Yen gains as Katayama signals policy shift – but change will take time

JPY: MoF calls on GPIF to buy domestic assets

The yen is the top performing G10 currency today with the move triggered by a remark at a regular press conference by Finance Minister Katayama. In discussing government investment plans Katayama stated that it was now a government priority to “encourage households, as well as pension funds including the GPIF, to increase their investments in Japanese financial assets”. This has come from nowhere and hence the surprise has had a notable impact not just on the yen but on equities and JGBs with yields down over 10bps. This also marks a departure from one aspect of Abenomics. As part of Japan’s reflation policy, the Abe government encouraged greater risk taking, including investing in higher yielding foreign securities as a means of instilling confidence in Japan’s pension system. The view then was that households’ concerns over the pension system in Japan was encouraging greater household saving. By boosting returns on pensions via greater risk-taking, it would help restore confidence and reduce household savings and increase spending.

So in that broader context, this is a significant moment. But what does this mean for the financial markets over the short-term? These policy shifts take time and ultimately, we would argue there remains an important fundamental fact that needs to fall into place in order for pension funds and other investors to send less capital abroad and invest more in JGBs – confidence in the BoJ and reduced fears over the BoJ being behind the curve. So we are unlikely to see any notable shift any time soon.

However, this feels like a theme that could get greater focus and encouraged by government policy it could certainly have an impact over time. The big overhaul of the asset allocation of the GPIF was in 2014 and pre-2014 the domestic bond allocation was 60% but in 2014 was reduced to 35% and then in April 2020 was reduced to 25%. The Ministry of Health, Labour and Welfare sets the medium-term objectives and then the GPIF chooses the composition. So if the government objective was to change this would ultimately get reflected in changes in GPIF asset compositions.

