USD rebound proves short-lived as sell-off resumes

USD: Optimism over further US-Iran talks triggers fresh sell-off

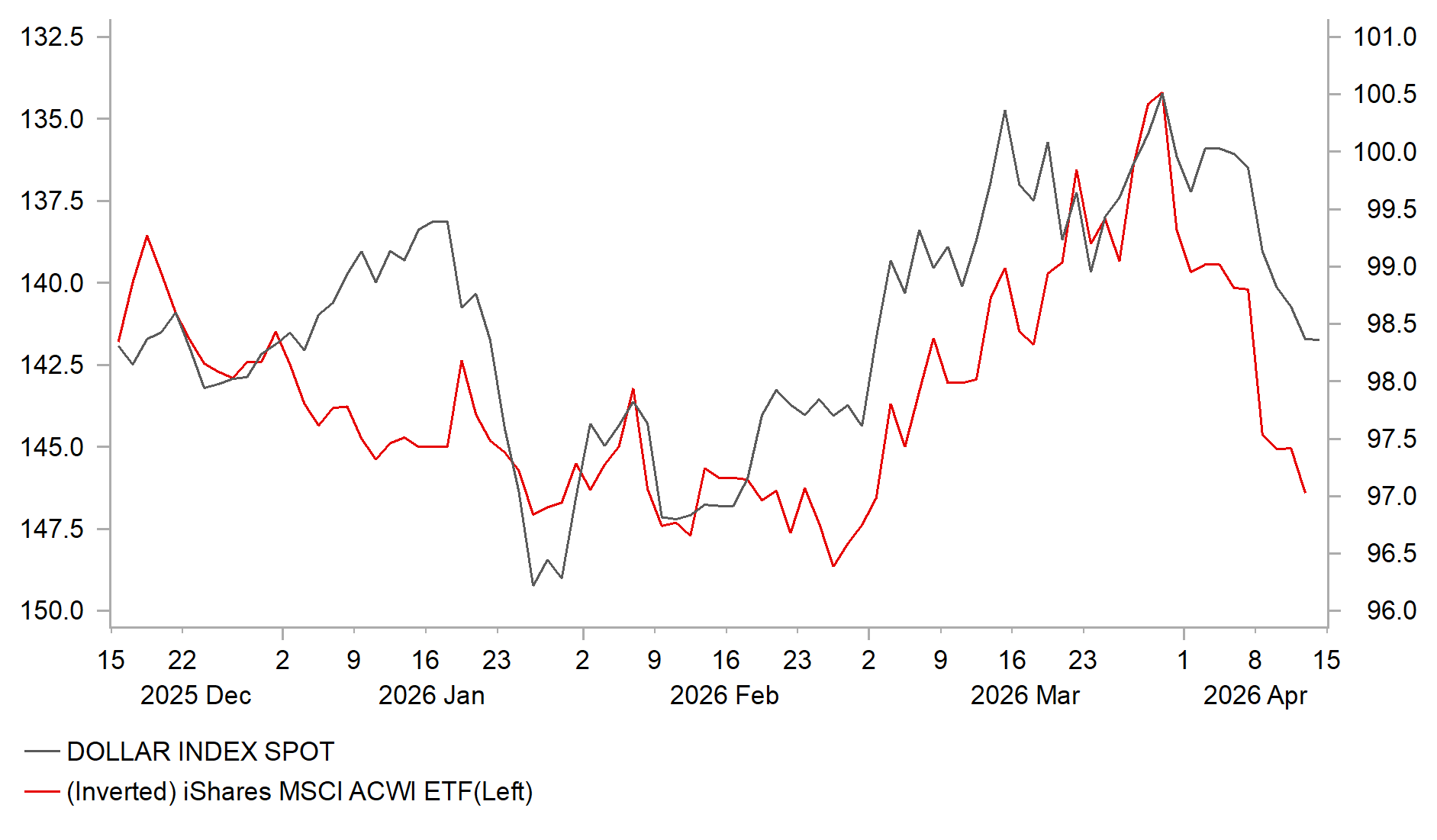

The US dollar’s rebound at the start of this week has proven short-lived with the dollar index quickly giving back those gains and more overnight as it moves back closer to pre-Middle East conflict levels. It now stands only around 0.7% stronger than levels recorded back in late February compared to an advance of around 3.1% at the end of March. The further reversal of US dollar strength was triggered by fresh investor optimism that the US and Iran will continue to work towards a deal to bring an end to the conflict. President Trump told reporters at the White House that “we’ve been called this morning by the right people, and they want to work a deal”. The reassuring comments quickly followed the talks between the US and Iran over the weekend that failed to reach a deal. He added though that “we did make some progress in the negotiation”. The media have also reported further details of the talks. The New York Times reported that the US proposed a 20-year suspension of nuclear activity while Iran countered with a plan to halt it for up to five years similar to an offer they made in February. The reports have given off the impression that both sides remain open to reaching a deal with the US and Iran reportedly discussing holding another round of negotiations before the two-week ceasefire ends next week. At the same time, Israel and Lebanon will engage in high-level security talks today for the first time since 1993. The latest developments have helped to bring the price of oil back below USD100/barrel and lifted global equity markets back closer to record highs.

In the foreign exchange market the best performing G10 currencies this month on the back of building investor optimism that the Middle East conflict will continue to deescalate have been the Scandi currencies of the Norwegian krone and Swedish krona closely followed by the commodity currencies of the New Zealand and Australian dollars while the US dollar and yen have both underperformed. The failure of the US dollar to strengthen further in response to the energy price shock is clearly a bearish development which is increasing downside risks to our updated forecasts (click here). We looked at potential reasons why the US dollar has underperformed relative to our expectations in our latest FX Weekly report (click here).

SUPPORT FOR USD FROM SAFE HAVEN DEMAND HAS FADED

