Retaliatory strikes have muted FX market impact ahead of US CPI report

USD: Muted market response to US retaliatory strikes against Iran

The main development overnight was the announcement from the US that it has carried out retaliatory military strikes against Iran. It follows Iran’s attack on a US Apache helicopter off the coast of Oman. US Central Command have stated that their retaliatory strikes have “struck Iranian air defence, ground control stations and surveillance radar sites near the Strait of Hormuz with precision munitions”. It added the operation had been completed and described the operation as a “proportional response to recent attacks on U.S. forces and international commercial ships transiting regional waters”. The choice of language suggests that the U.S. is seeking to contain the renewed confrontation with Iran. Market participants will now be watching to see how Iran responds. Iran’s Foreign Minister Abbas Araghchi posted on social media that they “will leave no attack or threat unanswered”. The initial market response to renewed military strikes between Iran and the US has been relatively muted suggesting confidence that the fallout will be contained. The price of Brent crude oil continues to trade close to recent lows after briefly falling back below USD90/barrel yesterday.

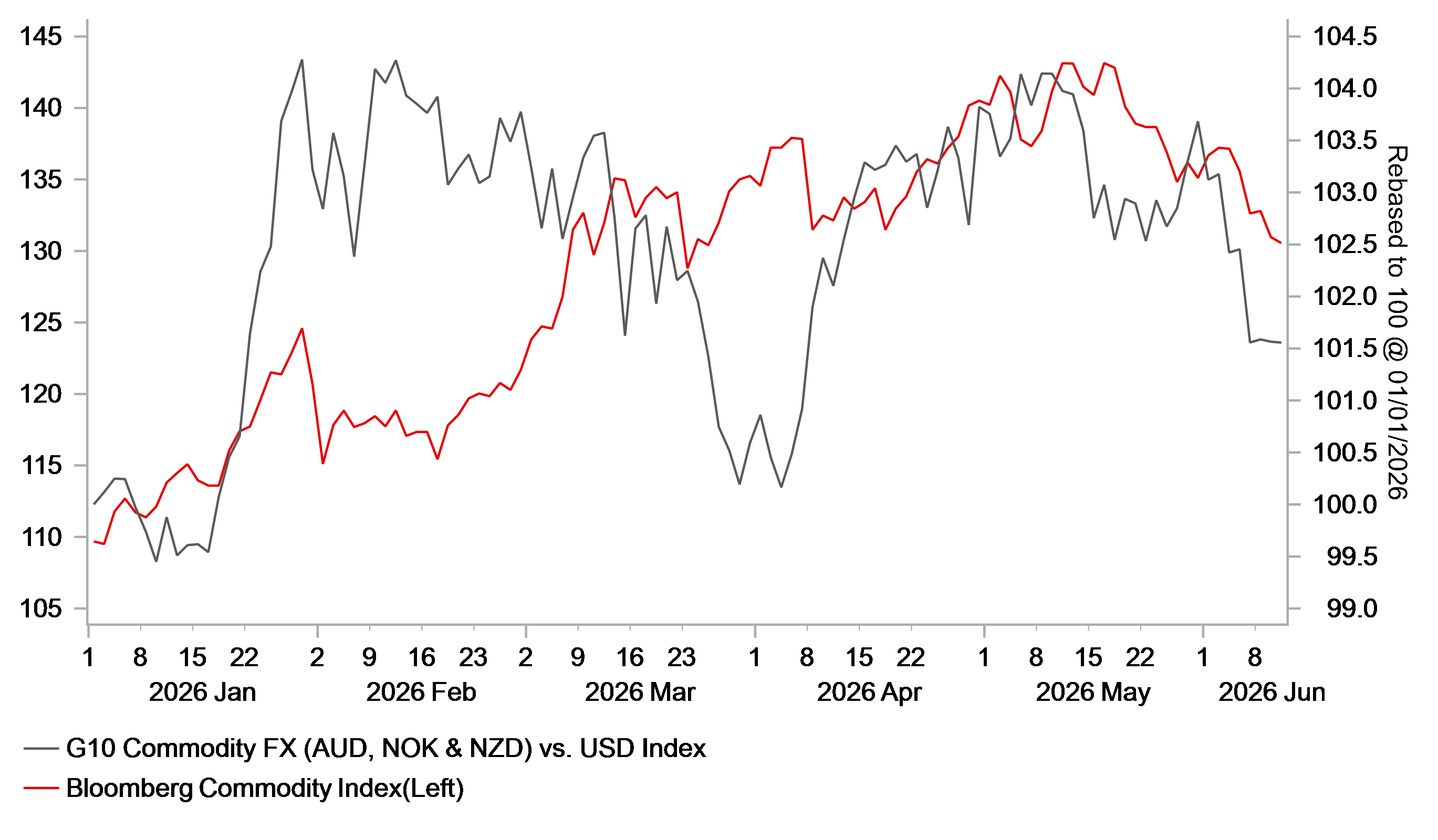

Similarly, in the foreign exchange market the major currency pairs are little changed overnight. The G10 commodity currencies of the New Zealand dollar, Norwegian krone and Australin dollar have underperformed so far this month alongside the correction lower for commodity prices. After peaking on 18th May, Blooomberg’s commodity price index has fallen by almost 9% giving back over half of the gains recorded since the Middle East conflict started in late February. At the same time, the recent pick-up in US yields and stronger US dollar has created a more challenging backdrop for carry trades in the near-term. FX carry trades have performed strongly this year supported by the relatively low level of financial market volatility including in the foreign exchange market. The start of the Middle East conflict only triggered a short-lived and modest pick-up in financial market volatility in March only temporarily disrupting carry trade performance. Bloomberg’s FX carry index has risen by just over 5% this year extending the strong run of positive returns since the middle of last year.