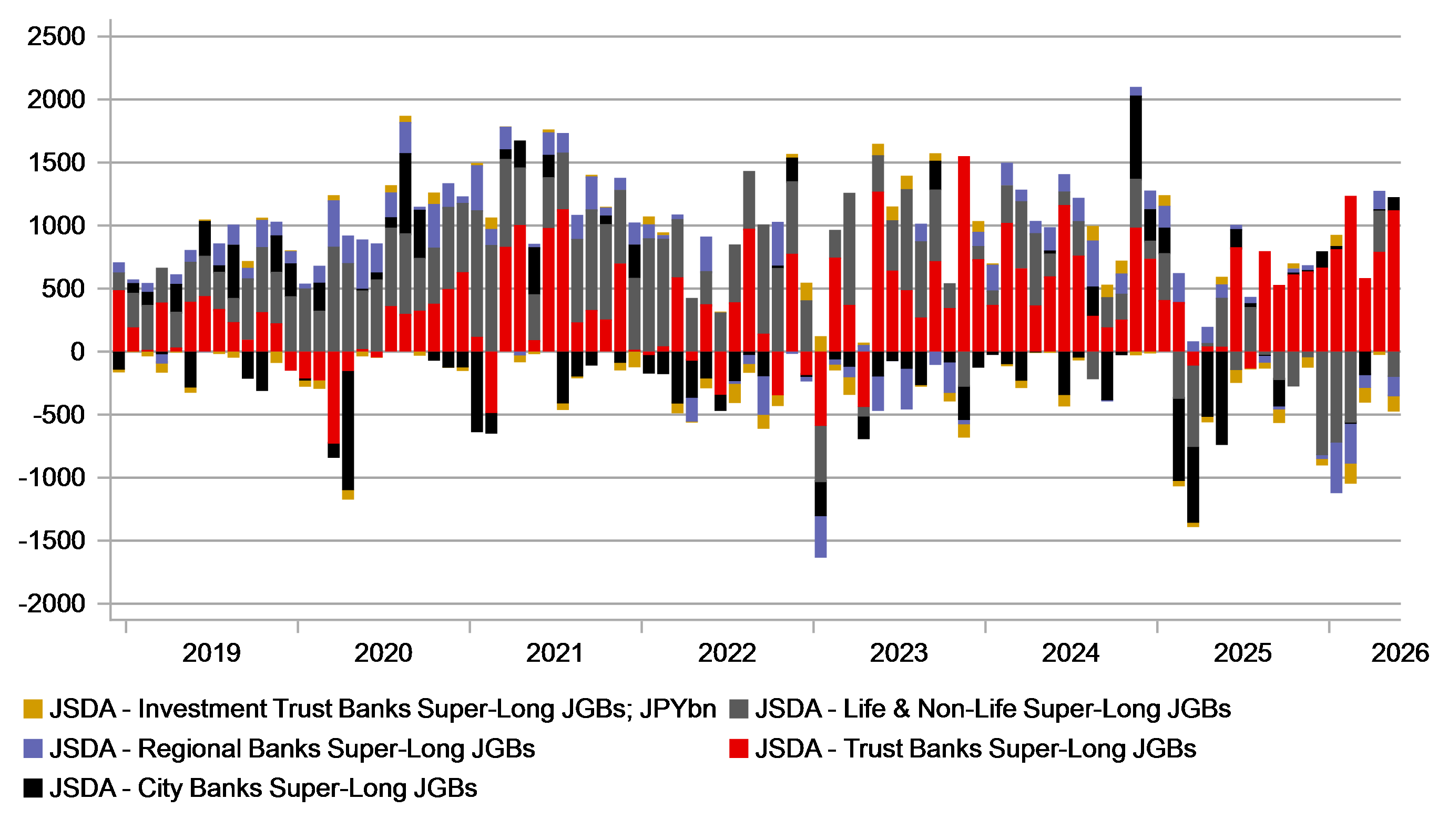

For now the markets will likely start to watch flows more closely. The chart above shows Japan Trust buying of super-long JGBs which would include GPIF and there has been some gradual increased buying. The asset compositions as of end FY25 are: domestic bonds 26.9%; domestic equities 23.8%; foreign bonds 24.5%; and foreign equities 24.8%, all reasonably close to the 25% level. Foreign equities, and domestic bonds and equities have a +/-6% leeway while foreign bonds have a +/-5% leeway.

It’s probably too soon to expect this to have any lasting impact on the yen and as stated above, BoJ credibility and reducing fears over being behind the curve remain key. There is also a risk that near-term the markets view Katayama’s comment as a sign of reduced appetite for MoF intervention and could help encourage renewed yen selling if yields globally were to move further higher.

JAPAN DOMESTIC INVESTOR BUYING/SELLING OF SUPER-LONG JGBS

Source: Bloomberg, Macrobond & MUFG Research

EUR: ECB minutes provided limited new information

The German 2-year yield traded in a narrow range yesterday – 2.65%-2.69% - and the release of the ECB minutes from the meeting in June when the policy rate was hiked offered only limited new information. The key take-away from our perspective was the indication in the minutes that the ECB wanted to ensure that its rate hike in June was neither portrayed as a one-off nor as the start of a series of hikes. That would certainly be consistent with a number of Governing Council members seeing the potential benefit of a further hike before being in a position to remain on hold for longer. The only other observation of note was the reference to the inflation projections being built, in part, on energy prices in the futures market and prices would need to drop back along the curve otherwise it would feed into higher inflation than expected. While Brent crude oil has dropped back to levels below, prices are obviously rising again. For natural gas prices, the TTF price remains higher than the ECB assumed when the forecasts were updated in June. In that context we see continued risks of the ECB acting again consistent with our current forecast of another 25bp hike in September.

The ECB will be certainly less concerned over longer-term inflation expectations becoming un-anchored with the 5y5y inflation swap rate having declined since the initial ceasefire was agreed. Even now following the re-escalation of the conflict and the rebound in crude oil prices, the 5y5y inflation swap rate at 2.11% is exactly in line with the average over the last twelve months. If crude oil and/or natural gas prices were to rebound sharply then risks will rise of course but at this point longer-term inflation expectations remain well anchored.

The speed in which crude oil prices dropped likely points to a bearish fundamental backdrop that is curtailing investor appetite for buying crude oil. While security of supply could become a big issue once again there has been evidence emerging of Middle East producers shifting focus to competing for market share. That could also be helping curtail a rebound in crude oil prices. Saudi Aramco cut its OSP (Official Selling Price) to Asia by USD 6pbl in July and a further USD 11pbl in August, the largest reduction in two decades.

