Lack of progress in peace talks support USD after stronger NFP report

USD: Fallout from Middle East peace plans & latest NFP report in focus

The US dollar has staged a modest rebound at the start of this week helping to lift the dollar index back above the 98.000-level which has provided good support over the past month. The US dollar has derived support overnight from reports that the US and Iran have both rejected each other’s latest peace proposals putting a dampener on investor optimism that a deal could be reached soon to end the conflict and re-open the Strait of Hormuz. President Trump described Iran’s latest proposal as “TOTALLY UNACCEPTABLE”. According to the WSJ, Iran offered to transfer some of its stockpile of highly enriched uranium to a third country but rejected the idea of dismantling its nuclear facilities. However, Iran’s semi-official news agency Tasnim stated that the WSJ’s reporting on the proposals for handling nuclear material was “not true”. The state-run IRIB News added that Iran has also rejected President Trump’s latest plan describing it as tantamount to surrender and insisted that the US must pay war damages. The US had proposed that ran permit passage through the Strait and Washington would end its blockage of Iranian ports in the next month. The latest developments continue to highlight the risk of a more prolonged closure of the Start of Hormuz which would be disruptive for the global economy and financial markets. The lack of progress in peace talks has lifted the price of Brent back above USD105/barrel overnight. The negative spillover impact on investor risk sentiment and high beta currencies has been muted so far.

At the same time, the US dollar has been supported in part by the release of the stronger than expected nonfarm payrolls report for April. The report revealed that the US economy added 115k jobs in April following on from the upwardly revised increase of 185k in March. It was the first two consecutive months of job growth since April and May of last year. The report provides further reassuring evidence that the US labour market appears to have strengthened in 2026 after the weak end to last year. Employment growth has averaged 76k/month in the first four months of this year compared to average jobs losses of -10k/month in the final four months of last year. It supports the Fed’s view that downside risks to the labour market have eased which alongside the energy price shock has helped to ease pressure on the Fed to deliver further rate cuts in the near-term. However, the report was not strong enough to encourage the US rate market to price in Fed rate hikes curtailing support for a stronger US dollar. In contrast, the household survey was much weaker revealing job losses of -226k while the labour force shrunk again by -92k. Still, the unemployment rate held steady at 4.3%. Overall, we believe the latest developments favour the Fed leaving rates on hold.

