USD remains on softer footing in anticipation of further deescalation

USD: Warsh’s confirmation hearing to briefly take focus away from conflict

The US dollar has quickly given up gains recorded at the start of this week with the dollar index falling back towards the 98.000-level. The price action continues to highlight that the US dollar remains heavy after falling for three consecutive weeks. Despite the setbacks over the weekend including Iran firing on vessels in the Strait of Hormuz and the US taking over an Iranian ship, market participants remain optimistic that the Middle East conflict will continue to deescalate providing a headwind for US dollar performance. President Trump stated yesterday that it is “highly unlikely” that the two-week ceasefire will be extended if a more sustained peace deal can’t be reached in time. He has confirmed that the two-week ceasefire ends on “Wednesday evening Washington time” which buys a little more time for negotiations to take place. US officials including vice-president JD Vance are set to return to Islamabad for a second round of talks, but Iranian officials have not decided yet whether they will attend according to the FT. The talks are expected to take place either on Tuesday night or Wednesday morning. Bloomberg has reported that there is a divide between the IRGC’s leader Ahmad Vahidi and less ideological figures in Iran such as Iranian President Pezeshkian and Foreign Minister Araghchi who are more inclined to reach a deal with the US. Despite the divide, Bloomberg has reported that there’s still a good chance of a deal in the next few days that effectively ends the war, even if more negotiations are needed over nuclear and military issues according to officials. Market participants will also be watching closely to see how quickly traffic then normalizes through the Strait to ease global energy supply restrictions. With the US dollar already trading back close to levels prior to the Middle East conflict from late February, the announcement of a deal may not trigger another sharp sell-off for the US dollar.

Market attention will also focus on the outlook for Fed policy today when Kevin Warsh will testify before the Senate Banking Committee at the confirmation hearing to be the next Fed chair. It will be the first time that he has publicly spoken on the US economy and monetary policy since he was nominated by President Trump to the next Fed Chair. He has already released his opening statement ahead of the hearing. In the prepared remarks he emphasized that “monetary policy independence is essential” but added that “I do not believe the operational independence of monetary policy is particularly threatened when elected officials…state their views on interest rates”. Downplaying the impact of repeated interference from President Trump calling for lower rates. To sustain the Fed’s independence, he believes that the Fed must take responsibility for ensuring price stability “without excuse or equivocation, argument or anguish”. It must recognise that “peak” Fed independence applies only to the operational conduct of monetary policy, and the Fed “must stay in its lane” by not getting drawn into “fiscal and social policies where it has neither authority nor expertise” or act as “some general-purpose agency” of the US government. He favours a “clearer, cleaner match between the Fed’s powers and responsibilities” although did not explicitly mention the need for a new Fed-Treasury accord. It fits with market views that he is likely to pursue smaller Fed balance sheet.

While the comments are not surprising, they should provide further reassurance that he will defend the Fed’s independence and will not give in to President Trump’s calls for lower rates unless justified by economic fundamentals. The Q&A has the potential for market moving if he provides any insights into his latest thoughts on the economy and policy settings in light of the recent energy price shock. US rate market participants are of the view he will leave the door open for rate cuts later this year justified by the potentially disinflationary impact of higher productivity growth. If he sounds more hawkish than expected, it could offer some near-term support for the US dollar.

