Scope of US dollar appreciation has limits

USD: MoU doubts sees oil rebound

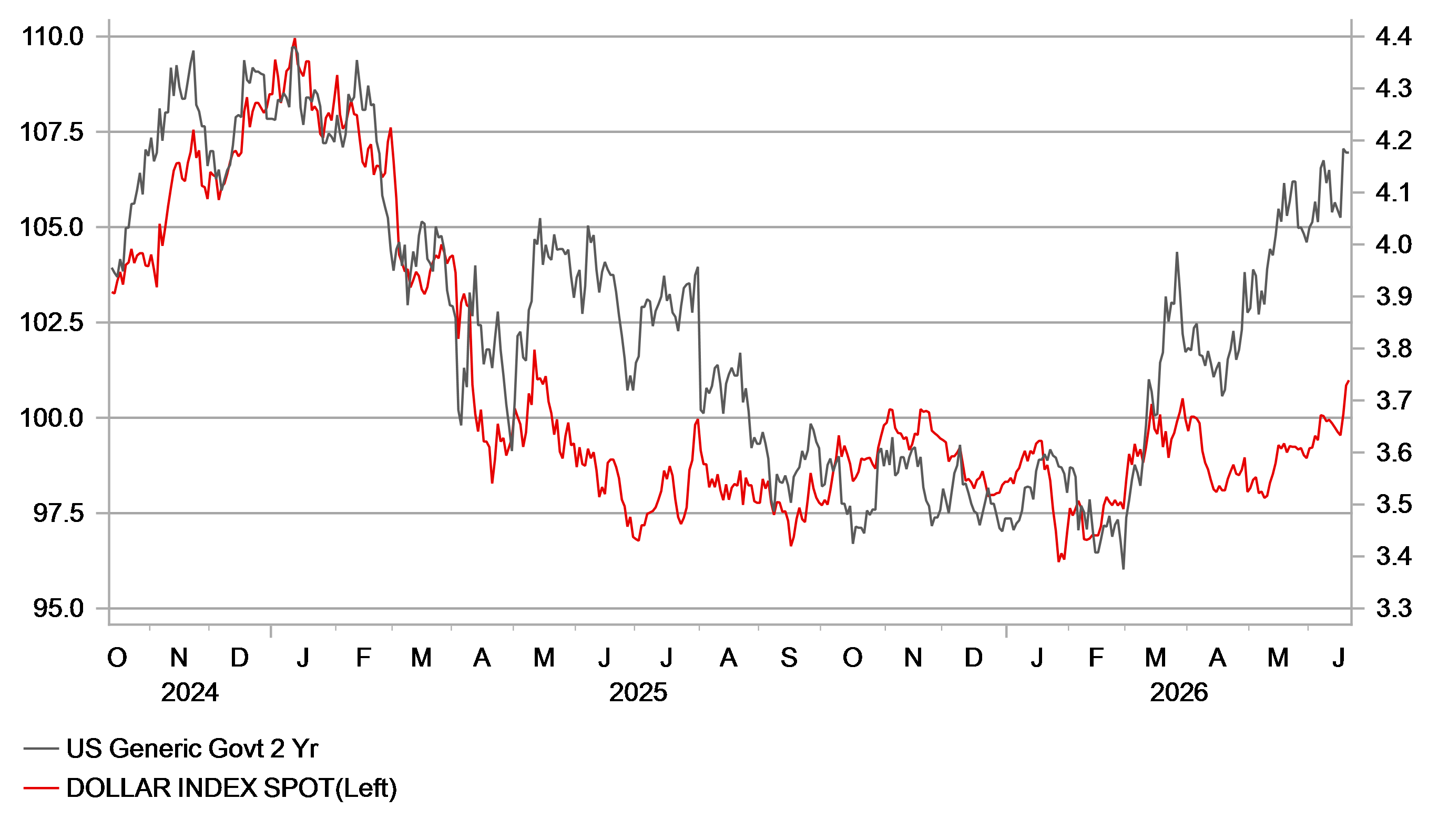

The US dollar (DXY) has advanced further to a level not seen since May 2025 with the substantial hawkish shift from the Fed this week continuing to reinforce positive momentum. In the three days since the Fed meeting, the dollar is 1.5% stronger. The momentum is being helped by the postponement of the signing of the MoU in Switzerland after Iran pulled out, accusing Israel of breaching the deal by attacking Lebanon. The hit to risk appetite has been modest however and it looks unlikely that this decision by Iran will derail the process. Israel is now under considerable pressure (explicit criticism from VP JD Vance) to avoid attacks on Israel and the rebound in crude oil prices has been modest. Brent is now unchanged on the day and remains close to 30% lower over the last month.

