Weak UK labour data dampens relief rebound for GBP after policy “u-turn”

AUD/USD: Weak China growth & RBA pause weigh on Aussie

The major foreign exchange rates have traded within tight ranges overnight with the US dollar remaining close to recent highs. The biggest mover among G10 currencies has been the Australian dollar which has weakened by over 0.5% against the US dollar. High beta currencies such as the Australian dollar have weakened overnight even though President Trump called off fresh military strikes on Iran after an appeal by leaders of Persian Gulf allies, who called for more time to pursue a diplomatic resolution. At a White House event yesterday he stated “I put it off a little while, hopefully maybe forever, but possibly for a little while, because we’ve had very big discussions with Iran, and we’ll see what they amount to”. “I was asked by Saudi Arabia, Qatar, UAE and some others if we could put it off for two or three days, a short period of time, because they think that they are getting closer to making a deal”. President Trump has repeatedly threatened to restart military action to place more pressure on Iran to make a deal but so far a deal remains elusive to end the conflict and re-open the Strait. It follows reports earlier in the day that a fresh proposal delivered by Iran lacked meaningful improvement, failing to offer detailed commitments to surrender their stockpile of highly enriched uranium according to Axios.

The Australian dollar has underperformed at the start of this week undermined both by the release of softer activity data from China and the latest minutes from the RBA’s policy meeting earlier this month. The latest monthly activity data from China revealed that the economy slowed more sharply than expected in April. The slowdown was broad-based with annual retail sales growth slowing to just 0.2% in April down from 1.7% in March, and industrial production growth slowing to 4.1% in April down from 5.7%. More worrying was the contraction in fixed-asset investment excluding rural areas by an annual rate of -1.6% in the first four months of this year. The loss of growth momentum in China will increase pressure on domestic policymakers to provide additional stimulus to support growth. At the same time, it will dampen expectations for further renminbi strength in the near-term when USD/CNY is attempting to break below the 6.8000-level. Evidence of softer domestic demand in China has also weighed on the Australin dollar. After failing to hold above the 0.7200-level, AUD/USD is correcting lower reinforced by the latest RBA minutes indicating that board members agreed that a hike earlier this month “would give the broad space to see how the conflict in the Middle East develops and how households and businesses respond”. The minutes have supported market expectations that the RBA will leave rates on hold at their next meeting in June.

