Optimism persists leaving the US dollar vulnerable but risk could turn quickly

USD: Trump keeps market optimism going

The US dollar on a DXY basis is trading around 0.6% stronger since the conflict in the Middle East began while equity market resilience persists on the continued optimism that a deal will be soon reached between the US and Iran and the disruption to energy supply will reverse quickly. President Trump stated that it was “looking very good” that Iran would make a deal and “it’s going to be a good deal”. There has been no official public comment from the Iranian regime that endorses Trump’s optimism with Trump’s very political comments indicating optimism with Iran’s more technical and defensive comments that convey a high level of wariness on the Iranian side to show any perception of being the country that is backing down.

For the financial markets it is more about what’s actually happening on the ground and with the ceasefire holding and Lebanon and Israel also agreeing a ceasefire, these details are enough to keep the positive risk sentiment going. President Trump is now shifting focus to try and tackle the rising unpopularity of the war and spoke yesterday in Las Vegas during a “No Tax on Tips” roundtable, describing the economy as “great” and that we are “blowing it away now” mentioning the fact that the US equity markets were again at record highs. But you can’t imagine that citing rising inflation as “fake” is going to provide a boost to his popularity when gasoline prices remain over 36% higher since the conflict began. Despite the optimistic spin the prospect of larger disruptions to economic activity increases by the day. Bloomberg ship-tracking data for the Strait of Hormuz indicated just 2 ships passed through yesterday, which was the lowest since 10th April. So far today, the data shows just one ship has passed through. So the reports of progress are not being matched by any increased flow of tanker traffic. Refined fuel shortages look to be approaching and there remains substantial price divergences. Jet fuel is 150% higher compared to a 40% gain for Brent.

But the US dollar will remain vulnerable for now given this optimistic backdrop and unless we see a notable jump in crude oil prices from here and/or larger declines in global equities then scope for further dollar depreciation remains. We continue to see capacity for the Fed to cut rates later this year and in any case will remain more inclined toward rate cuts than either the ECB or the BoE. The Fed has a dual-mandate and looks more inclined to focus on underlying inflation than headline inflation including energy. New York Fed President Williams stated yesterday that his “primary concern is core inflation”.

Next week Kevin Warsh will testify in his nomination hearing (Tuesday 21st April) but there are already calls for this to be delayed given the threat to his nomination not even getting through committee stage. Fed independence uncertainties and Trump’s overt interference and general US dollar debasement fears will likely return to focus, and weigh on the US dollar.

