Yield rise could threaten market calm

USD: Strong inflation as SoH stays closed

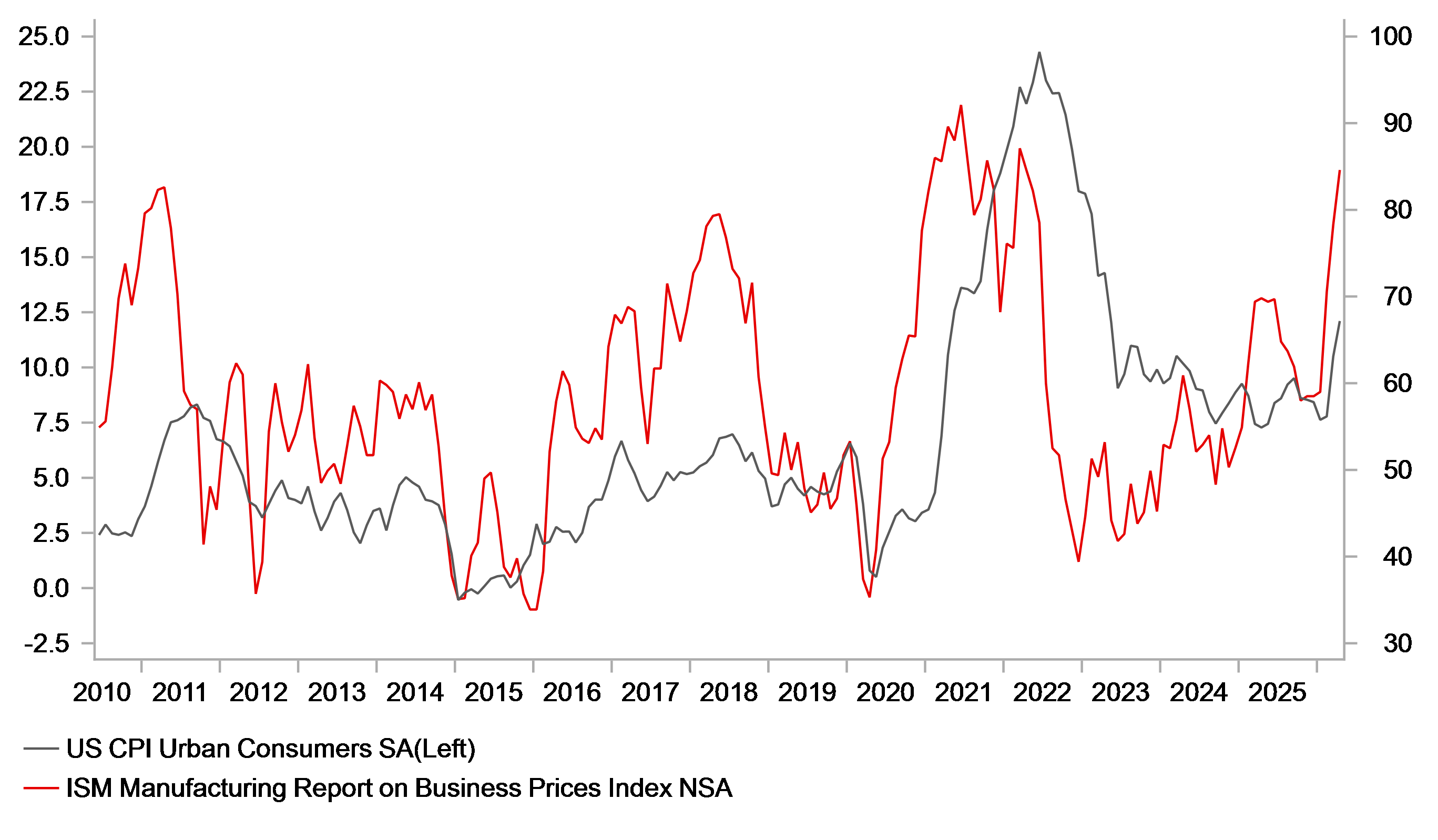

The US dollar remains broadly stable but has advanced modestly since the US inflation print yesterday that was stronger than expected. The 2-year UST bond yield jumped, closing at the highest level since the conflict in the Middle East began. The CPI report clearly showed the impact of rising energy with gasoline prices up a further 5.4% MoM in April after a 21.2% gain in March. Energy services jumped 1.6% MoM in April. Food prices jumped 0.5% MoM after being unchanged in March underlining the seep through from energy into food. There was a quirk on the rental inflation jump which was notable with the calculation based on rolling data collected every six months – that didn’t happen most recently due to the government shutdown and hence was measured in April based on a year of increases rather than six months. So the headline rates would have been lower but that is unlikely to be much comfort given the risks ahead of further upward pressure on prices as the Strait of Hormuz remains closed.

Gasoline prices remain close to recent highs in the US, up 50% from prior to the conflict starting and risks are rising of another lurch higher. We have already gone past the point of avoiding physical shortages and that is likely to play out in June into July in Europe but that playing out with the Strait of Hormuz still closed or having re-opened would be very different, so the pressure on getting a resolution remains considerable. Crude oil prices have softened a touch with no development in the Middle East to explain that and it looks like there is hope building that the summit in China between President Trump and President Xi could provide some momentum toward reaching a deal with President Xi acting as an influence on Iran.

Time remains crucial here and further upward pressure on yields is likely to build over the coming days and weeks if there is no resolution to the closure of the Strait of Hormuz. The AI-related euphoria and strong momentum remains a key counter to the risk of an equity market correction of any note, but the higher yields go on inflation concerns the AI-related momentum could well fade at these more elevated levels. So increased volatility on higher yields in the US is a key risk that would likely propel the dollar stronger. Bond markets will be key over the coming days and weeks for broader markets with inflation risks, as seen in the CPI report, rising.

ISM PRICES PAID POINT TO US INFLATION UPSIDE RISKS STILL LIE AHEAD

Source: Bloomberg, Macrobond & MUFG GMR

GBP: Starmer hangs on but risks remain

The pound is the second worst performing G10 currency this week underlining the underperformance related to the upturn in political uncertainties. It was looking highly likely this time yesterday that PM Starmer was about to step down as prime minister but his refusal and his call-out to backbenchers for someone to challenge him has gone unanswered, suggesting, for now at least, that his tenure as PM can carry on.

