Inflation & UK political risks driving FX market performance

USD/JPY: Inflation risks and hawkish BoJ comments in focus

The US dollar has continued to trade at stronger levels this week supported both by the lack of progress in talks to end the Middle East conflict and re-open the Strait of Hormuz, and the hawkish repricing of Fed rate hike expectations. The US rate market has moved to more fully price in a Fed rate hike in the year ahead encouraged by strong US inflation readings in recent days. It was revealed that consumer price inflation jumped to 3.8% in April and producer price inflation rose even more sharply to 6.0%. While the pick-up in inflation was largely expected driven by higher energy prices, it will make the Fed more uncomfortable in the near-term as it moves further above the their target. So far the Fed has signalled that it is willing to look through the energy price shock, and remains comfortable to leave rates on hold but that view could be challenged the longer the Strait of Hormuz remains closed. The Senate’s decision overnight to confirm Kevin Warsh as the next Fed chair is helping to dampen rate hike expectations. He was confirmed by the slimmest margin ever for a Fed chair by 54-45 votes. With Kevin Warsh set to be in place at the next FOMC meeting on 17th June, market participants will be watching closely to see how he responds to the near-term pick-up in inflation. The US dollar could strengthen if there is any indication that the Fed’s tolerance for looking through higher inflation is diminishing.

The ongoing move higher in yields in Japan has attracted more market attention overnight as well after the 30-year JGB yield rose above the high from 20th January and hit a fresh high of 3.93%. The previous peak from 20th January was driven by heightened fiscal concerns in Japan after it was reported that the government was planning to lower the VAT rate on food to 0%. The recent sell-off appears to have been driven more by building inflation risks related to the Middle East conflict. The 30-year JGB yield has increased by around 55bps since start of the conflict. In comparison the 30-year US Treasury and euro-zone government bond yields have also risen by around 40bps and 30bps respectively.

The sell-off overnight has been encouraged by hawkish comments from BoJ board member Kazuyuki Masu who indicated that he is moving closer to voting for a rate hike. He stated “if statistical data do not indicate clear signs of an economic downturn, I believe it is desirable to raise the policy rate at the earliest stage possible”. At the last policy meeting in April, he voted to leave rates on hold and three other board members dissented in favour of a hike. He noted that there are concerns that rising fuel costs and already mounting distribution costs may not be temporary shocks. His comments have reinforced market expectations for the next BoJ hike to be delivered as soon as the next policy meeting in June. A development that would help to provide more support for the yen, and ease pressure on Japan to continue intervention in the FX market.

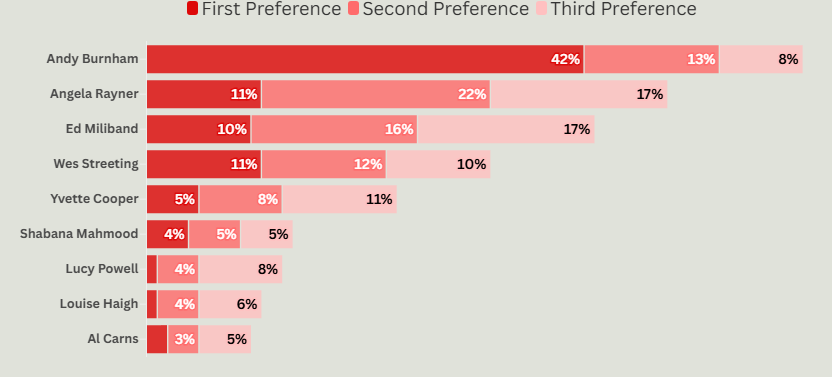

LABOUR PARTY MEMBERS FAVOUR SOFT LEFT CANDIDATES

Source: Survation poll results (30th April-5th May 2026)

GBP: UK political risks providing an offset to support from stronger UK growth

The pound continues to trade on a softer footing this morning despite evidence revealing that the UK economy expanded more robustly than expected at the start of this year. The latest UK GDP report revealed that the economy expanded by 0.6% in Q1 up from an upwardly revised expansion of 0.2% in Q4 2025. It was the fastest quarter of growth since Q1 of last year. It fits with the pattern in recent years whereby the economy has started strongly then slowed through the rest of the year. Slower growth in the coming quarters appears likely again in response to the energy price shock. On the plus side the UK economy had stronger growth momentum heading into the shock with growth driven by private consumption which expanded by 0.6% and business investment which expanded by 0.7%. Stronger UK cyclical momentum alongside higher UK yields and favourable conditions for carry trades have helped to the pound to surprisingly outperform so far during the Middle East conflict.

However, downside risks for the pound have increased in the near-term in response to heightened political uncertainty in the UK. It has been reported that Prime Minister Keir Starmer could face a leadership challenge as soon as today. Health Secretary Wes Streeting is reportedly set to quit his post this week and launch a bid to replace Starmer as leader of the Labour party. It is not yet clear if he has the backing of 81 MPs required to launch a formal leadership challenge. At the same time, it has been reported that Angela Rayner has been cleared in an investigation into whether she deliberately dodged paying tax which paves the way for her to launch her own leadership campaign. However, recent comments from Angela Rayner have indicated that she favours supporting Manchester mayor Andy Burnham as a potential leader, and would only run on her won if he is unable to take part.

Once a leadership contest is triggered, other candidates could join if they also have 81 backers. Labour party members and affiliate members then vote by postal ballot to choose the new leader. A recent survey carried out by Survation between 30th April and 5th May revealed that Andy Burnham is by far the most popular potential candidate amongst Labour members followed by other soft left candidates Angela Rayner and Ed Miliband. The survey indicates that a soft left Labour candidate is mostly likely to replace Keir Stamer if a leadership contest takes place which would create more unease over UK fiscal risks weighing on gilts and the pound.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 10:15 | ECB President Lagarde Speaks | - | - | - | !! |

GB | 12:00 | NIESR Monthly GDP Tracker | (Apr) | - | 0.6% | !! |

US | 13:30 | Retail Sales (MoM) | (Apr) | 0.5% | 1.7% | !!! |

US | 13:30 | Import Price Index (YoY) | (Apr) | - | 2.1% | ! |

US | 15:00 | Business Inventories (MoM) | (Mar) | 0.8% | 0.4% | !! |

GB | 16:15 | BoE MPC Member Pill Speaks | - | - | - | !! |

US | 22:45 | FOMC Member Williams Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com