Over the short-term, the US dollar can certainly extend further. The shift in the dots was the most significant since the dots were first published in 2012. This largest ever hawkish shift in the dots came at a time when the risks to inflation have receded markedly given the plunge in crude oil prices. The IEA Monthly Report released this week also highlights the prospects of an over-supplied market potentially driving prices further lower. The drop over the last month can also be explained by the fact that traffic through the Strait of Hormuz was already picking up notably in May/June. The IEA estimated that shipments through the SoH, supported in part by ship-to-ship transfers in the Gulf of Oman, increased from 9.6 mb/d in May to around 12 mb/d in early June. Supply constraints were also eased by the fact that crude imports into China and Japan declined sharply, each falling by around 40% as both countries tapped large strategic reserves. The IEA also estimated that in 2027 crude oil balances would show a “significant overhang” with demand rising by 2 mb/d to 105.3 mb/d but supply increasing by 8 mb/d to 110 mb/d.

If the deal between the US and Iran is done and holds, the disinflation impetus from energy could be very considerable by year-end and into 2027. Inflation in the US is likely at around the peak so the scenario of the Fed having to hike rates still looks very unlikely to us.

We understand the positive momentum for the dollar following the record hawkish shift in the dots but it still doesn’t really tally that it leads to a rate hike. On the other hand, the ECB could well see the benefit of hiking again. The difference between the ECB and the Fed is the policy setting level and the mandate. Chief Economist Philip Lane stated yesterday the “upper end of the range of neutral” had crept up to 2.50% which could provide the justification for a further hike given the ECB has a single price stability mandate. We still see greater upside scope for EUR/USD later in the year.

