JPY to weaken further without intervention

JPY: Middle East and crude oil not favouring yen stability

Crude oil prices are moving higher again and that is going to further unsettle sovereign bond markets with inflation concerns more elevated this week following higher than expected inflation in the US. President Trump stated that the Strait of Hormuz may not need to open “at all” reinforcing the prospect of a longer than expected closure. As we have written here before, the success or failure of MoF intervention to strengthen the yen was always going to come down to factors outside Japan’s control and those factors are clearly working against a strengthening of the yen. Global yields are heading higher once again, and crude oil is drifting higher with the Strait of Hormuz closed. USD/JPY is clear through the 158-level that marked the point when the MoF last intervened on 6th May and is quickly retracing back to the highs on 30th April when intervention first took place (both interventions to be confirmed).

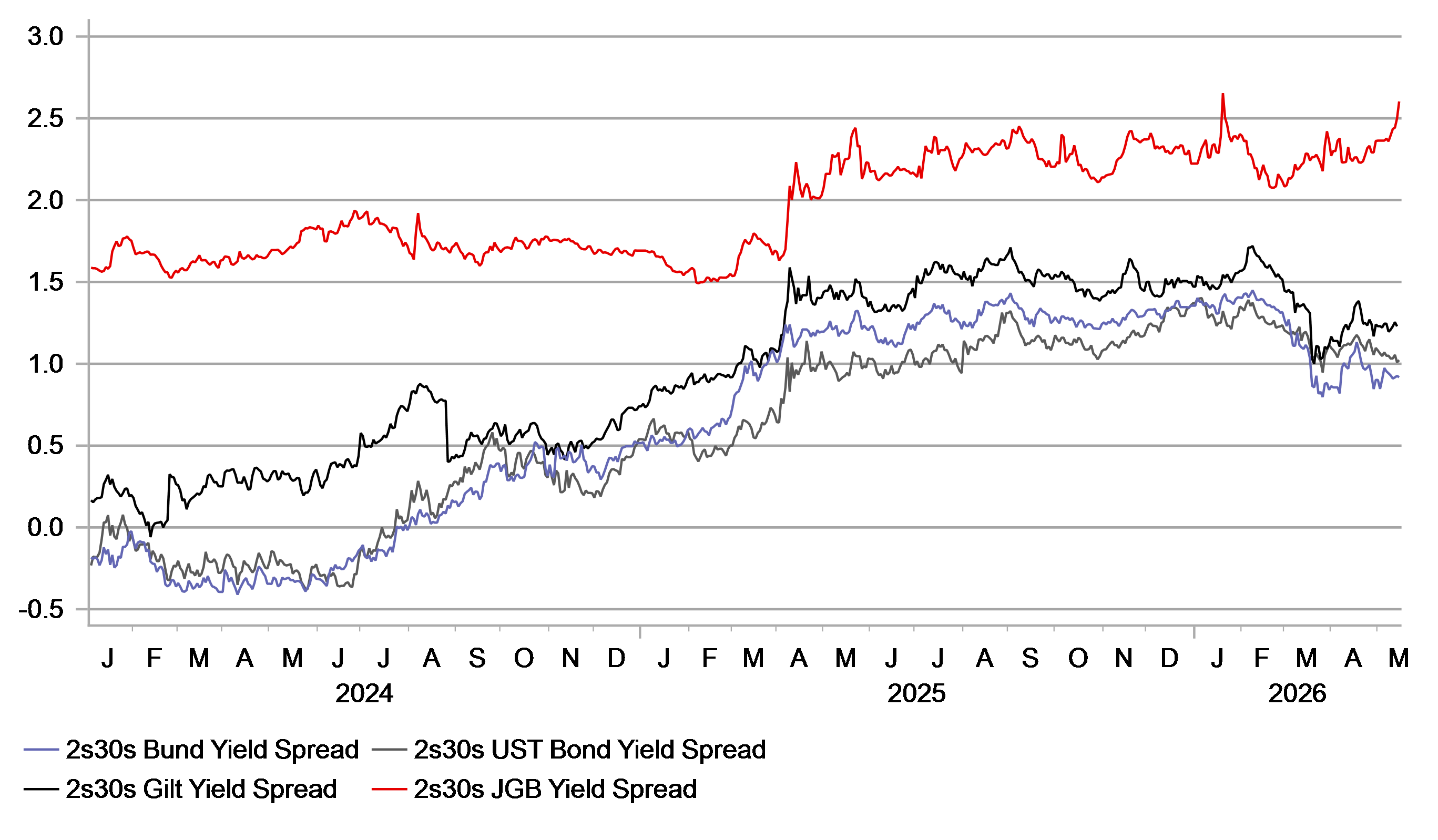

In these circumstances a rate hike by the BoJ would have been an important additional support for the success of intervention but the BoJ held off and this looks to be adding to bond market instability again. Fears of the BoJ being behind the curve are rising and the 2s30s JGB spread is widening sharply. Since the start of May, the 2s30s has widened by 23bps while since the conflict began at the end of February the same spread is 47bps wider. By contrast, 2s30s spreads for US Treasuries, Bunds and Gilts have all narrowed. Finance Minister Katayama spoke on Friday to suggest the JGB move was simply following global markets, but the evidence is clear – the JGB market is now underperforming with the monetary stance in Japan inappropriately loose. That was evident Friday with the release of the April corporate goods price data that revealed an annual increase of 2.3%, the biggest increase since April 2014. The decision to hold off hiking at the last meeting looks increasingly like the wrong decision.

There are also concerns over a further supplementary budget to ease the cost of living burden. Katayama denied that today stating the government had “not reached that point yet” – hardly reassuring comments that further fiscal spending won’t happen. Further intervention looks very likely if the MoF wants to continue capping USD/JPY. Investors are once again being left with the impression that higher inflation is being engineered and tolerated in order to fuel nominal GDP growth and bring down Japan’s debt in GDP terms. That is reducing investor appetite for longer-term debt. Domestic investors are primarily selling super-long JGBs with only foreign investors buying. Real yields are too low to stabilise super-long yields and real yields are declining further as inflation rises which likely makes further FX intervention by the MoF / BoJ necessary. It looks like the only way to halt another break higher in USD/JPY.

