Warsh to determine rates & FX path from here

USD: Warsh gets his first opportunity – key moment for dollar

Today has been marked for some time as a key date for the financial markets and that remains the case even with near-term inflation risks having receded notably following the confirmation of a 60-day ceasefire extension agreed between the US and Iran. As a result, Brent crude oil fell below the $80pbl level yesterday for the first time since 3rd March. Fed Chair Kevin Warsh’s first post-FOMC meeting press conference may therefore be somewhat more balanced than it might have been if crude oil was still trading above the $100pbl level. In the space of one month, crude oil has declined from an intra-day high (on 18th May) by 30%. That’s a game-changer in terms of assessing near-term risk to broader inflation from a sustained energy price shock.

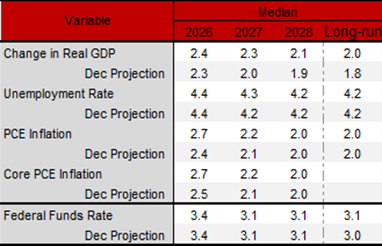

But this doesn’t imply Fed Chair Warsh will be dovish this evening and inflation risks are likely still a concern. The unchanged policy announcement this evening will be accompanied by an update of the Summary of Economic Projections (SEPs) that will include the median dot profile. A number of the other FOMC members will certainly be still more concerned over inflation risks than at the last SEPs update in March and hence, we will likely see the one rate cut for this year implied by the median dots in March being removed. In March twelve of nineteen FOMC members saw at least one rate cut this year with seven of the twelve expecting one cut. Stephen Miran expected four cuts, but he is no longer an FOMC member, so the median dot profile is skewed a little higher because of that. It’s a close call on 2027 but given the sharp drop in crude oil prices it is likely that the 2027 median dot showing one rate cut is maintained and one further dot to get to the long-run 3.125% level is either added in 2027 or is put into 2028. In March only four dots were higher than a range of 3.25%-3.50%. If that implied cut in 2027 was removed from the dot profile it would likely have a more meaningful impact on the rates market as it would imply a fundamental shift rather than a delay in easing due to the energy price shock.

The statement is very likely to show the removal of the implied easing bias with the removal of the word “additional” referring to adjustments to the fed funds target range which would signal the view of the FOMC that the next move could be a hike or a cut. That is widely expected after three FOMC members dissented against the statement.

The other element that will be important for the markets is whether Chair Warsh will indicate any plans at this early stage in how the Fed will operate under his leadership. He could imply or possibly even announce a review of the communication framework of the Fed, including forward guidance methods (dots profile, speeches) which would reinforce the potential for greater uncertainty around Fed meetings that could result in additional risk premia being priced. Any signal of looking more closely at balance sheet policy would add to upward pressure on longer-term yields.

In the period since the crude oil price has dropped nearly 30%, the 2-year UST bond yield is close to unchanged so there is clearly a reluctance amongst investors to take a bullish view on rates with uncertainty over the outcome this evening an obvious deterrent. Investors also likely see the energy price drop as only a counter to the continued surge in equities and the three months of stronger than expected NFP reports. Warsh is likely to signal that the policy stance is currently appropriate and given the changes to the statement and the SEPs is likely to be more hawkish, he may be reluctant to push a dovish view at this juncture. Still, the large drop in energy prices could well allow him leeway to emphasise the importance of looking through energy price shocks that could help pressure front-end rates and the dollar lower.

