USD rebounds alongside price of oil to reflect risk of longer supply disruption

USD/NOK: Fears over longer energy supply disruption lifts USD & NOK

The US dollar has continued to trade at stronger levels overnight after rebounding yesterday in response to fears over the risk of more prolonged peace talks between the US and Iran to end the conflict and reopen the Strait of Hormuz. At the same time, the price of Brent crude oil has risen back above USD100/barrel. The main beneficiary from higher energy prices amongst G10 currencies continues to be the Norwegian krone which extended its advance yesterday to over 2% against the US dollar since the conflict started in late February. EUR/NOK has fallen to its lowest level since February 2023. Energy prices and the krone have been lifted over the last 24 hours by the failure of the US and Iran to hold fresh talks. White House press secretary Karoline Leavitt told reporters that President Trump “has not set a firm deadline to receive an Iranian proposal”. Vice President JD Vance had been set to fly to Islamabad to resume discussions before it became clear that Iran would not send its own delegation. Without fresh talks the Strait of Hormuz remains effectively closed which increases the risk of a more disruptive outcome for the global economy. Both the US and Iran claim that they are responsible for closing the Strait. There were further reports yesterday that Iranian gunboats fired on a cargo and container ship in the Strait. The moves highlight Iran’s aggressive stance in the face of US pressure at a time when talks between the two sides are in limbo.

At the same time, a more prolonged disruption of energy supplies from the Middle East is raising concerns about access to US dollar liquidity. It was reported earlier this week that the UAE had informally inquired about potential financial lifelines, including a currency swap, if the economic and financial impact of the war worsens. US President Trump then told CNBC that a currency swap with the UAE is under consideration. UAE’s foreign minister has since stated that “any suggestion that the UAE requires external financial backing misreads the facts” while highlighting the UAE is underpinned by more than USD2 trillion in sovereign investment assets and over USD300 billion of foreign exchange reserves. However, Treasury Scott Bessent added yesterday that many of their Persian Gulf allies along with a number of Asian nations have also requested foreign exchange swap lines with the US. He noted that “swap lines, whether it’s from the Federal Reserve or the Treasury, are to maintain order in the dollar funding markets and prevent the sale of US assets in a disorderly way”. One of is his goals is to “create a big dollar funding market in the Middle East” to lock in “dollar supremacy”. He indicated that the Treasury can do swap lines just like the Fed and “I think you’re going to see us doing swap lines with a whole cohort of new countries that the Fed doesn’t have swap lines with”. Finally, he emphasized that the US wants the UAE, Saudi Arabia and other Gulf countries to maintain their US dollar pegs.

