Pound outperforms as UK fiscal concerns continue to ease

USD: Softer US inflation & dovish comments from Fed Chair Warsh in focus

The US dollar has continued to trade at weaker levels overnight with the dollar index moving back closer to the 100.00-level. The weaker US dollar has been driven by evidence of softer US inflation in recent days. Firstly, the release of the latest US CPI report for June revealed that both headline and core inflation were much weaker than expected falling to annual rates of 3.5% and 2.6% respectively. It has since been backed up the release yesterday of the softer than expected US PPI report for June. Taken together the CPI and PPI readings have indicated that the Fed’s preferred measure of underlying inflation pressure, the core PCE deflator, is likely to increase by around 0.2% in June helping to lower the annual rate to 3.3%. The reports have helped to ease pressure on the Fed to tighten policy as soon as this month in response to upside inflation risks. While the latest inflation data is encouraging, Fed Chair Kevin Warsh noted that policymakers should not overreact to a single month’s report. He cautioned that it did not mean “mission accomplished” on inflation. At the same time, comments overnight from Fed Governor Lisa Cook continued to highlight the Fed is still seriously considering rates this year. She stated that “if we do not see signs of disinflation soon, I am prepared to act”. But she is not in a rush to raise rates as she added that the “FOMC can take its time, I can take my time to observe more data to understand whether it’s really restrictive or not”. Overall, the US inflation data released this week supports our view that the Fed is likely to leave rates on hold this year contributing to a re-weakening of the US dollar (click here). The key test will be inflation data released over the summer alongside developments in the Middle East.

Our forecast for the Fed to leave rates on hold was also supported by some dovish comments yesterday from Fed Chair Kevin Warsh when speaking about the near-term inflationary impact from surge in capital investment related to AI. He told lawmakers that “I don’t view a one-time change in prices as necessarily being inflationary because I think there’s a supply response. In that way, this is different from a foreign conflict and what it might do, which tends to reduce the supply side of the economy”. The comments indicate a willingness to be patient with sources of inflation that he believed to be temporary, including demand from AI investment. In the medium-to-long run he remain optimistic that AI will deliver a positive supply shock to the US economy and prove disinflationary.

