USD loses upward momentum at the end of the week

USD: Upward momentum dampened by US data and Fed rhetoric

The US dollar is on track to strengthen for the second consecutive week although it has lost some upward momentum heading into next week. The US dollar’s upward momentum was dampened yesterday by latest US economic data releases and comments from New York Fed President Williams that have triggered a reversal of the recent hawkish repricing of Fed rate hike expectations. The 2-year US Treasury yield has dropped around 7bps from yesterday high and moved back closer to where it was trading prior to last week’s FOMC meeting. US yields and US dollar fell after the release of the latest US GDP data for Q1 which revealed that consumer spending slowed more than previously reported by only 0.5% down from 1.4%. The downward revision (-1.3ppts) was mainly driven by services consumption. It was the slowest quarter of personal consumption growth since Q1 2022. It has cast some doubt on the resilience of the US economy with fiscal support from President Trump’s tax cuts set to fade during the second half of the year. Import growth was also revised down alongside personal consumption which more than offset the hit to GDP growth in Q1. The breakdown of growth in Q1 reveals that the economy was driven by a pick-up in capital expenditure which increased sharply by 15.8% reflecting the ongoing AI roll out, and government spending which increased strongly by 4.4%. In contrast, the latest US PCE deflator report contained few surprises which in the current circumstances of upside inflation risks provided some temporary relief for financial markets and the Fed. The report revealed that the core PCE deflator increased for the second consecutive month by 0.3%M/M in May lifting the annual rate up to 3.4%. The core PCE deflator was driven by services inflation with portfolio management fees increasing by 4.9%, air transportation by 3.1% and healthcare by 0.4%. In contrast, the core goods deflator fell by -0.1%M/M. Evidence of slowing inflation in the coming months will be required to prevent the Fed from backing up tough talk with rate hikes.

The correction lower for US yields and the US dollar yesterday was also encouraged by comments from New York Fed President Williams. He stated that “the current stance of monetary policy is well positioned to do that” when referring to resorting inflation to our 2% longer-run goal on a sustained basis. However, he did acknowledge that inflation is “unquestionably elevated” driven by tariffs, an energy shock from the Iran war and an investment boom in AI. He is wary that the investment boom in AI may push up prices more than expected, and global supply disruptions stemming from the conflict in the Middle East remain a source of risk to both growth and inflation outlooks. He expects inflation to ease back to 3.5% by year-end and then continue to slow on a glide path toward 2.0% reaching the target in 2028. He noted that the fade effects of trade tariffs and slowing shelter costs should help to ease inflation in the coming quarters. Energy and goods prices should also stabilize if the conflict is resolved relatively soon. Overall, the comments are supportive of our view that the Fed will look through the energy price shock by leaving rates on hold this year, although he has consistently been at the more dovish end of the spectrum. If the Fed does not follow through with rate hikes, we expect the US dollar to re-weaken later this year.

