The GPIF flows already highlighting stronger home bias

JPY: Some signs of homeward bias already

The yen remains close to cyclical lows and the US data yesterday (see below) along with the risk of further crude oil price rises are curtailing the appetite to sell the US dollar following the weak CPI and PPI reports. We would still argue that the lack of price action in the yen should not be viewed as the government’s push to encourage greater investment in domestic assets not being significant. We would still argue that it marks a notable turning point from the Abenomics era that encouraged investments in risker assets to boost returns – for pensions this would help restore confidence in Japan’s pension system and in turn reduce cautionary savings. That would lift consumer spending and help end mild deflation.

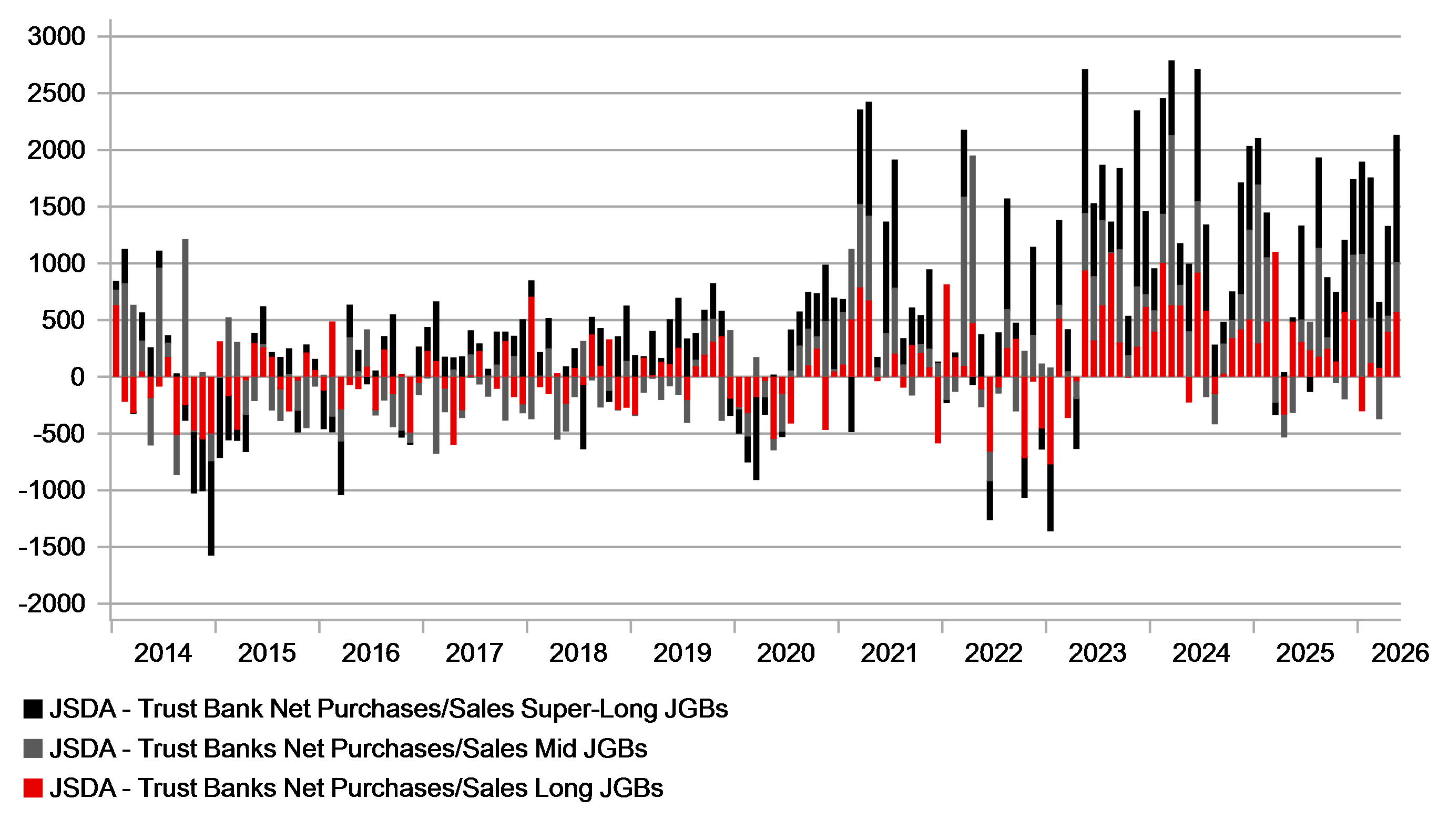

The start of formalising the end of that policy – which is happening now – is significant. It could certainly help shift the mindset on investment behaviour. There is though some evidence that flows have already started to shift. Below is the JSDA data on JGB buying by Japan Trusts (that would include GPIF). You can see a clear upturn in buying from late 2020, which continued bar a disruption in 2022 possibly reflecting greater volatility during the global inflation shock period. From the Abenomics review and announced change in 2014 (Domestic bond allocation reduced from 60% to 35%) Trust banks started selling JGBs – over the five-year period 2014-18 Trusts sold JPY 1,280bn worth of JGBs. The GPIF allocation for domestic bonds was then lowered from 35% to 25% in 2020 but the composition was already slightly below 25% (there was a +/-10% band then) and this in fact looks to have in fact marked a turning point back favouring JGBs although the notable pick-up in JGB buying was from 2021.