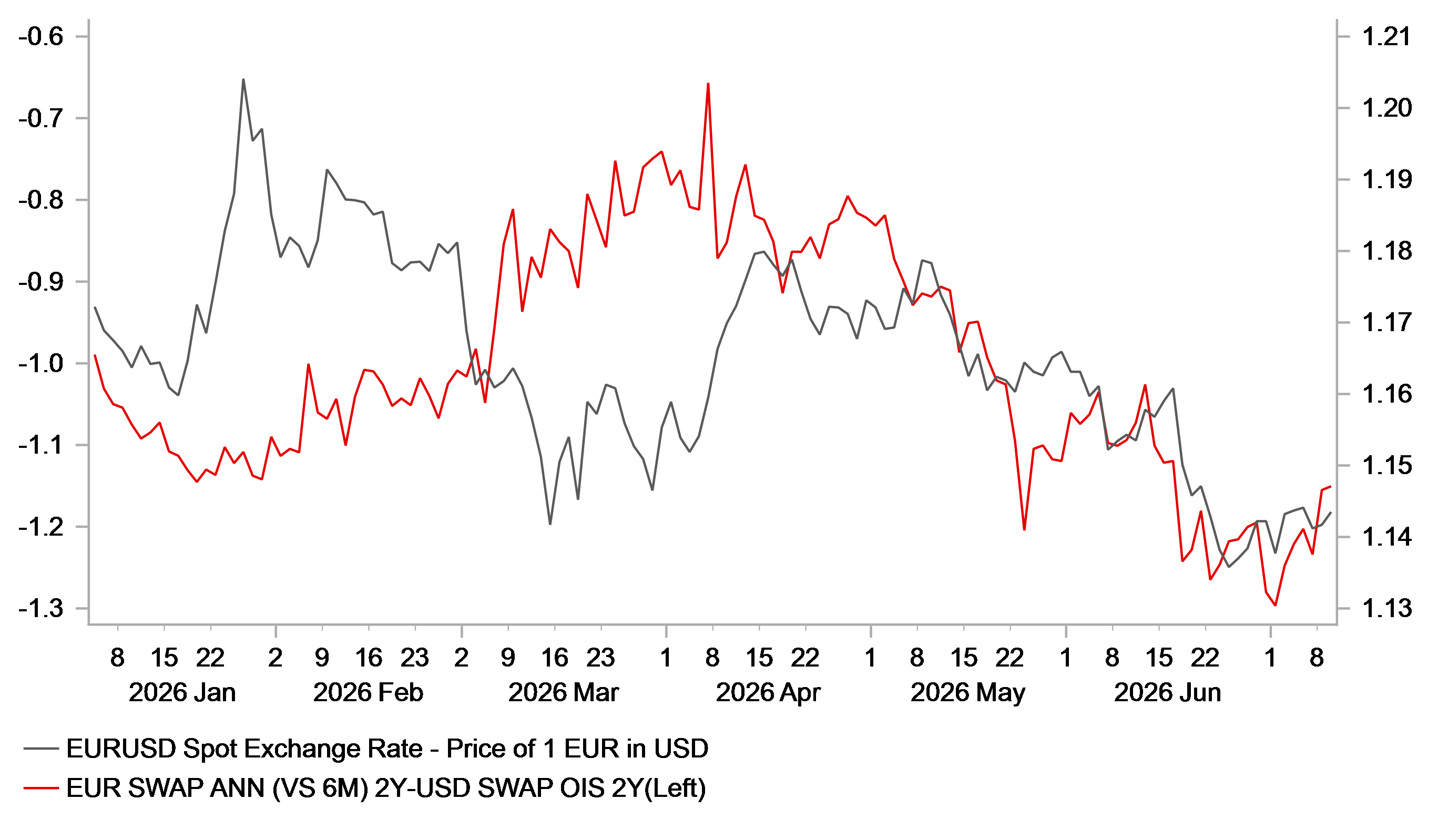

The euro is currently the worst performing G10 currency in July but the 2-year yield spread has started to turn in favour of some moderate EUR/USD recovery. That reflected a sharper jump in yields in Europe relative to the US. The ECB minutes should at least reinforce the current pricing of another rate hike in Europe while for the US next week’s CPI release and Fed Chair Warsh’s semi-annual testimony will be crucial for short-term yields. We continue to see risks of US yields turning lower that should reinforce renewed upward momentum for EUR/USD.

FRONT-END EURO-ZONE YIELDS SPREAD OVER US TURNING HIGHER

Source: Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

IT | 09:00 | Industrial Production MoM | May | -0.2% | 0.5% | !! |

CA | 13:30 | Net Change in Employment | Jun | 10.0k | 87.8k | !!! |

CA | 13:30 | Unemployment Rate | Jun | 6.6% | 6.6% | !!! |

Source: Bloomberg & Investing.com