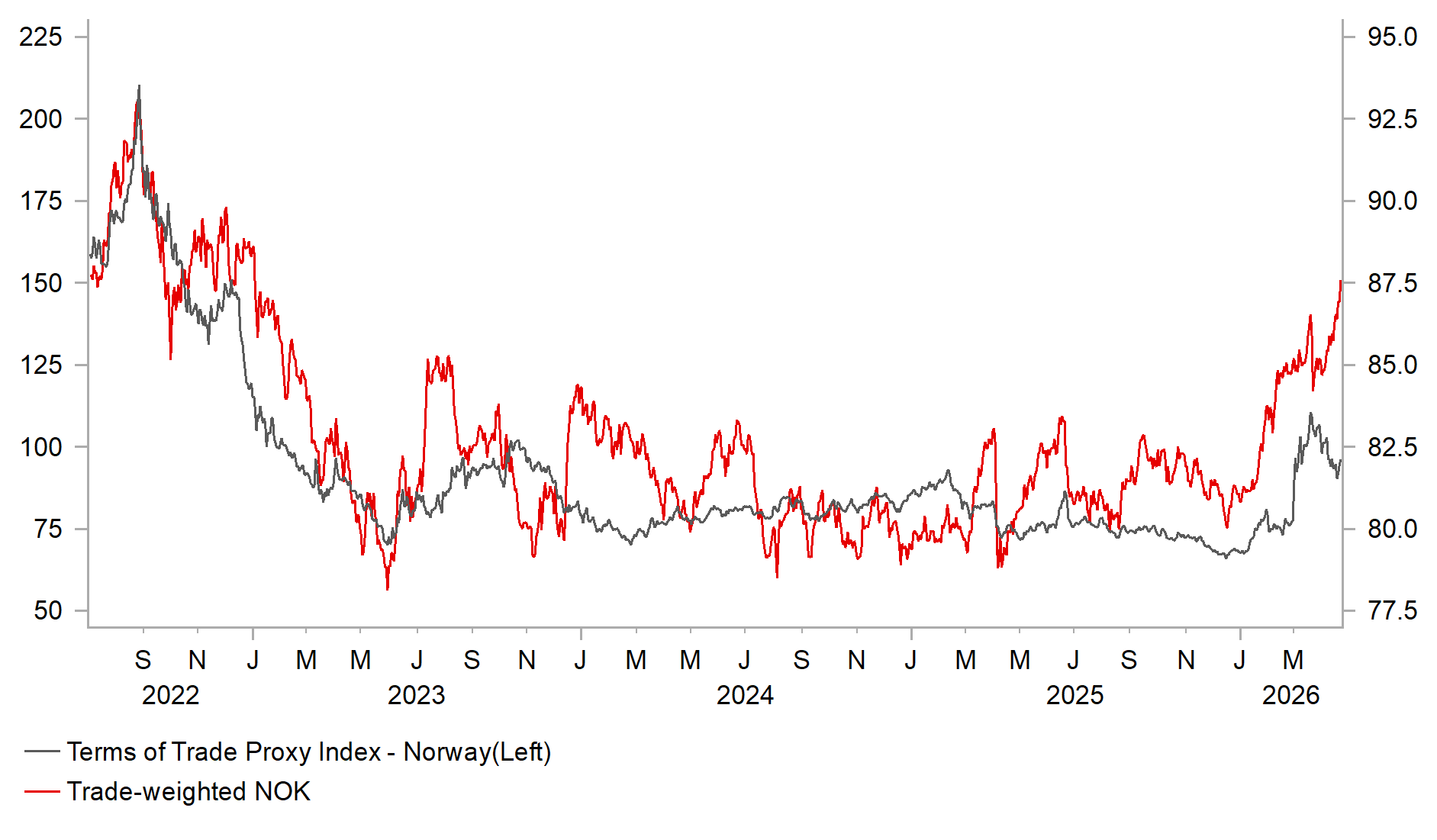

NOK HAS OUTPERFORMED DURING ENERGY PRICE SHOCK

Source: Bloomberg, Macrobond & MUFG GMR

EUR: ECB is still weighing up policy response to energy price shock

The euro has weakened against the US dollar falling back below 1.1700 overnight. The euro has been mainly undermined by the pick-up in energy prices. Market participants will be closely watching the releases of the latest euro-zone PMI surveys this morning for April to better assess the initial negative impact of the energy price shock on the economy. The euro-zone composite PMI is expected to drop back closer to the 50.0-level in April which would indicate that growth is starting to stagnate, and would be the lowest reading in a year. The energy price shock is expected to deliver a stagflationary shock for the euro-zone economy with growth slowing and inflation moving above target.

Bloomberg reported yesterday that ECB officials say that it is too early to decide on rate hikes as soon as next week. Greek central bank Governor Yannis Stournaras stated that “we should wait” citing “uncertainty and the high hopes that this war might end soon”. It was a view shared by Lithuanian central bank Governor Gediminas who stated that “I am of the opinion that we really shouldn’t increase interest rates at the next policy meeting”. ECB Chief Economist Philip Lane added as well that “no one really knows how long the situation will last and by the time of next week, I doubt we’re gonna have clarity on that”. He believes that “until we know more how long this war is going to last, it is really hard to know whether this is going to prove to be a temporary phase or a much bigger shock to the European economy”.

The comments are in line with current euro-zone rate market expectations for the ECB to wait until the June policy meeting to begin raising rates. There are only 3bps of hikes priced in for next week. The ECB wants more time to gather more data to better assess the risk of second round effects from higher energy prices and de-anchoring of inflation expectations. President Lagarde has stated that the economy is somewhere between their baseline and adverse scenario. In the base line scenario the ECB outlined that they would leaves rates on hold whereas the adverse scenario called for “measured” tightening. We still expect the ECB to deliver 50bps of hikes supporting the euro.

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EZ |

09:00 |

Services PMI |

(Apr) |

49.8 |

50.2 |

!!! |

|

EZ |

09:00 |

Manufacturing PMI |

(Apr) |

50.9 |

51.6 |

!!! |

|

GB |

09:30 |

Services PMI |

(Apr) |

50.0 |

50.5 |

!!! |

|

GB |

09:30 |

Manufacturing PMI |

(Apr) |

50.3 |

51.0 |

!!! |

|

US |

13:30 |

Initial Jobless Claims |

- |

211K |

207K |

!!! |

|

US |

14:45 |

Services PMI |

(Apr) |

50.5 |

49.8 |

!!! |

|

US |

14:45 |

Manufacturing PMI |

(Apr) |

52.5 |

52.3 |

!!! |

Source: Bloomberg & Investing.com