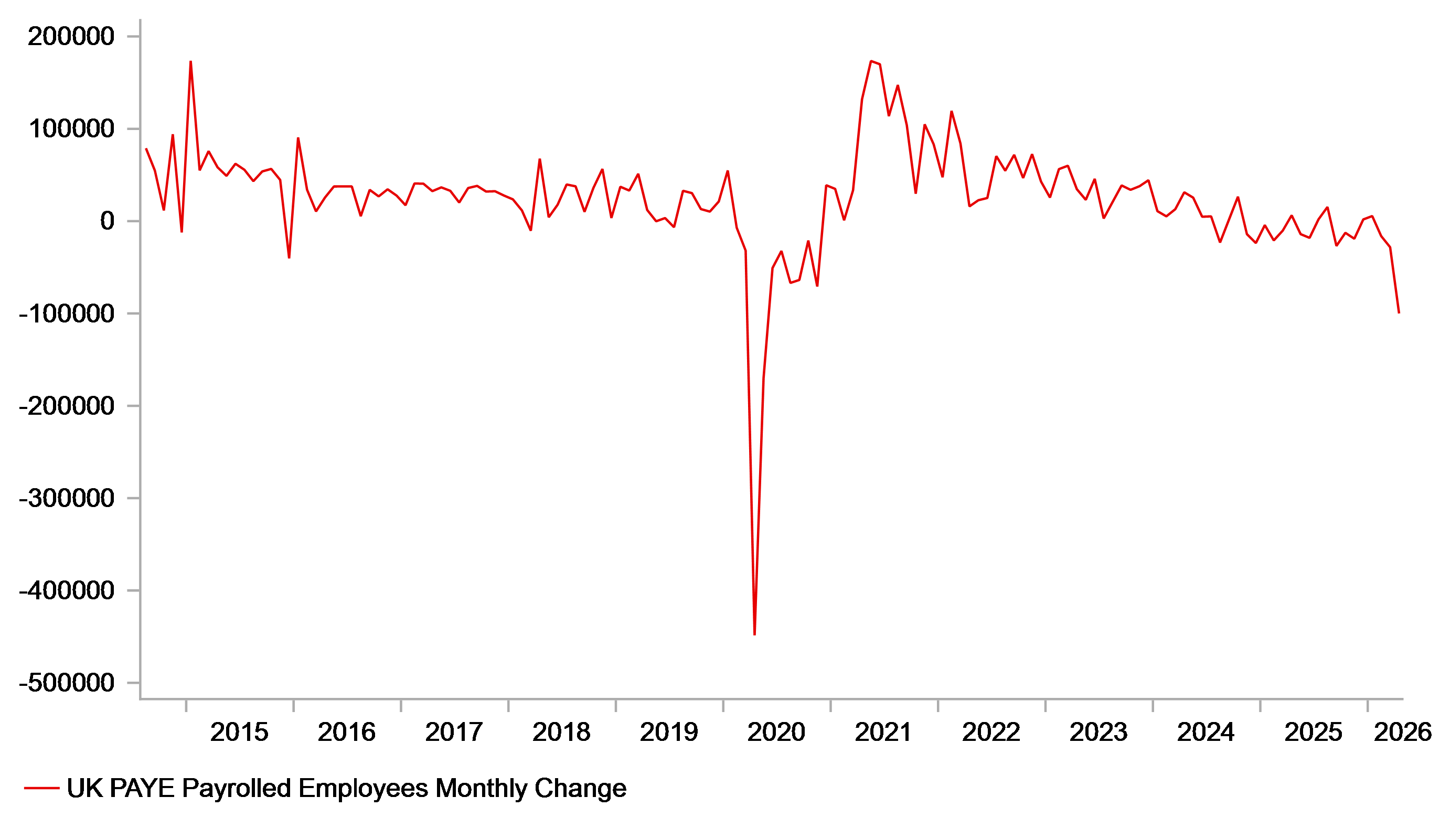

DOES EMPLOYMENT DATA OVERSTATE UK LABOUR MARKET WEAKNESS?

Source: Bloomberg, Macrobond & MUFG Research

GBP: Fiscal policy “u-turn” provides relief for gilts & GBP

The pound has staged a strong rebound over the last twenty four hours resulting in cable rising back above the 1.3400-level after hitting a low yesterday at 1.3303. The main trigger for the reversal higher for the pound were reassuring reports that potential Labour leadership candidate Andy Burnham has reportedly ruled out changing the government’s self-imposed fiscal rules according to one of his spokepersons. The comments will be viewed as an attempt to reassure investors that he will not seek to significantly loosen fiscal policy if he becomes prime minister. Under the current rules, the chancellor must balance day-to-day spending with tax revenues by 2039/30 and reduce debt – as measured by public-sector net financial liabilities – as a share of GDP by the same point. The rules in their current form would continue to act as a restraint on government spending. One can assume that the recent negative gilt market reaction is already putting pressure on Andy Burham to adjust his policy agenda. It stands in marked contrast to his comments from last year when he stated that Labour had to “get beyond this thing of being in hock to the bond markets”. He had also advocated increasing public investment by GBP40billion and excluding defence spending from the fiscal rules. The apparent fiscal policy “u-turn” should help to ease downside risks for gilts and the pound in the near-term from heightened political uncertainty in the UK. He has also performed another apparent “u-turn” by stating “I am not proposing that the UK considers rejoining the EU” as he attempts to win the by-election in Makerfield and faces strong competition from Reform.

However, the relief rebound for the pound has been dampened this morning by the release of much weaker than expected UK labour market data. The report revealed that payrolled employment contracted sharply by -100k in April following on from a larger fall of -28k in March. It was the biggest drop since the COVID shock in 2020. The ONS notes that early months in the tax year carry a greater degree of uncertainty. It is likely that the April figures overstates the underlying scale of labour market weakness, although the report as a whole is consistent with ongoing slack labour market slack. It will put a dampener on near-term market expectations for BoE rate hikes in response to the energy price shock. The UK rate market is still expecting a hike at the July MPC meeting indicating that market participants are not putting too much weight on the outsized drop in employment today.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

GB | 09:10 | BoE Breeden Speaks | - | - | - | ! |

GB | 09:30 | Labour Productivity | (Q4) | - | 1.1% | !! |

EU | 10:00 | Trade Balance | (Mar) | 5.4B | 11.5B | !! |

EU | 13:00 | ECB's Lane Speaks | - | - | - | !! |

US | 13:00 | Fed Waller Speaks | - | - | - | !! |

CA | 13:30 | CPI (YoY) | (Apr) | 3.1% | 2.4% | ! |

Source: Bloomberg & Investing.com