Warsh signals change on the way

USD: Warsh signals change but independent of Trump

As we await the developments from Islamabad and whether we are progressing toward de-escalation or re-escalation, the US dollar has strengthened on the back of the testimony from Kevin Warsh to the Senate Banking Committee in Congress yesterday. The moderate strength of the dollar no doubt reflects the building risk of renewed military conflict with crude oil prices drifting higher but there was also strong push-back from Warsh regarding suggestions that he would simply follow President Trump’s orders to cut rates. Of course, you wouldn’t expect otherwise from Warsh at this stage but his comments on balance sheet policy were perhaps a little stronger and more explicit than expected and firmly now strengthens the prospect of balance sheet shrinkage under a Warsh-led Federal Reserve.

But how quickly Warsh could go down that avenue remains unclear. A smaller balance sheet would likely require coordination on changes to bank regulation to reduce the current need for commercial banks holding large amounts of reserves. Warsh also stated yesterday that rate moves and balance sheet size should work in concert which would further imply that balance sheet shrinkage may not be on the agenda at the beginning of Warsh’s role as Fed Chair. Warsh also made clear that the Fed should not hold long-term bonds which could shape expectations of a composition change if the size of the balance sheet can’t be addressed over the short-term. Bond investors often need to take long-term views when investing further out the curve and it was very clear yesterday that change is coming regarding balance sheet policy and that is something that could certainly curtail underlying demand for longer-term US Treasury bonds.

What was also interesting yesterday was the strong message on guidance. Warsh doesn’t like guidance and that spells the end of two current aspects of Fed policy. Firstly, the median dots profile published four times a year and secondly, the extensive scheduling of Fed speeches. Strong guidance helps deliver the changes ahead of delivery of a policy change and helps reduce surprises and hence reduces volatility. Less guidance and generally less information increases uncertainty (certainly as the new regime kicks into gear) that leads to greater volatility that likely results in some added term premium.