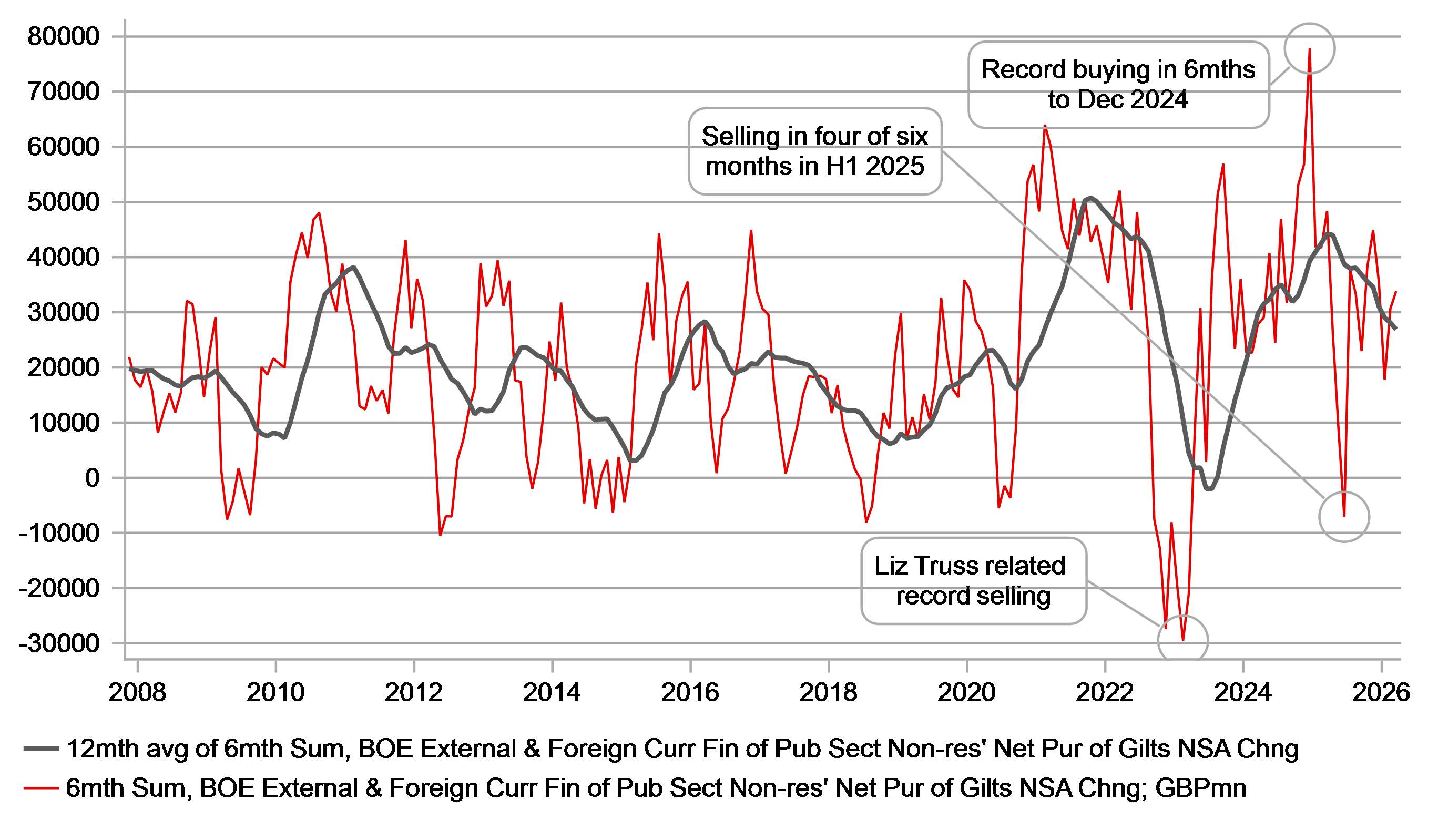

Starmer’s confirmation that he was not reigning did mark the time of the peak in Gilt yields so the decision does look to have helped contain the risk of a nastier rise in yields that could destabilise broader UK markets. But the 30-year Gilt yield ultimately ended 4bps down from that peak – so hardly a dramatic turn. That’s understandable given the risk associated with his resignation remains. A total of around 90 MPs have now called for him to step down while 4 ministers have resigned. Still, no Secretary of State has taken that step and hence there is an appearance of unity within cabinet. Shabana Mahmood, the Home Secretary, has not publicly called for Starmer to resign. But there are widespread reports of divisions with numerous media reports that as many as six cabinet members asking the PM to confirm a timeline for stepping down. There is a hesitancy of course in candidates coming forward given the apparent most popular candidate for taking over from Starmer is not even an MP! How realistic is to arrange for a by-election and have Andy Burnham fast-tracked back to parliament? Wes Streeting will reportedly have a meeting with PM Starmer this morning.

A shift to the left is what could create an extended bout of Gilt market stability and Burnham could imply a policy shift to the left, albeit a slightly smaller shift than a leadership under Angela Rayner. This political turmoil is happening at the worst time given the upturn in global inflation risks due to the conflict in the Middle East and with this uncertainty set to persist and potentially get worse, a period of renewed pound underperformance is the obvious conclusion. We were already assuming EUR/GBP would drift higher to 0.8850 by year-end but if this uncertainty persists and we do see new leadership and a shift left in policy, higher levels through 0.9000 is possible.