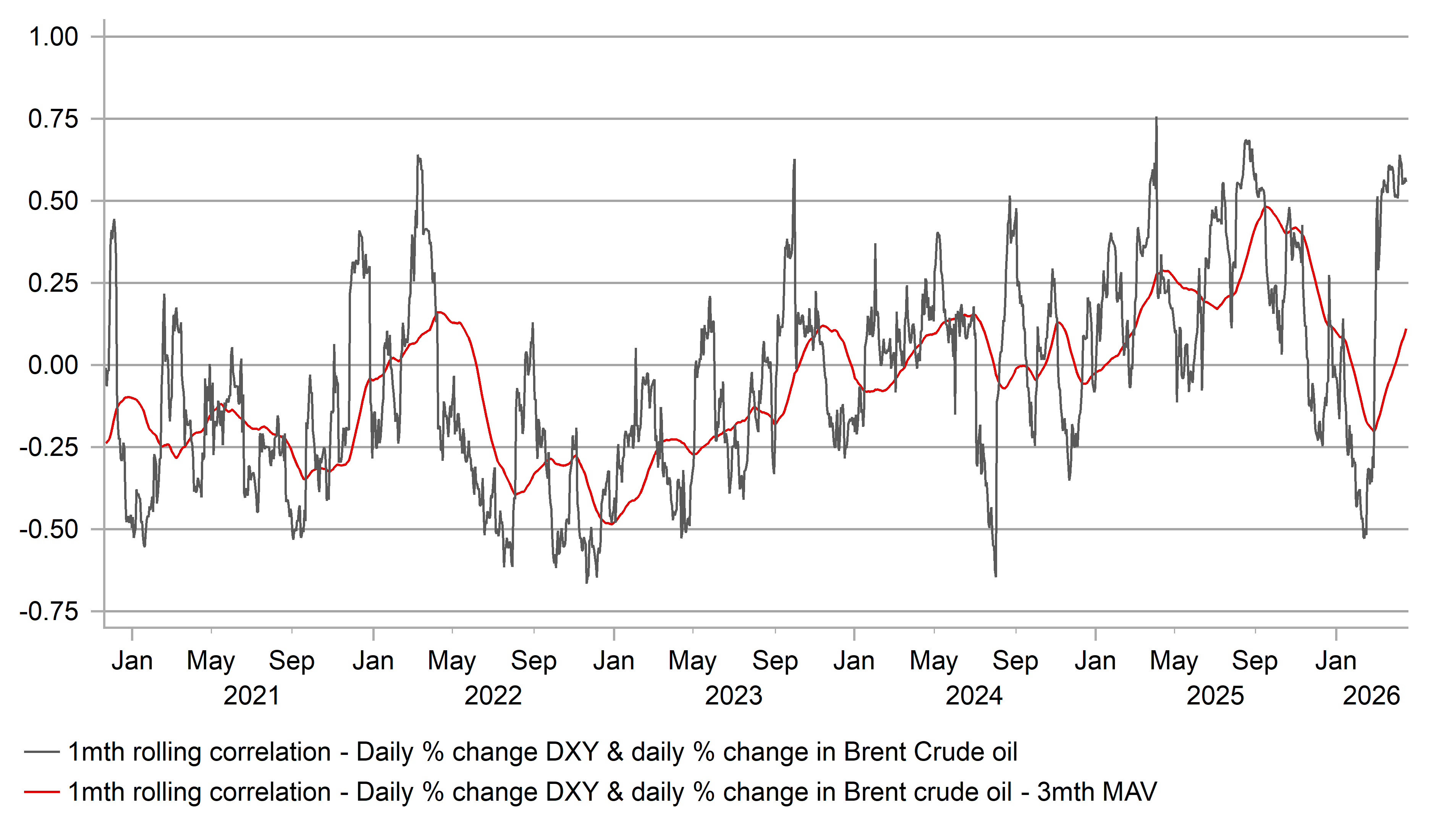

BRENT CRUDE OIL & USD CORRELATION REMAINS ELEVATED

Source: Bloomberg, Macrobond & MUFG GMR

GBP: Political risks could be re-emerging

The pound remains the third best performing G10 currency since the conflict began with only the Norwegian krone and the Australian dollar outperforming. Yield has continued to counter the downside risks from the energy shock and we continue to expect a 25bp rate hike in June. MPC member Alan Taylor spoke yesterday and, as expected from a key MPC dove, leaned more in favour of caution over policy action ahead arguing that the current stance is already restrictive and hence the BoE has time to assess the inflation impact from the conflict. The fiscal policy outlook could be another factor for Taylor to use for arguing caution ahead. The Telegraph is reporting that some in cabinet will push for increased defence spending being financed by cuts in benefits. A bigger drag on economic growth would be one further reason for the MPC to not rush into rate hikes. Government spending cuts would be very divisive for the Labour government and would be a real threat to PM Starmer’s leadership. But the government may be left with no alternative given the potential instability that could emerge in the Gilt market.

PM Starmer’s authority is also set to be challenged following the news that Peter Mandelson had failed security vetting procedures and despite that was then still selected as the UK’s US ambassador. PM Starmer had told parliament that “due process” had been followed and now is being accused of misleading parliament. The government has denied this stating Starmer was unaware of the vetting failure. The Foreign Office used exceptional powers to over-ride the vetting decision according to the Telegraph. It is hard to believe that Starmer would not have been aware of that and opposition leaders are calling for Starmer to step down.

The divisions within the Labour party look set to worsen after the local elections take place on 7th May when the government are expected to perform poorly. Starmer will come under further inevitable pressure to resign. The Gilt market has opened with yields modestly higher but if political risks intensify we could certainly see this translate to pound underperformance over the coming weeks.