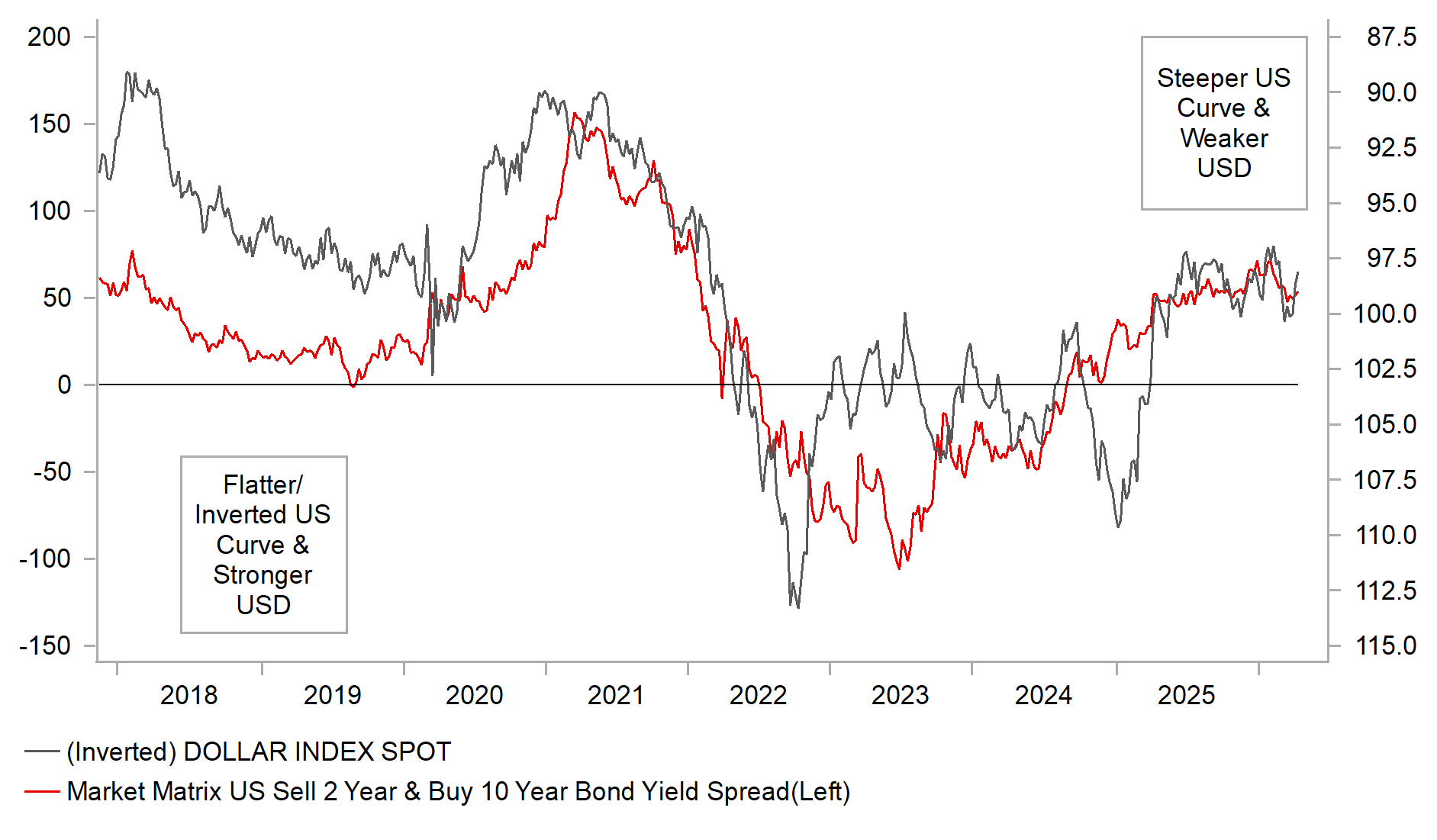

So, both the signals from Warsh on Fed balance sheet policy and on providing forward guidance indicate to us the potential for a steeper Treasury yield curve. That wasn’t the move we got yesterday – in fact there was a mild flattening – with perhaps Warsh’s strong words on not being dictated by Trump to cut rates helping to keep front-end yields higher. Our key conclusion is that over time investors need to get used to a less predictable Fed and at the same time the uncertainty related to a potential new framework for dealing with inflation. That mix coupled with the unpredictability coming from the White House does not suggest a positive backdrop for the dollar.