FOREIGN INVESTOR DEMAND FOR UK GILTS TO MARCH HELD UP WELL BUT WAS WEAKENING

Source: Macrobond, Bloomberg & MUFG Research

GBP: Has the resignation threshold been met?

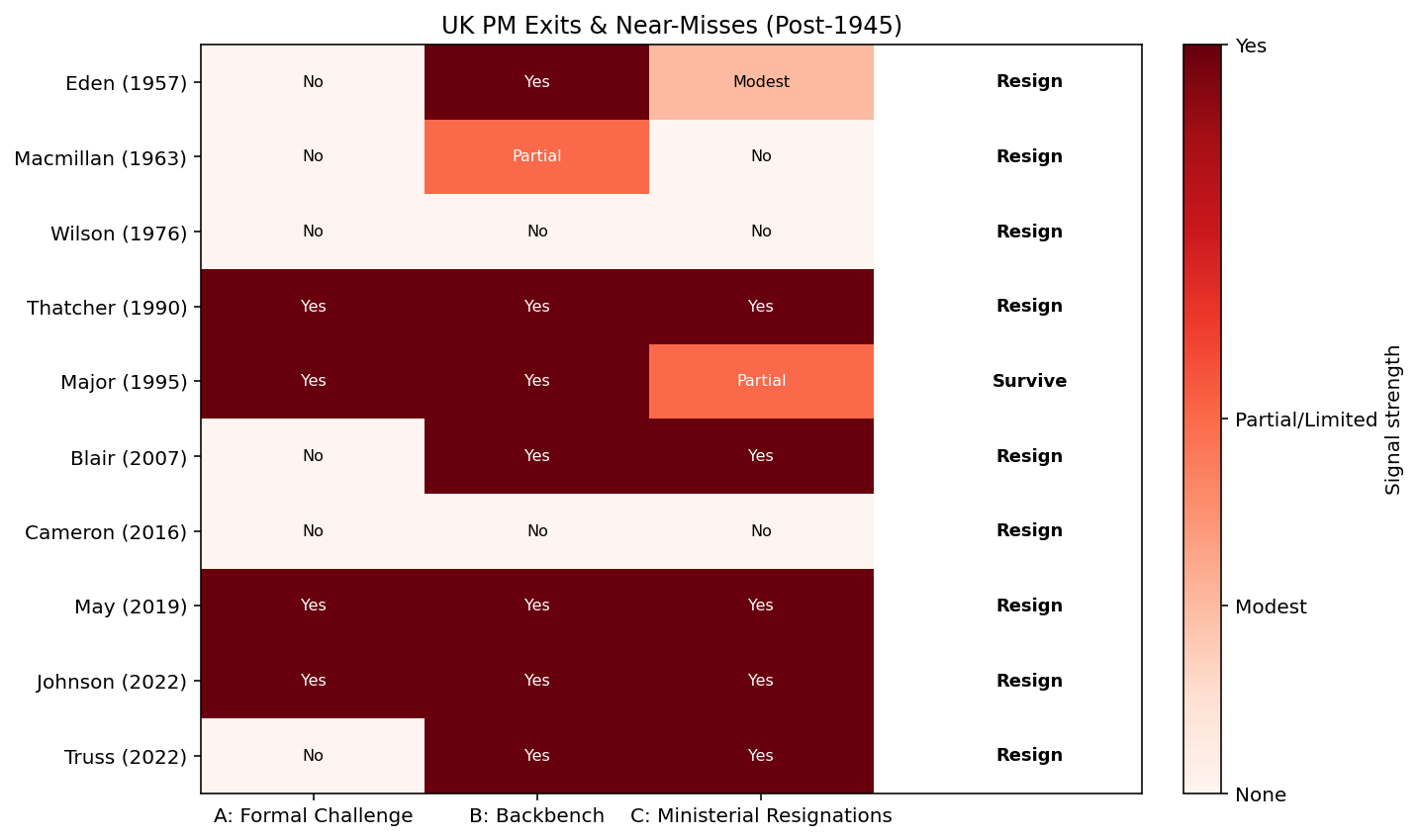

Should Prime Minister Keir Starmer leave his post, this would mark the fifth consecutive UK prime minister to depart office mid-term. Modern UK prime ministers rarely resign mid-term without strong internal pressures building first. In almost every instance since 1945 where a prime minister has stepped down early, there were clear signals from within their own party. Our analysis finds these include:

· Organized backbench dissent in the form of rebellions and letters of no confidence

· Formal leadership challenges

· and waves of ministerial resignations.

History suggests critical thresholds for dissent emerge around 30-40% of a governing party's MPs making explicit opposition clear. Boris Johnson's internal confidence vote revealed 41% disloyalty, within four weeks of the vote, rebels capitalized on this weakness and he fell. Combination signals are key as no single trigger guarantees a PM's downfall. The most predictive scenario involves multiple red flags occurring simultaneously resulting in a “pile-on” effect.

Tony Blair’s departure illustrates this dynamic. Following speculation of a leadership challenge, backbench agitation following the Iraq War, and resignations by Brown's allies in 2006, this effectively forced Blair to set a resignation date. However, not all leadership resignations fit this pattern, voluntary departures (Harold Wilson) and external shocks (David Cameron) are outliers. Starmer faces pressure following the latest local election results on 