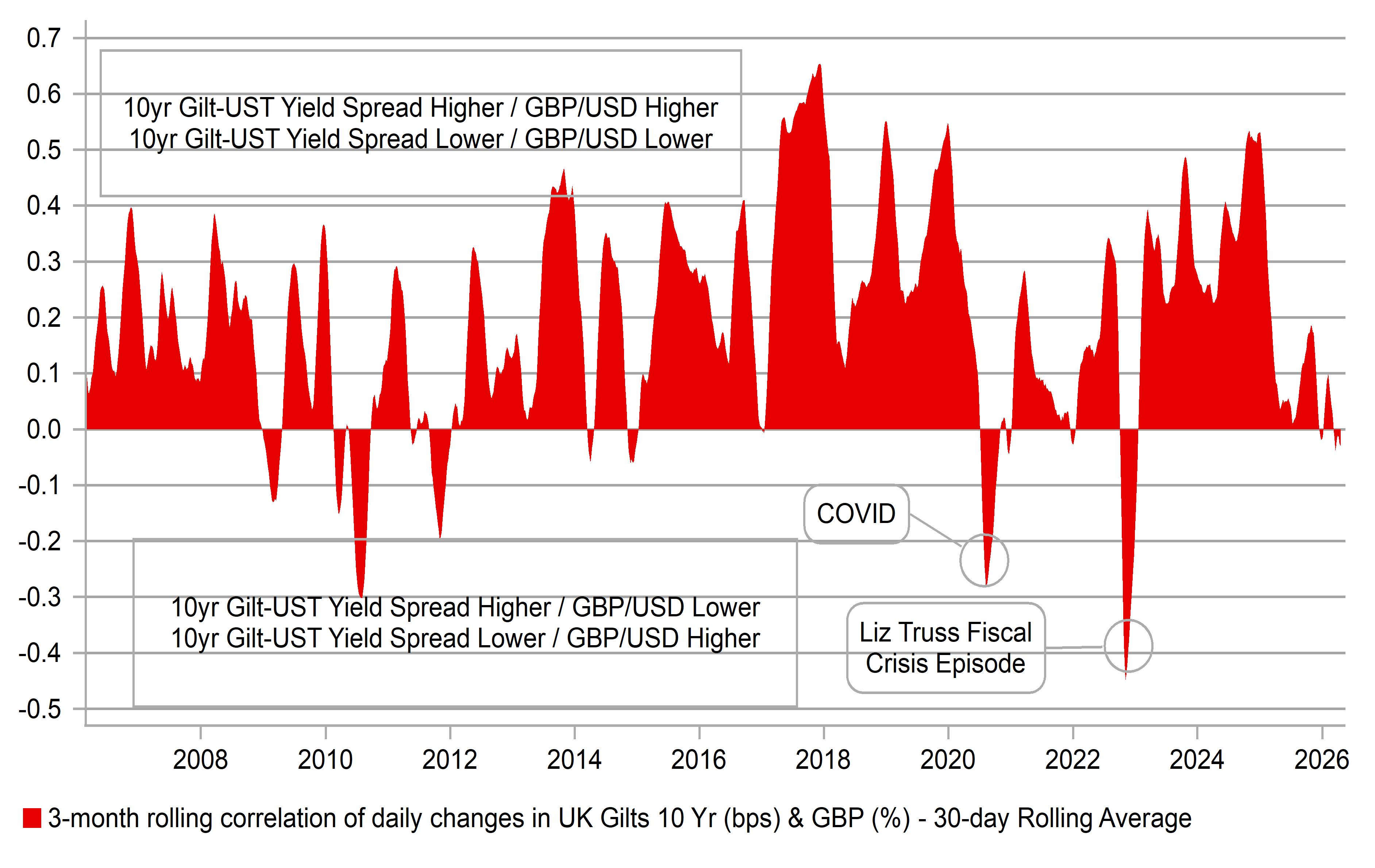

UK-US 10-YEAR SPREAD CORRELATION WITH GBP/USD IS MODESTLY NEGATIVE UNDERLINING FISCAL RISKS TO GBP

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EU |

09:00 |

Current Account |

(Feb) |

29.8B |

37.9B |

! |

|

EU |

10:00 |

Trade Balance |

(Feb) |

11.7B |

-1.9B |

!! |

|

US |

11:00 |

IMF Meetings |

- |

- |

- |

! |

|

UK |

13:00 |

BoE MPC Member Pill Speaks |

- |

- |

- |

!!! |

|

CA |

13:15 |

Housing Starts |

(Mar) |

258.0K |

250.9K |

!! |

|

CA |

13:30 |

Foreign Securities Purchases |

(Feb) |

23.81B |

46.73B |

!! |

|

CA |

13:30 |

Foreign Securities Purchases by Canadians |

(Feb) |

- |

11.390B |

! |

|

US |

16:30 |

Fed's Member Daly Speaks |

- |

- |

- |

!! |

|

US |

17:15 |

Fed's Member Barkin Speaks |

- |

- |

- |

!! |

|

US |

19:00 |

Fed's Waller Speaks |

- |

- |

- |

!!! |

Source: Bloomberg & Investing.com