WARSH CHANGES COULD LEAD TO STEEPER CURVE AND WEAKER DOLLAR

Source: Bloomberg, Macrobond & MUFG GMR

USD: Ceasefire extended but risks are rising

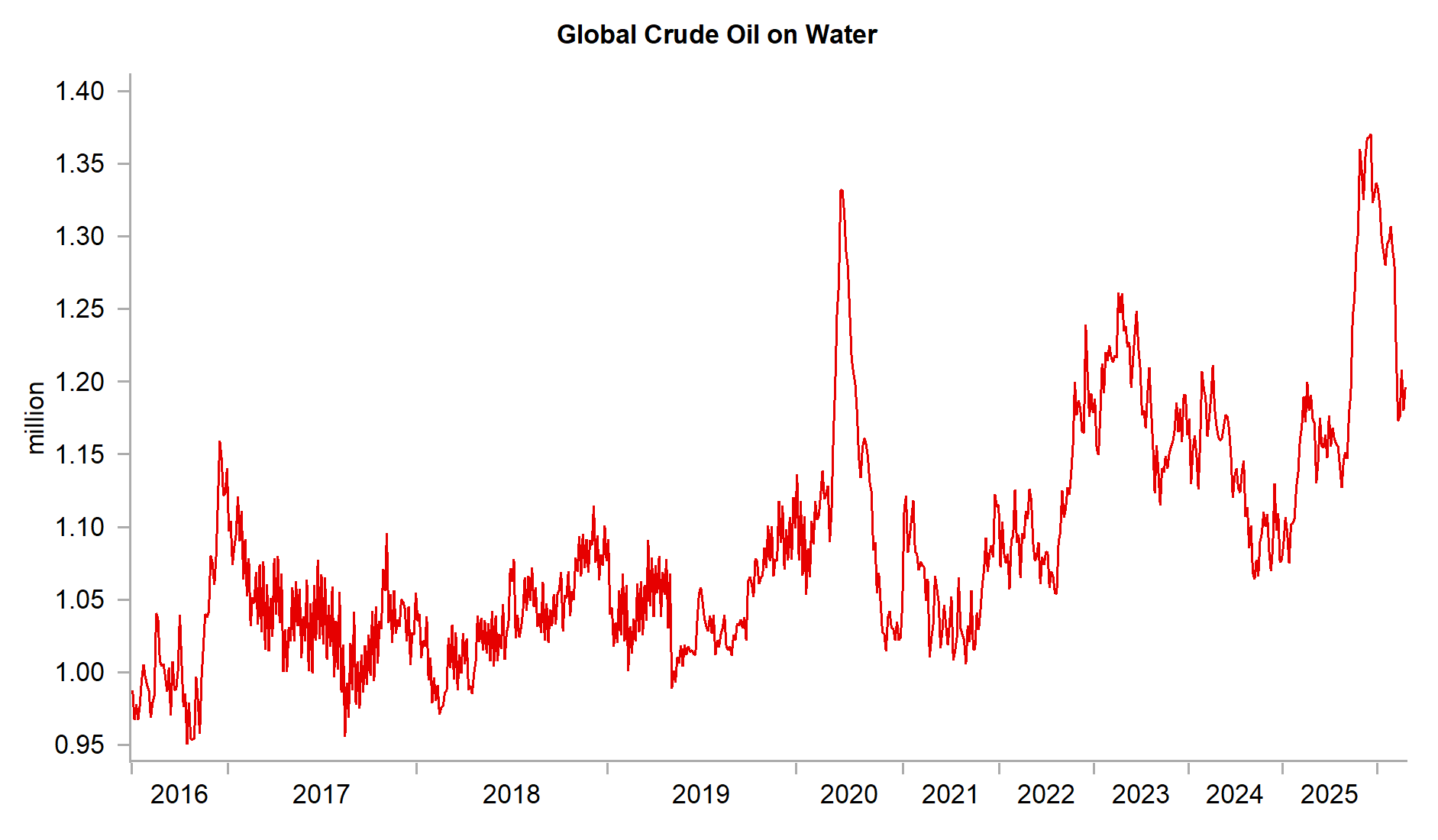

President Trump’s extension of the ceasefire yesterday has brought limited relief for financial market participants with crude oil prices remaining elevated close to USD 100pbl as both Iran and the US accuse each other of breaches to the ceasefire deal. President Trump has refused to end the blockade that Iran describes as a breach while UK Maritime Trade Operations reported that a container ship had been attacked off the cost of Oman. US equities finished lower yesterday and Asian equity markets are mixed today with definite indications that risk conditions, while resilient, have deteriorated with prospects of progress in negotiations looking bleak. One reason for the extension of the ceasefire by the US was to allow for a “unified” proposal to made by the Iranians and if there are divisions in Iran over next steps that does increase the risk of limited progress. Iran appears reluctant to proceed with further talks until the US acknowledges what Iran views is the primary breach of the ceasefire – the US blockade of the Strait of Hormuz. There was a BBC report suggesting the US would lift the blockade but that has yet to happen.

So for now the financial markets remain in limbo, awaiting news on whether there will be progress or whether another wave of military attacks lie ahead. Iran has threatened energy production facilities in the region stating its neighbours can “wave good-bye” to oil production in the region if the US resumes military attacks. We are surely on the cusp of another surge in crude oil prices of this ceasefire does not hold and that will most likely have a more notable knock-on impact on risk assets. While the US dollar has not strengthened to the degree we would have expected, a more meaningful risk-off would likely see a more significant rebound of the dollar.

THE STOCK OF CRUDE OIL ON WATER IS DIMINISHING INDICATING INCREASED RISKS OF PRICE SURGE

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

08:40 |

ECB's Lane speaks in Frankfurt |

!!! |

|||

|

UK |

09:05 |

BoE Deputy Governor Breeden speaks |

!!! |

|||

|

UK |

09:30 |

House Price Index YoY |

Feb |

1.3% |

!! |

|

|

EC |

11:00 |

ECB's Kocher speaks |

! |

|||

|

EC |

13:15 |

ECB's Lane speaks in Frankfurt |

! |

|||

|

EC |

15:00 |

Consumer Confidence |

Apr |

-17.2 |

-16.3 |

! |

|

EC |

18:00 |

ECB's Nagel speaks |

!! |

|||

|

EC |

18:30 |

ECB's Lagarde speaks in London |

!! |

Source: Bloomberg & Investing.com