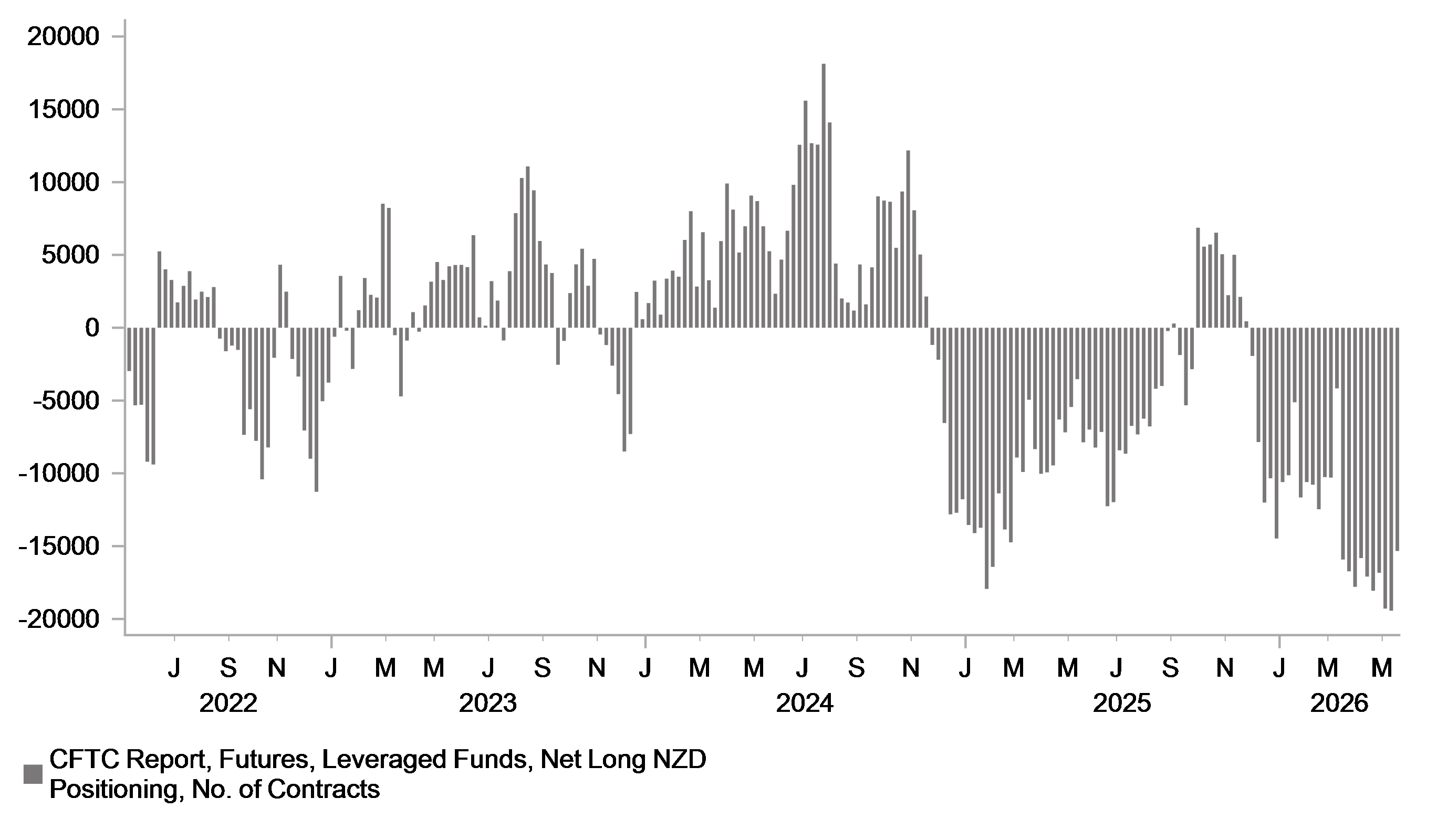

This RBNZ tomorrow will also release updated forecasts that will show higher inflation and a higher projected OCR rate for this year and next. The RBNZ does have a recent history of responding aggressively to inflation risks and we expect to see another hawkish message tomorrow that will help validate current market pricing. The NZIER Monetary Shadow Board policy indicated a split in terms of action by the RBNZ with three members arguing that the RBNZ should hike but overall the view was for rates to remain on hold in May. Given the bad data readings were mostly sentiment indicators that could turn around on a peace deal being reached, a signal of between two and three rate hikes this year from the RBNZ seems plausible. With around 70bps priced that would be broadly consistent with market pricing that should help support NZD positive momentum if the US dollar weakens back on a peace deal being reached between the US and Iran. NZD Leveraged Funds’ short position was pared to the week to last Tuesday after reaching the largest short since December 2019.

OPTIMISM ON A US-IRAN PEACE DEAL COULD HELP NZD TO OUTPERFORM WITH HEAVY SPECULATIVE SELLING REVERSED

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

UK | 11:00 | CBI Distributive Trades Survey | (May) | -52 | -68 | ! |

CA | 13:30 | Manufacturing Sales (MoM) | (Apr) | - | 3.0% | ! |

US | 13:30 | Chicago Fed National Activity | (Apr) | - | -0.20 | ! |

US | 14:00 | S&P/CS HPI Composite - 20 n.s.a. (YoY) | (Mar) | 0.9% | 0.9% | !! |

US | 14:00 | House Price Index (YoY) | (Mar) | - | 1.7% | ! |

US | 14:00 | S&P/CS HPI Composite - 20 s.a. (MoM) | (Mar) | - | -0.1% | ! |

US | 14:00 | House Price Index (MoM) | (Mar) | 0.1% | 0.0% | ! |

US | 15:00 | CB Consumer Confidence | (May) | 91.9 | 92.8 | !!! |

US | 15:30 | Dallas Fed Mfg Business Index | (May) | - | -2.3 | ! |

Source: Bloomberg & Investing.com