COMMODITY PRICES & CURRENCIES HAVE BEEN CORRECTING LOWER

Source: Bloomberg, Macrobond & MUFG Research

USD: Will US CPI report encourage further USD strength?

Today’s US CPI report is the most consequential data release ahead of the upcoming FOMC meeting. Consensus expects headline inflation to breach 4% YoY for the first time since 2023, driven primarily by the energy price shock stemming from the Middle East conflict. While this move appears significant on the surface, May 2025 delivered the softest CPI print of 2025, creating a low base that mechanically lifts the year-on-year comparison even if underlying inflation remains moderate. That said, the primary driver of the expected rise in headline inflation is energy prices. While weekly gasoline prices have begun to ease in recent weeks, this recent decline is unlikely to materially impact the May CPI report. Beyond headline inflation, there are signs of a risk of broadening inflationary pressure. Core CPI picked up in April marking a modest re-acceleration. Services and shelter remain the stickier components, consistent with the pattern observed since 2023. So far, the re-acceleration is modest and concentrated.

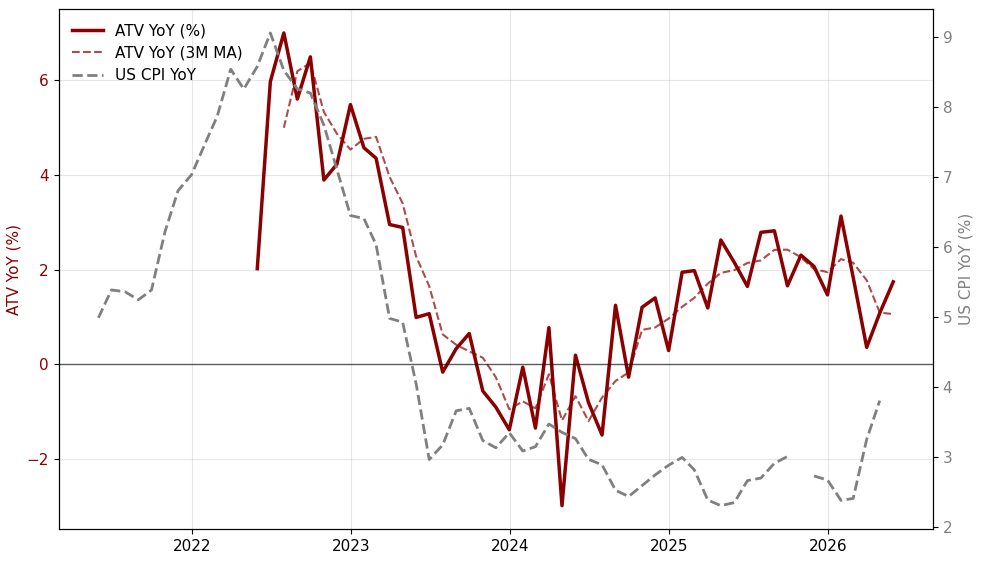

A hot print CPI (>4.3%) today would likely trigger a sharp sell-off in US front-end rates as markets price in a higher probability of further Fed tightening, potentially pulling forward expectations for a hike towards October. The USD would rally on widening rate differentials, pushing USD/JPY up towards 161.00–162.00. While a soft print (<4.0%) would trigger lower US yields and a weaker US dollar pulling USD/JPY back below 160.00. Looking at alternative data indicates upside risks. Transaction data from major US retailers shows rising average transaction values and resilient sales despite weaker foot traffic, suggesting ongoing price pass-through, particularly in food and core goods. Taken together, while base effects will exaggerate the YoY increase, underlying signals point to persistent inflation pressures. With the distribution of outcomes unusually wide, today’s CPI release carries heightened potential for outsized market moves relative to recent data prints.

WALMART AVERAGE TRANSACTION VALUE YOY VS. US CPI YOY

Source: Bloomberg, Macrobond & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

US | 13:30 | CPI (YoY) | (May) | 4.2% | 3.8% | !!! |

US | 13:30 | Core CPI (YoY) | (May) | 2.9% | 2.8% | !!! |

CA | 14:45 | BoC Interest Rate Decision | - | 2.25% | 2.25% | !!! |

CA | 15:30 | BOC Press Conference | - | - | - | !!! |

Source: Bloomberg & Investing.com