USD continues to firm after FOMC minutes & Nvidia earnings

USD: Fed minutes & Nvidia earnings in focus

The US dollar has continued to trade at stronger levels overnight supported by the recent adjustment higher in US yields. The 2-year US Treasury yield has increased by around 40bps from last month’s low as market participants have moved to price in a higher probability of multiple Fed rate hikes in response to the energy price shock. The release overnight of the minutes from the last FOMC meeting in April contained some relatively hawkish messages. We already knew that three Fed Presidents Beth Hammack, Lorie Logan and Neel Kashkari dissented against the decision to maintain an easing bias. The minutes added that “many” participants supported getting rid of the easing bias in April which was step up from “some” at the prior meeting. It will reinforce expectations that the Fed could drop their easing bias as soon as at the next policy meeting in June. Furthermore, a majority of FOMC members felt the need to indicate that they would be prepared to hike rates if inflation were to continue to run persistently above 2.0%. However, the Fed staff’s updated forecasts show inflation falling back to “close to 2.0%” next year in the base case scenario which does not currently support the case for higher rates. Overall, the minutes continue to show a gradual hawkish shift is underway at the Fed but does not fully back market expectations for multiple rate hikes. The recent appointment of Kevin Warsh as the new Fed chair adds to policy uncertainty arguing against putting too much weight on what happened at the last FOMC meeting when Jerome Powell was Fed chair.

The other main development overnight from the US was the release of the latest earnings report from Nvidia who reported record sales and earnings driven by surging demand for data-centre computing and the rise of AI agents. Nvidia’s sales for the April quarter reached USD81.6 billion up by 85% from a year ago. Net income was USD58.3 billion for the quarter, more than three times the result from a year earlier, and 36.5% higher than analysts had forecast. It was driven by sales of networking hardware which tripled from a year ago to a record USD14.8 billion. Nvidia also announced two shareholder-friendly changes; an USD80 billion share-buyback plan and an increase in the company’s quarterly cash dividend from one penny a share to 25 cents. CFO Collette Kress state that the company intends to return 50% of its free cash flow this year to shareholders. The report will boost investor confidence that the roll out of AI remains a tailwind for the global economy at time when it also facing an unprecedented energy supply shock. Buoyant global investor risk sentiment has worked against the US dollar recently even though US equities have performed strongly driven by AI-related stocks.

