Limited progress toward peace as USD grinds higher

USD: USD/JPY grinds higher toward 160-level

The US blockade in the Strait of Hormuz continues with little sign of any progress toward another round of peace talks. President Trump has ordered the US navy to shoot at any boat laying mines while the US military stated that it had intercepted two oil supertankers that had tried to evade the blockade. The focus now is fully on the Strait of Hormuz and pressuring Iran into shifting its position. However, Iran knows there is a time limit for the US as well and the inflationary impact of the closure will have a US and global impact that will be damaging for President Trump (see below). The risk must be that Iran’s tolerance for pain will be considerable and in that regard this stalemate could drag on to the extent that crude oil prices soon hit new highs and create greater financial market volatility.

The tolerance for such a scenario is also likely to test central bankers’ tolerance for doing nothing as inflation risks continue to rise. There are a host of central bank meetings next week and no rate hikes are expected from the big four central banks but that could well change by the time of the next round of meetings in June. The BoJ will meet on Tuesday and is expected to leave its policy stance unchanged.

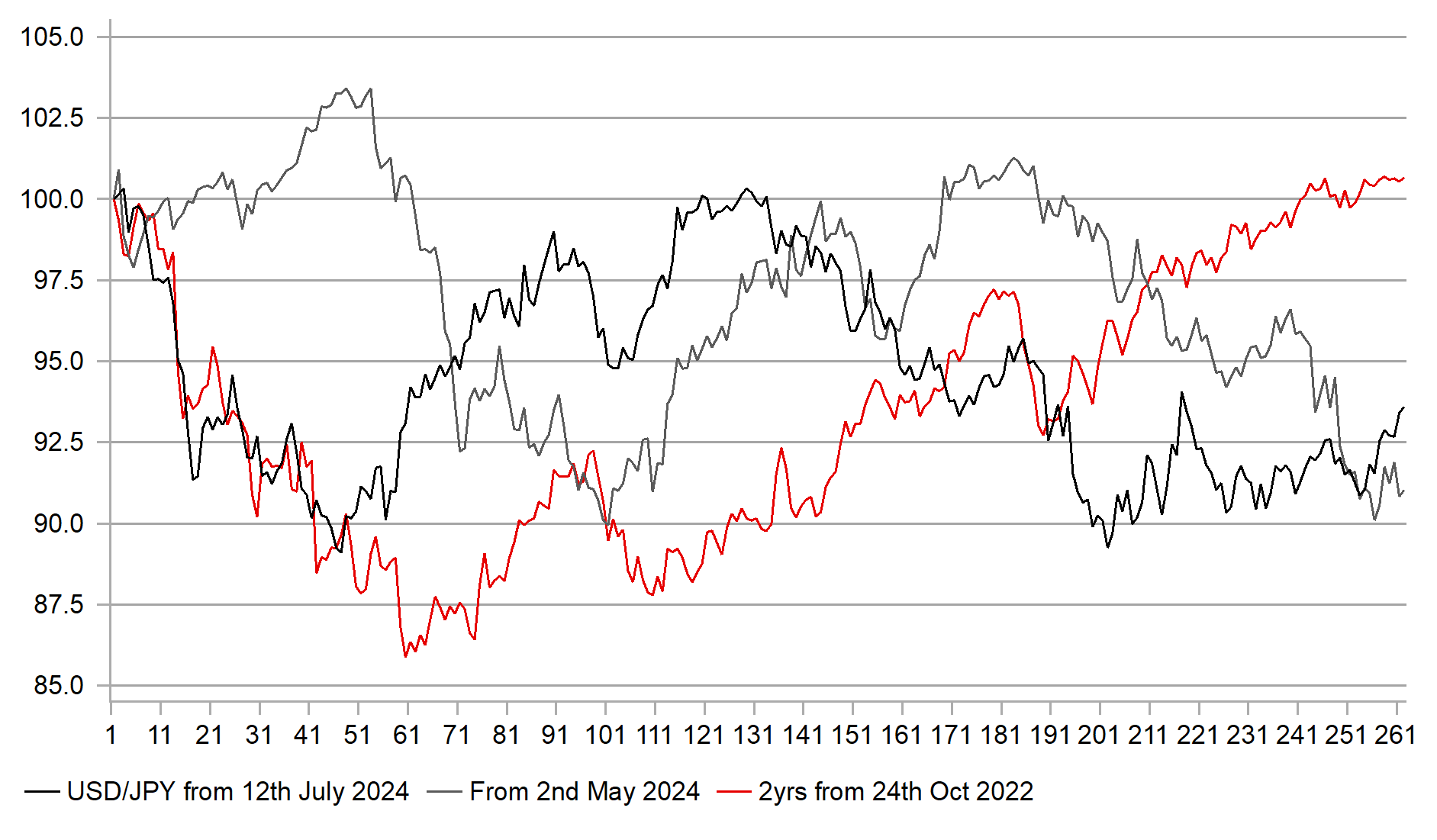

But there is a danger that the tone of communication by the BoJ next week fuels a renewed bout of yen selling that sees USD/JPY break more notably above the 160-level that in turn tests the resolve of the MoF to curtail yen selling. Finance Minister Katayama spoke today at an event in Tokyo and made clear that the MoF is ready and very focused on taking “bold action” against speculative moves. Katayama was also very keen to convey the message that Japan and the US are in very close contact “24 hours a day” and that Japan had a “free hand” on taking action.