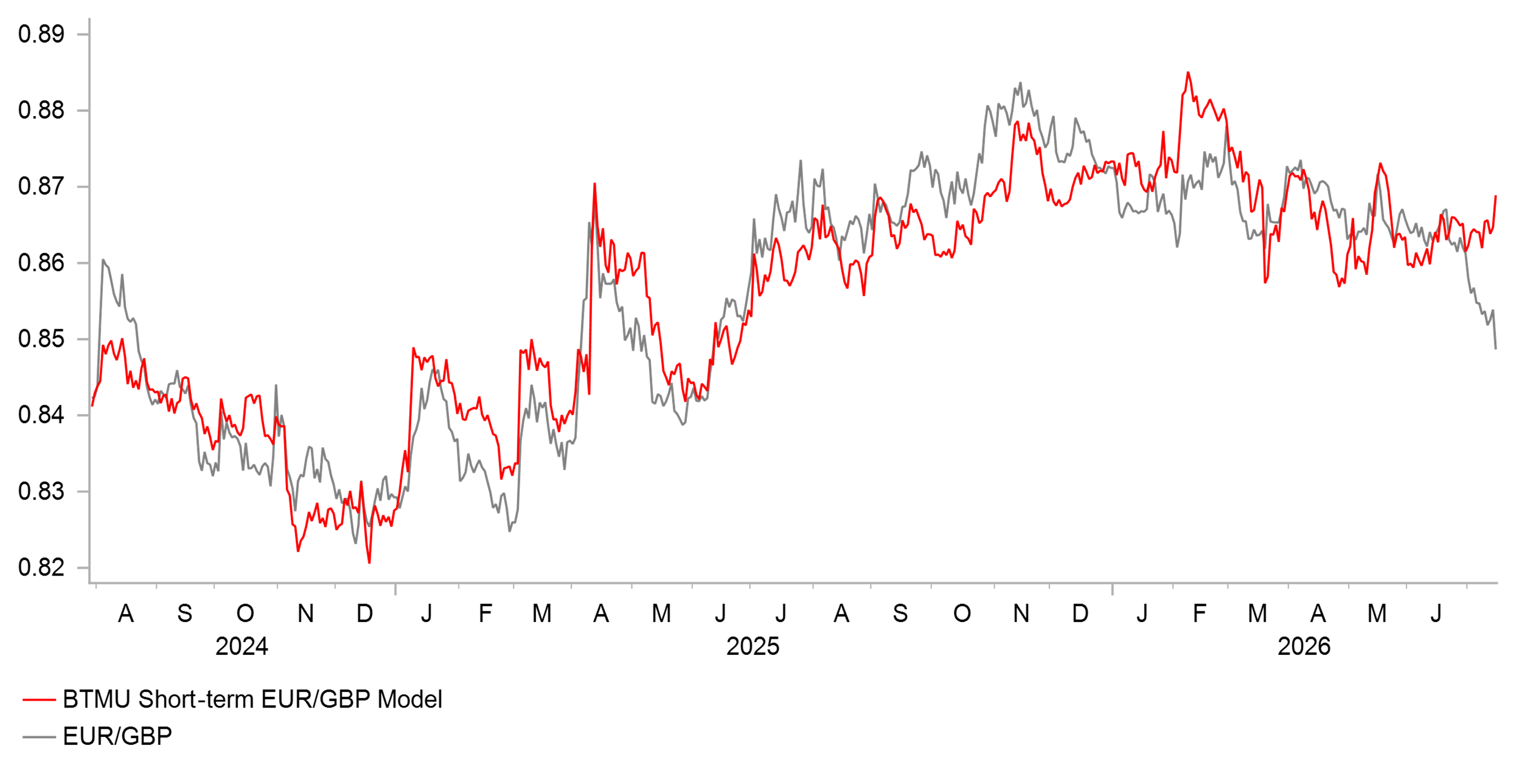

POUND HAS DIVERGED FROM SHORT-TERM FUNDAMENTAL DRIVERS

Source: Bloomberg, Macrobond & MUFG Research

GBP: Dampened fiscal risks & stronger UK growth provide support

The pound has continued to trade at stronger levels after strengthening sharply yesterday in response to media reports that Home Secretary Shabana Mahmood is set to become Britain’s next chancellor. While it has not yet been confirmed, the report provides further reassurance to market participants over the outlook for fiscal policy under new Prime Minister in-waiting Andy Burnham. Market participants had been fearful that he would choose a Labour MP from the left of the Labour party such as Ed Miliband who would also have been viewed as less supportive for economic growth given environmental agenda can increase costs, delay projects, or redirect investment away from traditional growth sectors. The appointment would back up recent comments from Andy Burnham stating that his policy agenda would be backed by “sound public finances” and the “discipline of our current fiscal rules”. The paring back of the UK fiscal/political risk premium helped the pound to outperform over the past month. EUR/GBP has fallen by around -2.5% since the high on 22nd June. However, it has not been sufficient to prevent gilts selling off again over this period in response to renewed inflation risks triggered by the conflict in the Middle East and the pick-up in BoE rate hike expectations. The UK rate market has moved to fully price back in a couple of BoE rate hikes in the year ahead. It stands in contrast to our own forecast for the BoE to leave rates on hold after inflation surprised significantly to the downside in recent months. There was also some good news for the pound this morning from the release of monthly UK GDP data for May which has raised our forecast for growth in Q2 up to 0.3% providing further evidence of stronger than expected growth in 1H of this year.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 10:00 | Trade Balance | (May) | 2.8B | -1.0B | !! |

GB | 12:00 | NIESR Monthly GDP Tracker | (Jun) | - | 0.5% | !! |

CA | 13:15 | Housing Starts | (Jun) | 256.0K | 261.4K | !! |

US | 13:30 | Initial Jobless Claims | - | 216K | 215K | !!! |

US | 13:30 | Retail Control (MoM) | (Jun) | 0.5% | 0.7% | !! |

US | 15:00 | NAHB Housing Market Index | (Jul) | 35 | 35 | ! |

Source: Bloomberg & Investing.com