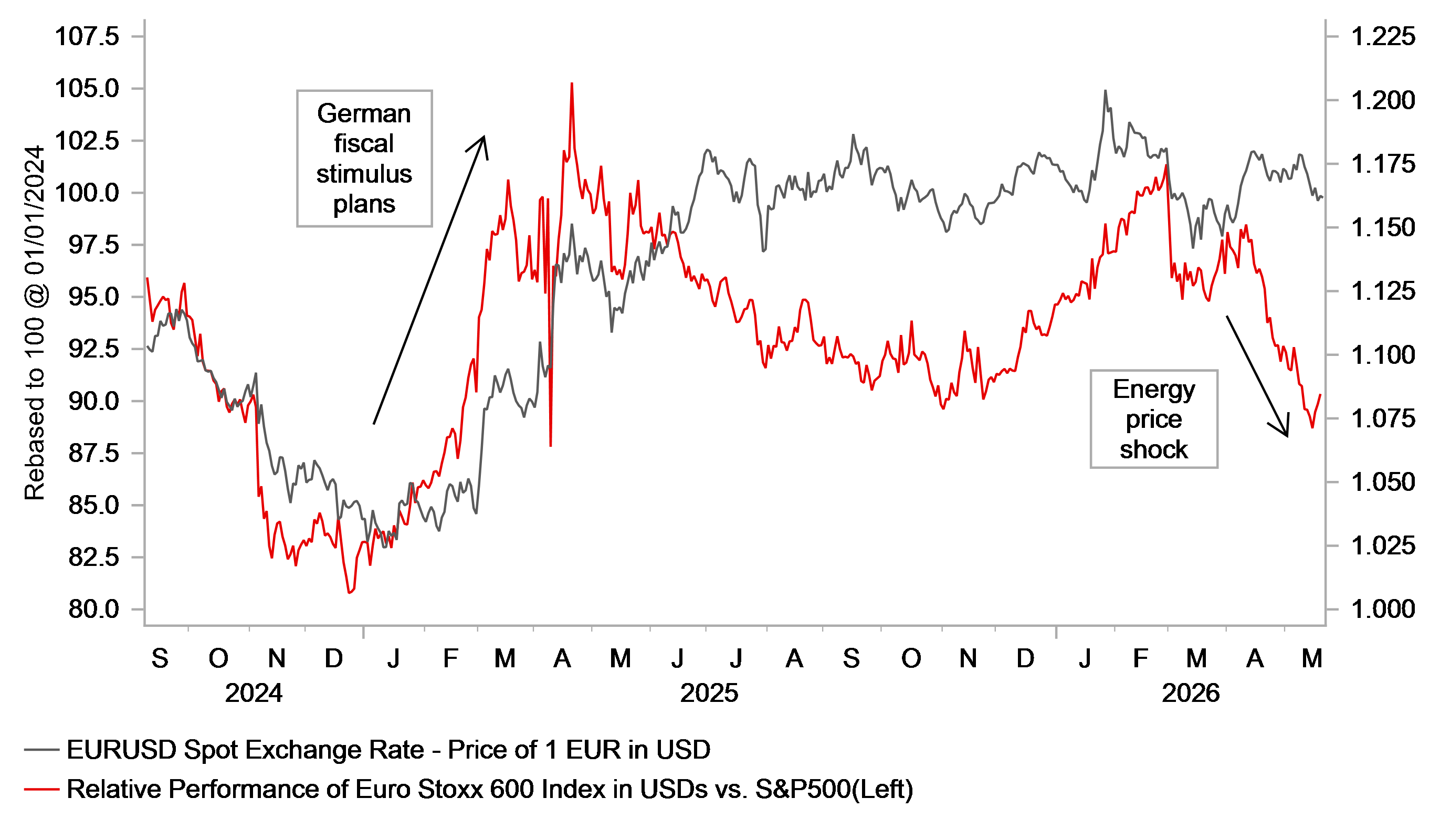

EUR/USD VS. RELATIVE EZ/US EQUITY MARKET PERFORMANCE

Source: Bloomberg, Macrobond & MUFG Research

GBP: Gilts & GBP rebound as UK fiscal & inflation persistence fears ease

The pound and gilts have staged an impressive rebound this week driven both by a reduction in fears over UK fiscal and inflation risks. After hitting a low of 1.3303 on 18th May, cable has risen back up towards the 200-day moving average at around 1.3420. The rebound for gilts has been even bigger with the 30-year yield dropping by around 20bps in recent days. The rebound for the pound and gilts was initially driven by reassuring comments from a spokesperson for Andy Burnham who is the front-runner to potentially challenge Keir Starmer if he wins the by-election in Makerfield. The spokesperson stated that Andy Burnham plans to stick the government’s current fiscal rules which would curtail room to loosen fiscal policy if he becomes prime minister. The policy “u-turn” helps to ease downside risks for the pound and gilts in the near-term.

The second positive surprise in quick succession was delivered yesterday by the release of the latest UK CPI report for April. The report revealed a much larger than expected drop in core and services inflation helping to ease some concerns over the risk of more persistent inflation in the UK. It provides some reassuring news that underlying inflation was continuing to slow before the energy price shock hits harder heading into the summer. It makes the UK looks less of an outlier in terms of higher inflation when compared to other major economies. The weakening UK labour market has helped to bring down wage growth. The latest labour market report released earlier this week revealed a surprisingly sharp drop in payrolled employment and further evidence of slowing wage growth. Admittedly, there were some one-off technical factors that likely exaggerated the scale of the monthly drop in CPI inflation payrolled employment .Please see our latest Focus report more details on the CPI report (click here).

In response to the softer CPI report, the UK rate market has moved to scale expectations for BoE rate hikes. The timing of the first rate hike has been pushed out until July or September, and there are only around 50bps of hikes priced in by year end. Market pricing is now more in line with our forecast for two hikes this year. Overall, the latest developments leave the pound on a stronger footing in the near-term but we still judge that risks remain tilted to the downside. The ongoing fallout from the energy price shock and lingering UK political uncertainty continue to pose downside risk for the pound.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 09:00 | Manufacturing PMI | (May) | 51.7 | 52.2 | !! |

EU | 09:00 | Services PMI | (May) | 47.8 | 47.6 | !! |

EU | 09:00 | Current Account | (Mar) | 26.3B | 24.9B | ! |

GB | 09:30 | Services PMI | (May) | 51.7 | 52.7 | !!! |

GB | 09:30 | Manufacturing PMI | (May) | 52.9 | 53.7 | !!! |

EU | 10:00 | Construction Output (MoM) | (Mar) | - | -0.19% | ! |

EU | 10:00 | Labor Cost Index (YoY) | (Q1) | - | 3.30% | ! |

GB | 11:00 | CBI Industrial Trends Orders | (May) | -40 | -38 | !! |

US | 13:30 | Philadelphia Fed Manufacturing Index | (May) | 17.6 | 26.7 | !!! |

US | 13:30 | Initial Jobless Claims | - | 210K | 211K | !!! |

US | 13:30 | Housing Starts | (Apr) | 1.420M | 1.502M | !! |

US | 13:30 | Philly Fed Business Conditions | (May) | - | 40.8 | ! |

US | 14:45 | Manufacturing PMI | (May) | 53.8 | 54.5 | !!! |

US | 14:45 | Services PMI | (May) | 51.1 | 51.0 | !!! |

GB | 16:00 | BoE Gov Bailey Speaks | - | - | - | !!! |

Source: Bloomberg & Investing.com