DXY BREAKING HIGHER AS FOCUS SHIFTS TO YIELD

Source: Bloomberg, Macrobond & MUFG Research

CHF: Limited scope for franc depreciation

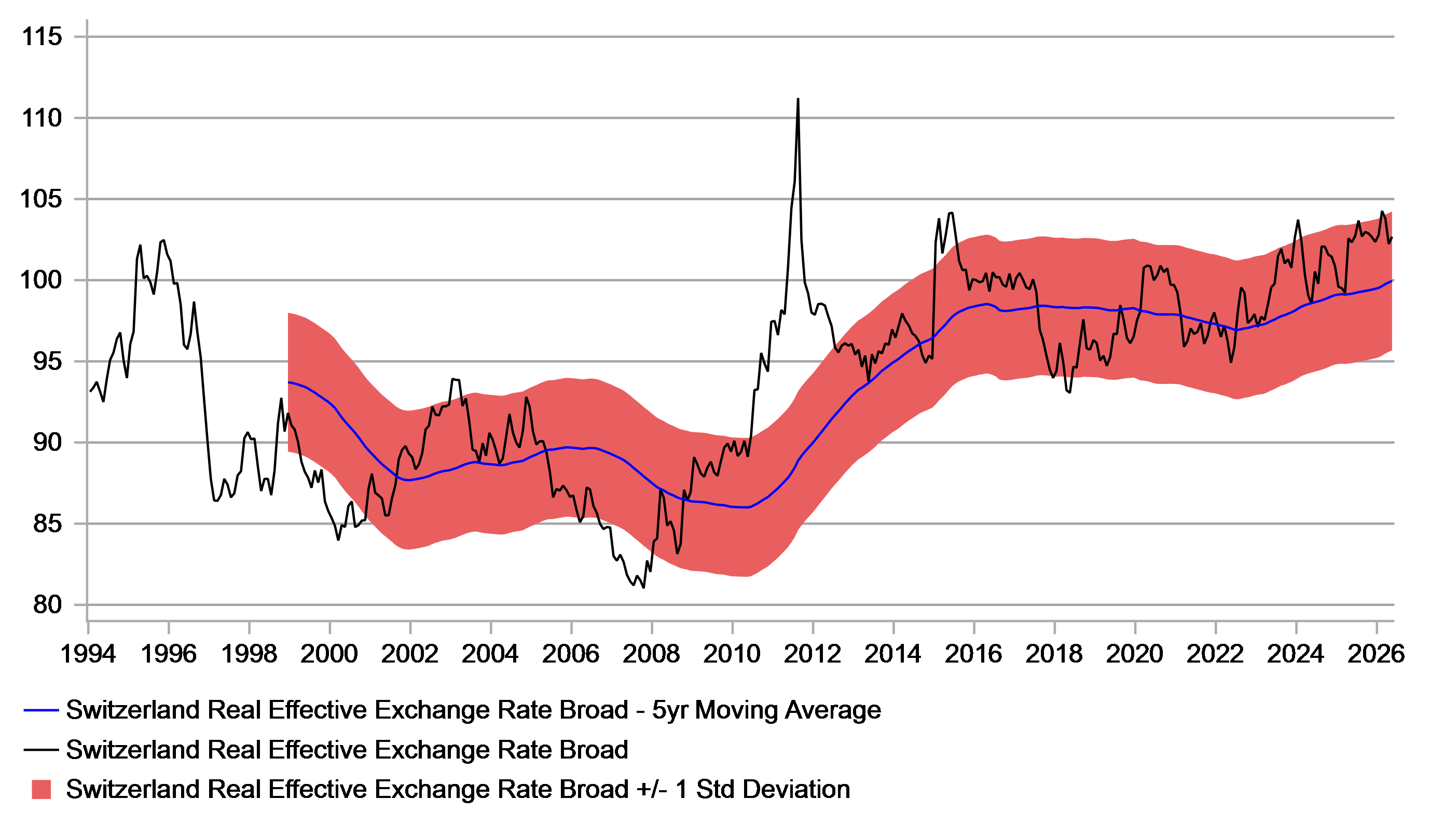

The focus has been very much on the Fed meeting on Wednesday and the BoE meeting yesterday, but the SNB also met yesterday and as expected left the key policy rate unchanged at zero percent. The franc underperformed much of G10 and was the third worst performing with only NOK and SEK performing worse. There was certainly no sense of urgency communicated by the SNB in relation to having to respond to any upside inflation risks. The SNB did raise its projection for inflation by year-end by 0.2ppt to 0.8% and the calendar year adjustments higher were even smaller at just 0.1ppt. The very limited adjustments to forecasts underlines the prospects of continued low inflation in Switzerland, which has been a source of demand for the franc given the lower risk of an inflation induced decline in real yields that is a much higher risk in the euro-zone, the UK and the US. The SNB also reiterated that “if necessary” it would be willing to intervene to ensure excessive currency strength is avoided that would undermine achieving the SNB’s price stability goal. President Schlegel was keen to play down the idea that the inclusion of the words “if necessary” implied there was less willingness to intervene to sell the franc.

However, the adjustments to the inflation projections, even though minor, does reduce somewhat the appetite of the SNB to revert to negative rates if required. The rise in yields globally since the conflict began has had an impact on weakening the franc. Since the start of the conflict the franc is the second worst performing G10 currency although some of that move also reflects the easing of geopolitical risks and the fact that the inflation shock stemming from the Middle East conflict is turning out to be smaller than initially feared. If US yields advance further in the wake of the more hawkish Fed communication this week, then franc underperformance could extend further.

However, we suspect the upside scope for global yields from here is relatively limited. We do not expect the Fed to hike rates this year and yesterday changed our call for the BoE to the policy rate remaining unchanged this year (from +50bps) while the ECB at most will raise rates just once further. Front-end yields therefore look overdone relative to the monetary action that will likely be delivered. Next year we expect the Fed, ECB and BoE to cut rates which suggests to us that the window for higher global yields to weaken the franc from here is relatively narrow.

CHF REER REMAINS ELEVATED WITH SNB YESTERDAY REPEATING ITS WILLINGNESS TO INTERVENE

Source: Bloomberg, Macrobond & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EC | 11:30 | ECB's Elderson Speaks | - | - | - | !! |

CA | 13:30 | Core Retail Sales (MoM) | (Apr) | 0.8% | 1.4% | !! |

CA | 13:30 | Retail Sales (MoM) | (Apr) | 0.6% | 0.9% | !! |

CA | 13:30 | Retail Sales (MoM) | (May) | - | - | !! |

EC | 15:00 | ECB's Moulin speaks | !! | |||

EC | 15:30 | ECB's Lane Speaks | - | - | - | !!! |

Source: Bloomberg & Investing.com