7th May. As of now, 89 Labour MPs have publicly called for his resignation (22% of the parliamentary party). Four ministers have resigned, each explicitly demanding his departure, and backbench revolt continues to gain momentum. For this reason, while formal challenges remain muted and no key minister has resigned, backbench dissent is building, though not yet reaching the critical 30–40% threshold historically associated with prime ministerial downfall.

UK PM EXITS & NEAR MISSES

Source: JSTOR, Statista, politics.co.uk

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 10:00 | GDP (QoQ) | (Q1) | 0.1% | 0.1% | !! |

EU | 10:00 | GDP (YoY) | (Q1) | 0.8% | 0.8% | !! |

EU | 10:00 | Industrial Production (MoM) | (Mar) | 0.2% | 0.4% | !! |

US | 10:00 | IEA Monthly Report | - | - | - | !!!! |

EU | 10:00 | Industrial Production (YoY) | (Mar) | -1.8% | -0.6% | ! |

EU | 10:00 | Employment Change (QoQ) | (Q1) | 0.1% | 0.2% | ! |

DE | 10:30 | German 30-Year Bund Auction | - | - | 3.570% | ! |

US | 13:30 | PPI (MoM) | (Apr) | 0.5% | 0.5% | !!! |

US | 13:30 | Core PPI (MoM) | (Apr) | 0.3% | 0.1% | !!! |

US | 13:30 | PPI (YoY) | (Apr) | 4.9% | 4.0% | ! |

US | 13:30 | Core PPI (YoY) | (Apr) | 4.3% | 3.8% | ! |

GB | 15:00 | BoE's Mann speaks | - | - | - | !!! |

US | 16:30 | Fed's Collins Speaks | - | - | - | !! |

GB | 18:00 | BoE's Mann speaks | - | - | - | !! |

US | 18:00 | 30-Year Bond Auction | - | - | 4.876% | !! |

US | 18:15 | Fed's Kashkari Speaks | - | - | - | !!! |

CA | 18:30 | BOC Summary of Deliberations | - | - | - | ! |

EU | 20:00 | ECB's Lane Speaks | - | - | - | !! |

EU | 20:15 | ECB President Lagarde Speaks | - | - | - | !!! |

Source: Bloomberg & Investing.com