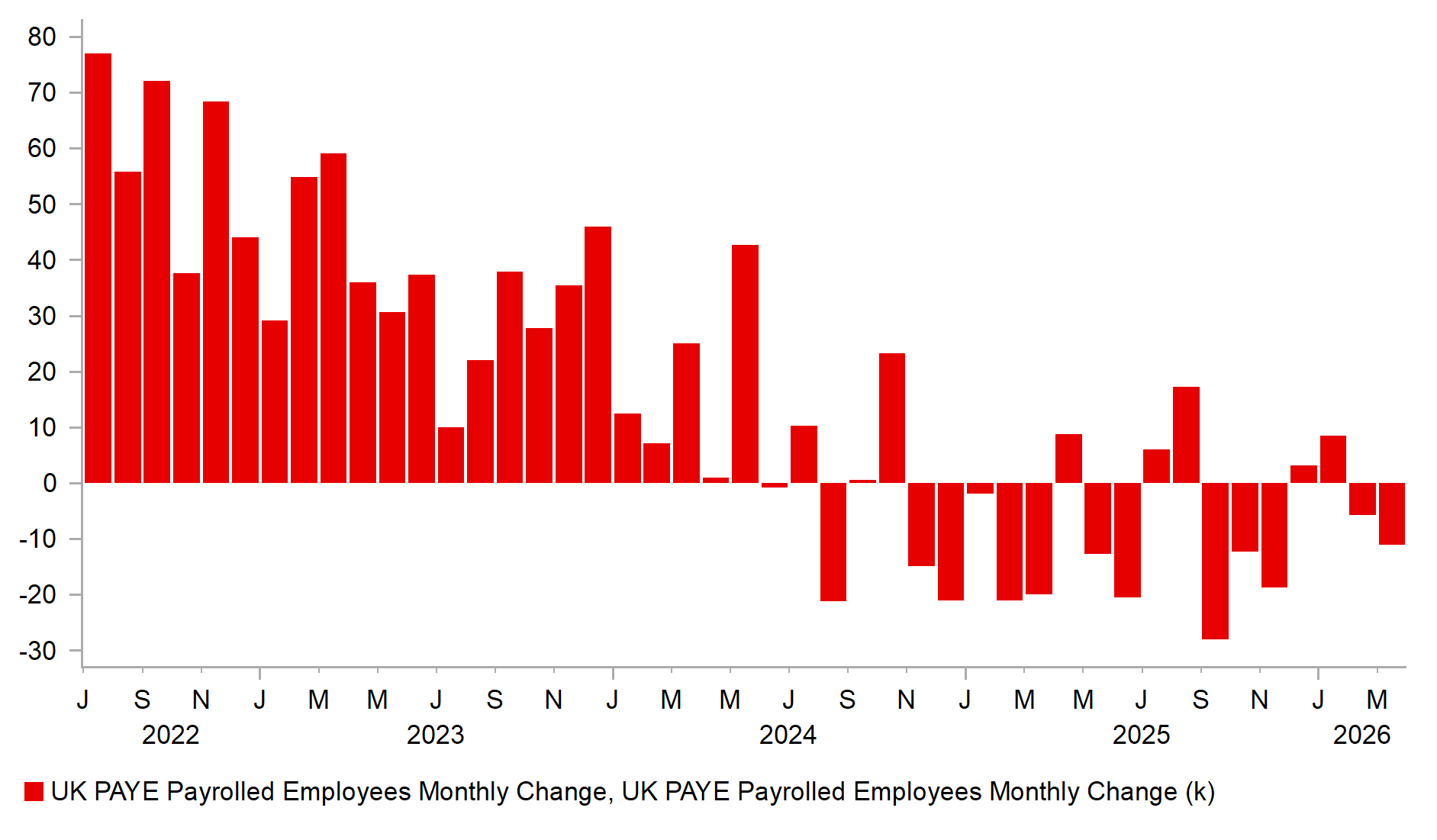

SOFT UK LABOUR MARKET HEADING INTO ENERGY PRICE SHOCK

Source: Bloomberg, Macrobond & MUFG GMR

GBP/NZD: Rate hike speculation builds in New Zealand but fades in UK

The main economic data release overnight was the release of the latest inflation report from New Zealand. The CPI report for Q1 revealed that headline inflation held above the RBNZ’s 1%-3% target band at 3.1%. Headline inflation is expected to rise further above target in the coming quarters in response to the energy price shock. Higher electricity prices already accounted for more than a tenth of the annual increase in headline inflation in Q1. The RBNZ is expected to raise their inflation forecasts at their next policy meeting on 27th May. The stronger inflation print has encouraged market participants to price in more RBNZ rate hikes helping to strengthen the kiwi. NZD/USD is currently attempting to break back above the 0.5900-level. A 25bps hike is now fully priced in by the July policy meeting.

The other main economic data release has been the latest UK labour market report this morning. The report has added to caution over the health of the labour market by revealing that payrolled employees fell by -11k in March, and the prior month’s increase of +20k was revised away to a contraction of -6k. Private sector wage growth excluding bonuses also slowed to 3.2% down from 3.3% moving closer to rates that are more consistent with meeting the BoE’s inflation target. The soft labour market prior to the energy price shock provides some reassurance over the upside inflation risks which alongside the already restrictive policy rates argues against more aggressive BoE rate hikes. We are currently forecasting only one rate hike from the BoE. The recent scaling back of more aggressive BoE rate hike expectations has helped to dampen pound strength.

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

DE |

08:30 |

German Buba President Nagel Speaks |

- |

- |

- |

!! |

|

EU |

09:00 |

ECB's De Guindos Speaks |

- |

- |

- |

!! |

|

CH |

09:00 |

M3 Money Supply |

(Mar) |

- |

1,216,014.0B |

! |

|

DE |

11:00 |

German ZEW Economic Sentiment |

(Apr) |

-6.7 |

-0.5 |

!! |

|

US |

14:15 |

ADP Employment Change Weekly |

- |

- |

39.30K |

!! |

|

US |

14:30 |

Retail Sales (MoM) |

(Mar) |

1.4% |

0.6% |

!!! |

|

US |

15:00 |

Fed Chair Nominee Warsh Testifies |

!!! |

|||

|

US |

16:00 |

Pending Home Sales (MoM) |

(Mar) |

0.0% |

1.8% |

!! |

|

US |

20:30 |

Fed Waller Speaks |

- |

- |

- |

!! |

Source: Bloomberg & Investing.com