2S30S BOND YIELD SPREADS – JAPAN VERSUS US, UK AND GERMANY

Source: Bloomberg, Macrobond & MUFG Research

GBP & EUR: UK politics hits pound as rates in Europe drop

Each day appears to take us closer to a Labour party leadership election, but we are yet to see a formal challenge being made. The resignation of Wes Streeting from the cabinet certainly raises the prospect of a challenge and Streeting allies have stated he has the 81 votes necessary to make a challenge. The issue would appear to be that the Labour party membership do not indicate broad-based support for Streeting. A Survation poll indicated that a Streeting/Starmer head-to-head would see Labour members support Starmer over Streeting 53% to 23%. Starmer versus Burnham shows Burnham winning 61% versus 28% for Starmer. Rayner and Miliband are both favoured over Starmer but be less than Burnham (45% v 41% & 46% v 39% respectively). It may simply be that Streeting doesn’t have the numbers and that if Burnham is favoured then this saga is set to run for longer with a challenge only possible if Burnham manages to win a seat to re-enter parliament. This will not be a favourable backdrop for the Gilt market or the pound. If Streeting doesn’t make a move, then we are left with either a move soon by Angela Rayner or a longer wait and a move by Andy Burnham. A Burnham move looks probable now after Josh Simmons confirmed he would stand aside, orchestrating a by-election in Makerfield, Wigan with Burnham seeking NEC permission to stand. Simmons majority was 5,399 in 2024 and while Burnham would not be a shoo-in, he would be in a reasonably strong position to win. It makes for an intriguing by-election given the strong shift favouring Reform shown in the local elections last week.

The pound is now lagging and shares worst performing G10 currency this week with the Swedish krona. A decline in short-term rates is also playing a role and it looks like the move higher in rates in the US this week is playing a part in strengthening the rate spread / FX correlation once again – a correlation that had weakened since the start of the conflict. A lot of tightening is priced in Europe relative to the US and we may have reached peak divergence for now. Certainly, some of the rhetoric from BoE officials suggest that Huw Pill may be more on his own than assumed. Catherine Mann, generally more of a hawk, on Wednesday mentioned the risk of tightening policy more than needed. Huw Pill did speak yesterday and was clear on his view of a rate hike sooner but qualified that arguing that a “prompt but modest hike” would be advantageous. In addition, comments from ECB officials also indicate the upside risks to inflation are evident but modest. Chief Economist Philip Lane stated on Wednesday that inflation impact has so far been “relatively contained”.