Source: Bloomberg, Macrobond & MUFG GMR

JPY: BoJ Governor Ueda refrains from signalling April rate hike

The yen has continued to underperform at the start of this week resulting in USD/JPY rising back to within touching distance of the 160.00-level. It is notable that the yen has failed to strengthen against the US dollar which has corrected lower against all other G10 currencies over the past week. The US dollar sell-off reflects investor optimism that the Middle East conflict will continue to deescalate even after initial talks held over the weekend between the US and Iran failed to reach a deal.

One reason why the yen has continued to underperform at the start of this week has been the scaling back of BoJ rate hike expectations. The Japanese rate market is currently pricing in around 7bps of hikes for this month’s BoJ policy meeting compared to around 14bps of hikes at the end of last week. The main trigger for the dovish repricing was yesterday’s speech from BoJ Ueda who refrained from providing a clear signal that they are preparing to hike rates imminently. He also expressed more concern that “developments in the Middle East remain uncertain and we will closely monitor them and their potential impact on economic activity, prices and financial conditions”. He added that there were two-sided risks for inflation.

While the comments do not explicitly rule out another hike as early as this month, we acknowledge that there a higher probability now that the BoJ will wait a little longer to assess the economic fallout from the Middle East conflict before tightening policy further. A rate hike is now judged as more likely at the following policy meetings in June or July when the BoJ will have had more time to assess the economic fallout from the Middle East conflict and when uncertainty may have eased. One downside of delaying the timing of the next hike is that it leaves the yen vulnerable to further weakness in the near-term which could reinforce upside risks to inflation from higher energy prices.

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

US |

13:15 |

ADP Weekly Employment Change |

Mar-26 |

-- |

26.000k |

!! |

|

US |

13:30 |

PPI Final Demand MoM |

Mar |

1.1% |

0.7% |

!! |

|

US |

14:45 |

Fed's Goolsbee on AP Livestream |

!! |

|||

|

EC |

15:00 |

ECB's Lane Speaks |

!! |

|||

|

US |

18:00 |

Fed's Paulson, Collins, Barkin and Barr in Fireside Chat |

!! |

|||

|

EC |

22:00 |

ECB's Lagarde Speaks in DC |

!! |

Source: Bloomberg & Investing.com