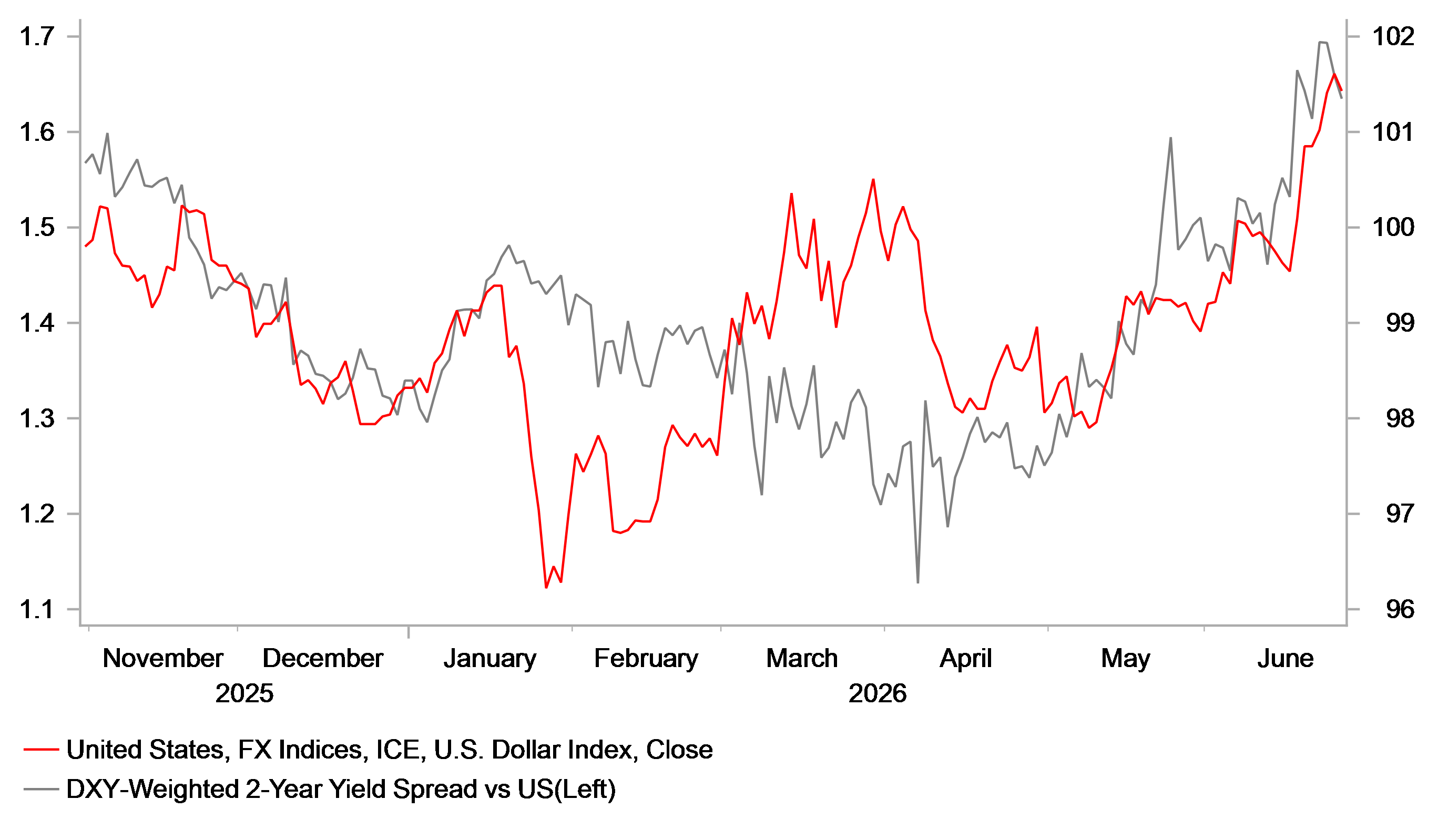

USD HAS BECOME TIGHTLY LINKED TO YIELD SPREADS AGAIN

Source: Bloomberg, Macrobond & MUFG Research

JPY: Stronger inflation keeps pressure on BoJ to normalize policy

The JPY is continuing to trade close to year-to-date lows against the US dollar after it briefly touched the high from July 2024 yesterday at 161.95. The risk of intervention is helping to dampen yen weakness in the near-term and contributing to the yen outperforming other G10 currencies alongside the strengthening US dollar in recent weeks. After hitting a high of 186.32 on 17th June, EUR/JPY has dropped back below the 184.00-level moving back closer to support from the 200-day moving average at around182.50.

The yen has continued to weaken this month even as the BoJ has hiked rates putting pressure on Japan to intervene again to slow the pace of depreciation even though the last bout of intervention in late May/early April proved to be largely ineffective. The case for further BoJ rate hikes was supported by the release of the latest Tokyo CPI report for June. The report revealed that headline and core inflation measures were stronger than expected rising to 1.7% and 1.9% respectively. Headline inflation was mainly driven by distortion from water-fee waiver sin the capital that contributed 0.23 percentage points. Measures to cap gasoline prices in June of last year also created a positive base effect. However, even after stripping out these effects, there was underlying evidence of stronger inflation with firms passing on higher labour costs, and the weaker yen lifting import prices.

The BoJ has recently indicated that there is higher risk that inflation could overshoot their target. It has encouraged expectations that they could speed up the pace of hikes by delivering the next hike as soon as the October policy meeting rather than waiting until December. There are currently around 14bps of hikes priced in by October. A BoJ rate hike could push down USD/JPY more if the Fed also disappoints market expectations for rate hikes starting in the autumn.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

DE | 09:30 | German Buba President Nagel Speaks | - | - | - | !! |

US | 13:30 | Goods Trade Balance | (May) | -85.00B | -83.01B | !! |

US | 15:00 | Michigan Consumer Expectations | (Jun) | 49.3 | 44.1 | !! |

US | 15:30 | FOMC Member Williams Speaks | - | - | - | !! |

US | 16:30 | FOMC Member Kashkari Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com