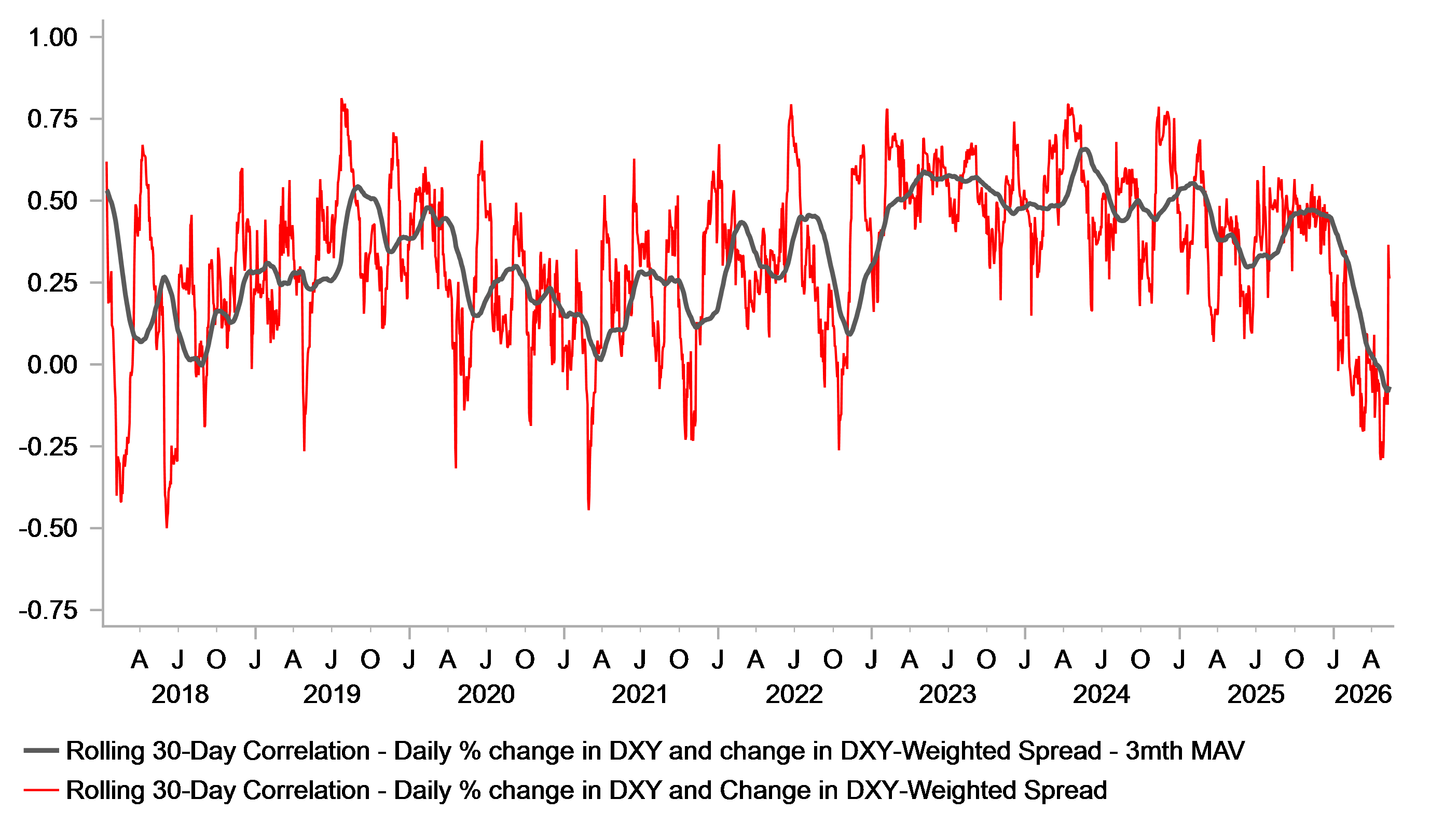

Based on these comments market pricing earlier this week was certainly starting to look misaligned with the OIS market pricing for the ECB by April 2027 showing nearly 90bps of hikes. For the BoE on Tuesday pricing reached 80bps over the same period. We continue to see scope for two rates hikes and hence the scope for this rates move to extend from here looks limited. For the US though after strong CPI, PPI and retail sales data, just 25bps of hikes by April 2027 leaves scope for further rate hike pricing. This week has seen the rolling correlation between DXY and the 2-year US-DXY rates spread strengthen notably, which points to scope for US dollar strength to extend further if rate hike pricing momentum continues.

ROLLING FX / RATE SPREAD CORRELATION HAS STRENGTHENED NOTABLY IN RECENT DAYS – FX / SPREAD CORRELATION COULD BE BACK

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 09:00 | ECB Bulletin | ! | |||

CA | 13:15 | Housing Starts | Apr | 245.0k | 235.9k | !! |

US | 13:30 | Empire Manufacturing | May | 7.3 | 11 | !! |

CA | 13:30 | Manufacturing Sales MoM | Mar | 3.5% | 3.6% | ! |

US | 14:15 | Industrial Production MoM | Apr | 0.3% | -0.5% | !! |

US | 14:15 | Manufacturing (SIC) Production | Apr | 0.2% | -0.1% | !!! |

US | 14:15 | Capacity Utilization | Apr | 75.8% | 75.7% | ! |

Source: Bloomberg & Investing.com