FED PROJECTIONS LIKELY TO SHOW HIGHER INFLATION VS MARCH 2026 LEVELS & DEC 2025 LEVELS

Source: Federal Reserve; March 2026 Summary of Economic Projections

USD: Leveraged Funds bought ahead of deal

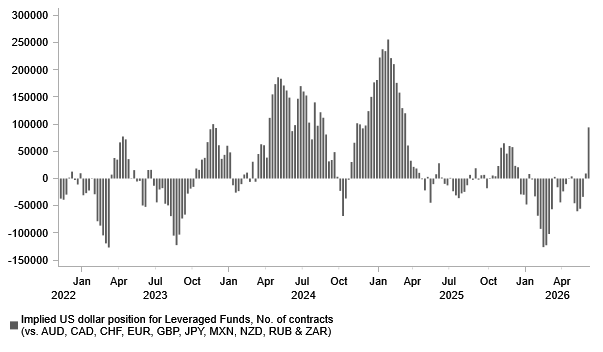

The IMM data released last Friday covering the week to last Tuesday highlighted the turn in sentiment for the US dollar with implied long positions amongst Leveraged Funds surging to the highest level since March 2025 – it was the biggest one-week US dollar buying shift since March 2023. The week covered the release of the non-farm payrolls data that revealed another stronger than expected reading that helped fuel US dollar buying. DXY did jump of course although the scale of the spot FX move was not reflective of the change in US dollar positioning. This partly reflects the fact that AUD shorts (USD buying) increased, and AUD is not included in DXY. Nonetheless, sentiment has clearly improved for the dollar based on US factors like a more resilient labour market. So, this goes some way to explaining the resilience of the US dollar this week despite the continued sharp falls in crude oil prices.

Today, Bloomberg has reported the details of the MoU scheduled to be signed in Switzerland on Friday and the details certainly point to a strong incentive for Iran to adhere to this deal. The 14-point plan reads favourably for Iran and is likely to be met with increased criticism, certainly in Israel. The MoU agrees that once a full final deal is agreed the US and regional partners will agree to USD 300bn of financing for the “rehabilitation and economic development” of Iran, the unfreezing of Iran’s assets and the removal of “all types of sanctions” while in the meantime on signing the MoU the US will commit to issuing waivers for exports of energy products and services. Iran’s enriched uranium stocks and Iran’s future nuclear capabilities will be negotiated over a 60-day window but with scope for that period to be extended. This MoU looks very favourable for Iran which now has a strong incentive to clear the SoH of mines quickly.

The US dollar positive momentum will be reinforced this morning by the weaker than expected UK inflation data. This is the second consecutive month of weaker inflation data and will provide more scope for the BoE to hold off hiking. We had assumed the BoE would hike but these consecutive weaker CPI prints point to a greater chance now that the BoE will be able to hold off and keep the policy rate stable – certainly if this MoU is signed and crude oil prices can stabilise at these lower levels.

LEVERAGED FUNDS BOUGHT US DOLLARS IN LATEST WEEK OF DATA AS US JOBS MARKET REMAINED STRONG

Source: Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

UK | 09:30 | House Price Index (YoY) | - | 2.8% | 0.0% | ! |

EC | 10:00 | CPI (MoM) | (May) | 0.1% | 1.0% | !! |

EU | 10:00 | Core CPI (MoM) | (May) | 0.3% | 0.9% | !! |

EC | 10:00 | CPI (YoY) | (May) | 3.2% | 3.0% | !!! |

EC | 10:00 | Core CPI (YoY) | (May) | 2.5% | 2.2% | !!! |

US | 10:00 | IEA Monthly Report | - | - | - | !! |

EU | 11:50 | ECB President Lagarde Speaks | - | - | - | !!! |

US | 13:30 | Retail Sales (MoM) | (May) | 0.5% | 0.5% | !!! |

US | 13:30 | Core Retail Sales (MoM) | (May) | 0.6% | 0.7% | !!! |

US | 13:30 | Retail Control (MoM) | (May) | 0.4% | 0.5% | !!! |

US | 15:00 | Pending Home Sales (MoM) | (May) | 0.8% | 1.4% | ! |

US | 19:00 | Fed Interest Rate Decision | - | 3.75% | 3.75% | !!! |

US | 19:00 | FOMC Statement | - | - | - | !!!!! |

US | 19:00 | FOMC Economic Projections | - | - | - | !!!!! |

US | 19:30 | FOMC Press Conference | - | - | - | !!!!! |

Source: Bloomberg & Investing.com