The GPIF domestic bond composition has gone from 23.9% at the end of FY2019 (as of March 2020) to the current 26.9%. Based on the GPIF composition falling ahead of the formal reduction in 2020 from 35% to 25%, we could well see stronger demand for JGBs continuing with the potential of reaching 31% (+6% from 25% benchmark). From this latest total, even holding the value of the fund constant, a move to 31% would imply potentially an additional JPY 12trn worth of JGB buying, but more if the total fund continues to grow. If a review is sooner, then the pace of buying would be even more.

Policy will only take you so far though and the BoJ still needs to play its role in encourage greater investments at home. The government this week added a footnote to its Economic and Fiscal Policy Plan underlining the autonomy of the BoJ as laid out in the BoJ Act. The government is now being pro-active in countering the perception of PM Takaichi pushing back on BoJ rate hikes. Household inflation expectations in data yesterday hit the highest since 2006. The BoJ now needs to show it is not constrained by the government and hiking in September would be the best way to do that and would go some way to helping turn the yen stronger.

PURCHASES/SALES BY JAPAN TRUSTS MID, LONG, SUPERLONG JGBS

Source: Bloomberg, Macrobond & MUFG Research

USD: Stronger data & crude oil contains US dollar selling

There has been no let-up in the escalation of the conflict in the Middle East which continues to curtail appetite to sell the dollar. Attacks by the US have expanded in the sixth day of renewed fighting. Iran has responded by attacking US bases in Kuwait, Jordan and Bahrain. Observable traffic in the Strait of Hormuz is sparse but the advance of crude oil prices have certainly not yet hit a level that would see risk assets come under pressure via higher yields. The broader conditions in risk have worsened with investors continuing to reduce exposure in chip-related stocks as AI valuations continue to be questioned. This is not hurting the US dollar however with the sell-off impacting Asian equities to a greater degree. The Kospi is down close to 20% so far in July while the TAIEX in Taiwan is 7.5% lower and the Nikkei is down close to 9%. The Nasdaq is 1.3% down this month. If the resilience in US markets gives way then we could see current US dollar resilience give way.

US data releases yesterday have also helped curtail dollar selling. The ‘Philly Fed’ manufacturing index surged (41.4 from 10.3) with most indices within the report pointing to a pick-up in manufacturing activity. Retail sales (control group) remained robust with a 0.5% gain following an upwardly revised 0.8% in May. Initial claims fell.

There was no notable response in the rates market to the flow of better data yesterday with most senior FOMC officials indicating the Fed is well placed and that there is little need for action. NY Fed President Williams helped weaken the dollar on Wednesday with dovish comments while Governor Jefferson stated yesterday that the current policy stance will be enough to support the labour market and bring inflation lower. Fed Presidents appear less confident though and Dallas Fed President suggested a higher policy rate would better balance the growth and inflation risks. It certainly looks likely that a lot of the nine dots for a hike in 2026 in the Summary of Economic Projections were from Fed Presidents rather than Governors. Today is the final day of Fed public comment before the blackout ahead of the FOMC meeting on 29th July. No Fed officials are scheduled to speak today.

A full hike remains priced by year-end, but spreads have generally remained against the dollar since the US inflation data this week. The risk of a sudden lurch higher in crude oil prices remains the primary deterrent to renewed US dollar selling. While there are reports that some tanker traffic is getting through the Strait of Hormuz it appears to be at a level that could quickly become problematic for energy supply – the IEA says within weeks. A worsening of the conflict over the weekend is a further risk curtailing US dollar selling. Another lurch higher in energy prices would see a Fed rate hike brought forward once again and this remains the primary risk to our view of a renewed trend lower for the dollar.

BRENT CRUDE NOT YET AT A LEVEL TO DICTATE US DOLLAR DIRECTION

Source: Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EZ | 10:00 | Industrial Production (MoM) | (May) | 0.3% | 0.1% | !! |

EZ | 10:00 | Industrial Production (YoY) | (May) | -0.5% | 0.3% | ! |

UK | 11:30 | BoE MPC Member Pill Speaks | - | - | - | !!! |

US | 12:00 | MBA Mortgage Applications (WoW) | - | - | -2.2% | ! |

US | 13:30 | NY Empire State Manufacturing Index | (Jul) | 9.40 | 5.70 | !! |

US | 13:30 | PPI (MoM) | (Jun) | 0.0% | 1.1% | !!! |

US | 13:30 | Core PPI (MoM) | (Jun) | 0.4% | 0.4% | !!! |

US | 13:30 | PPI (YoY) | (Jun) | 6.2% | 6.5% | !! |

US | 13:30 | Core PPI (YoY) | (Jun) | 5.2% | 4.9% | !! |

CA | 13:30 | Wholesale Sales (MoM) | (May) | -0.7% | 0.6% | ! |

US | 13:45 | Fed's Williams Speaks | - | - | - | !!! |

CA | 14:45 | BoC Interest Rate Decision | - | 2.25% | 2.25% | !!! |

CA | 14:45 | BoC Monetary Policy Report | - | - | - | !!! |

CA | 14:45 | BoC Rate Statement | - | - | - | !!! |

CA | 15:30 | BOC Press Conference | - | - | - | !!!! |

EZ | 17:00 | ECB's Nagel Speaks | - | - | - | !! |

US | 18:00 | Fed's Cook Speaks | - | - | - | !! |

US | 19:00 | Beige Book | - | - | - | !! |

Source: Bloomberg & Investing.com