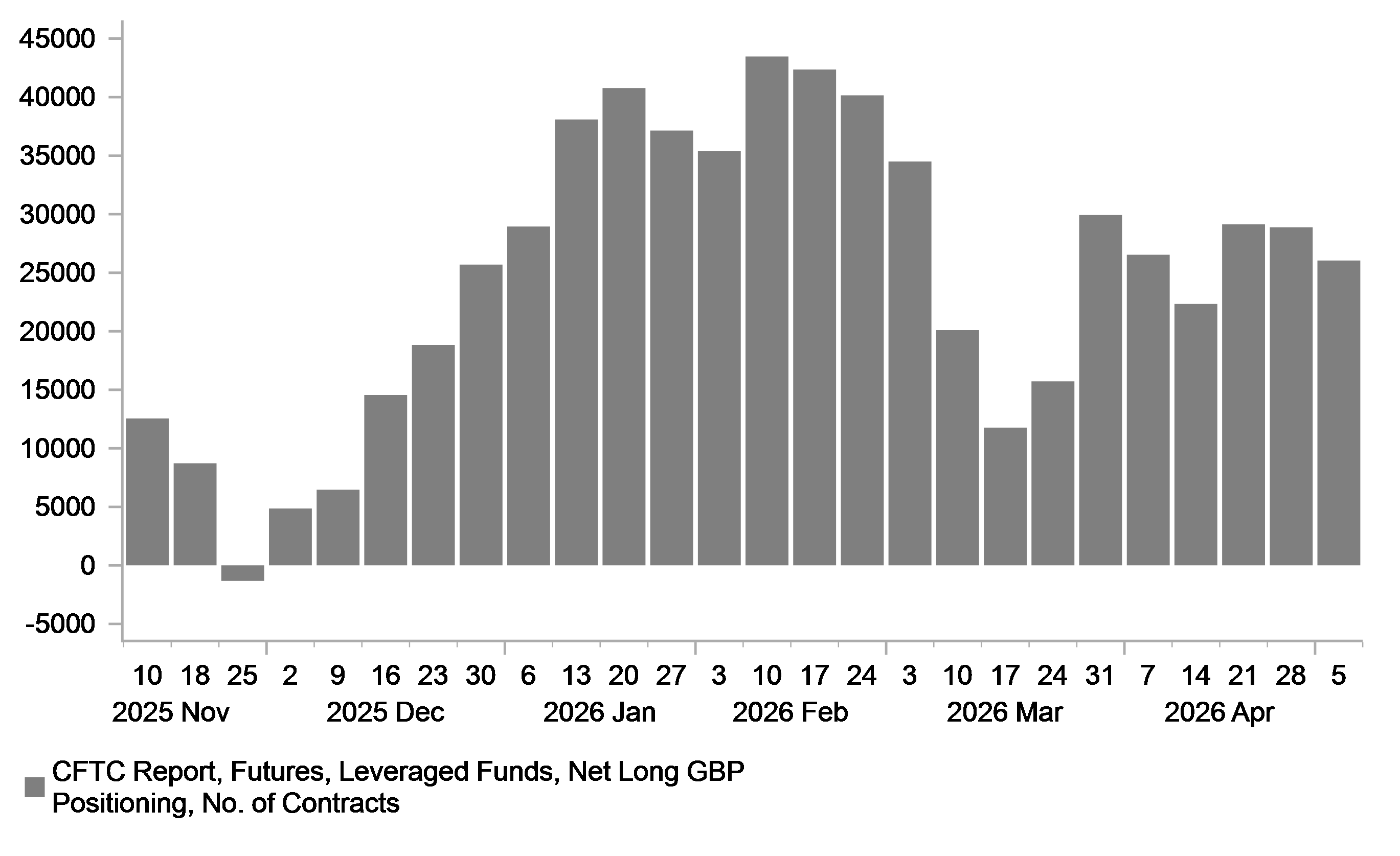

LONG GBP POSITIONS REMAIN POPULAR BUT HAVE BEEN SCALED BACK

Source: Bloomberg, Macrobond & MUFG GMR

GBP: PM Keir Starmer on shaky ground but how long can he cling on?

The pound has softened modestly at the start of this week resulting in cable falling back below 1.3600 and EUR/GBP rising above 0.8650. The pound is starting this week on a softer footing reflecting renewed uncertainty related to UK politics as the dust continues to settle following last week’s disappointing local election results for the government. It has been reported that Prime Minister Keir Starmer will make a last-ditch speech today to try to save his premiership. He is expected to lay out a plan to turn the party’s fortunes around, including a commitment to take the UK closer to the EU. He will vow to “face up to the big challenges” and concede that “incremental change won’t cut it”.

He faces the prospect of an immediate leadership challenge from Catherine West if she is still “dissatisfied” after hearing his keynote speech today. However, it is far from clear that she will be able to secure the backing of one fifth of Labour MPs (81) required to formally trigger a leadership contest. At the same time, it has been reported that Health Secretary Wes Streeting is “ready to go” according to his allies if a formal leadership content is triggered. Another potential leadership candidate former Deputy Prime Minister Angela Rayner issued a statement calling on Starmer urgently change the direction of his government, and saying it was a mistake to have blocked Greater Manchester Mayor Andy Burnham from standing in a special election earlier this year. While she did not directly challenge the Prime Minister, the statement clearly expressed dissatisfaction with the current policies. Her call to allow Andy Burnham to be allowed to run to become an MP again also indicates that he is her preferred potential leadership candidate from the left of the party.

The latest developments over the weekend have increased the risk of political uncertainty intensifying in the near-term which could weigh more heavily on pound performance. The probability of Stamer being removed by June according to Polymarket has picked up to around 40% and is as high as 65% by the end of this year. The writing appears to be on the wall for Keir Stamer’s premiership, and it is now more about how long he can cling on to power. We continue to believe that a shift to the left for the Labour party would trigger at least a temporary period of pound selling.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

US | 15:00 | Existing Home Sales | (Apr) | 4.05M | 3.98M | !!! |

US | 15:00 | CB Employment Trends Index | (Apr) | - | 105.72 | ! |

GB | 15:40 | BoE Deputy Governor Woods Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com