The tone of Governor Ueda’s comments at the press conference following the meeting on Tuesday will be key for yen moves. There is an impression that the government want policy kept loose but the rising inflation risks will see that stance increasingly questioned by the markets. A hawkish tone we believe is important given there is about 18bps of tightening priced for the following meeting in June. The real policy rate remains deeply negative and that will likely encourage yen selling despite the threat of intervention. Katayama stated today that past intervention had an influence “every time”. Yes, but the influence varied in terms of time.

The three episodes of intervention in the most recent periods (Oct 2022; May 2024; and July 2024) all faded over time and that is primarily down to the fundamental backdrop being consistent with yen weakness. A BoJ that remains sidelined as inflation moves higher will be another signal that the fundamental backdrop hasn’t changed.

PAST INTERVENTIONS ONLY HAVE TEMPORARY IMPACT ON USD/JPY

Source: Bloomberg, Macrobond & MUFG GMR

USD: Inflation will be a bigger problem soon

The ceasefire that is currently being maintained can certainly be viewed as a de-escalation from the more intense phase of the military conflict but keeping the US blockade in place essentially means the risks continue to build of a significant spike in prices. That risk and the scale of the inflation impact continue to increase, and this risk looks to be increasingly underpriced. The FT ran a great article yesterday highlighting the impact on the agricultural sector in the US where record price increases are being recorded for certain products. The price of nitrogen fertiliser is up more than 30% while urea (a nitrogen-based fertiliser) is up 47%, a record rise. Farm diesel is up 46% and these price changes will inevitably soon start to impact the price of food for consumers. So this remains an issue of time and if President Trump’s strategy is to squeeze Iran dry of energy revenues, then time will be required, which we would argue President Trump doesn’t have. These prices are likely to get worse over the coming weeks if the Strait of Hormuz remains closed – our assumption based on crude oil prices average USD 115pbl in Q2 would see annual inflation pick up to around 3.6% in Q2 to 3.8% in Q3 and Q4 this year. The impact on refined fuels and fertiliser prices could mean these estimates are too low.

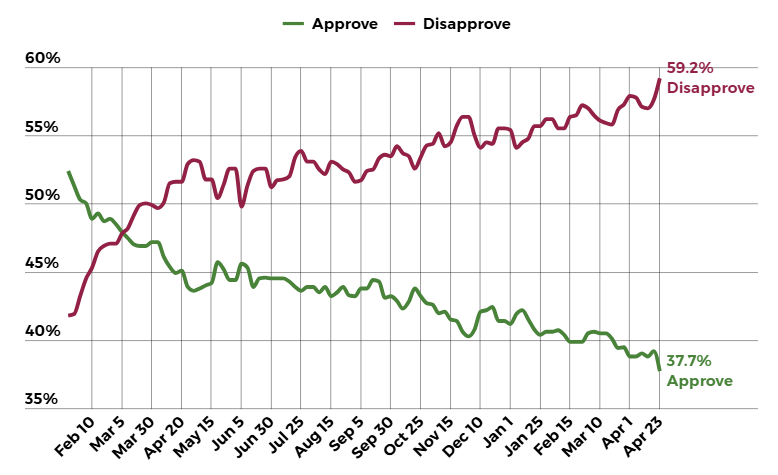

President Trump came to power on a mandate that included the promise of bringing down the cost of living and no more foreign wars. The net approval is now at -21.5% and has been in steady decline but has recently seen the drop accelerate. That is clearly down to the increased unpopularity of the war as inflation pressures continue to build. Iran’s strategy is very likely to wait-it-out and see the damage on the US economy increase further. This will have implications for inflation globally too of course and for Europe we maintain that the ECB and BoE will be quicker to act than the Federal Reserve which will continue to weigh on US dollar performance, especially under circumstances of equity market resilience continuing

PRESIDENT TRUMP’S POPULARITY CONTINUES TO DECLINE WITH NET APPROVAL AT A RECORD LOW IN THIS TERM OF OFFICE

Source: Race to the White House – www.racetothewh.com

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

DE |

09:00 |

German Ifo Business Climate Index |

(Apr) |

85.7 |

86.4 |

!! |

|

CH |

09:00 |

SNB Vice Chairman Schlegel Speaks |

- |

- |

- |

! |

|

CA |

13:30 |

Retail Sales (MoM) |

(Feb) |

0.9% |

1.1% |

!! |

|

US |

15:00 |

Michigan Consumer Sentiment |

(Apr) |

47.6 |

53.3 |

!! |

Source: Bloomberg & Investing.com