JPY remains weak in run up to BoJ policy meeting

USD: Middle East risks & Fed policy outlook remains key for USD performance

The US dollar lost upward momentum yesterday after the dollar index ran into resistance at the 100.00-level. It followed reports that Iran and Israel have agreed to ease strikes against each other after the tit-for-tat strikes over the weekend threatened to derail peace negotiations. Israel’s Prime Minister Benjamin Netanyahu stated that Israel would hold fire in Iran for now but would respond should they attack again. Iran had earlier announced an end to its own military operations against Israel. However, they did warn that if Israel continued to attack, including southern Lebanon, then “much harsher and more crushing actions than before would be on the way”. Investor optimism triggered by the de-escalation in military tensions between Israel and Iran has since been encouraged by comments from President Trump overnight who stated he expects to declare total victory “very soon”, and “oil prices will come tumbling down”. He made the comments during a tele-rally for South Carolina Republicans. The latest developments have resulted in the price of oil dropping back closer to recent lows at just above USD90/barrel.

Nevertheless, the US dollar is still continuing to derive more support from the recent hawkish repricing of Fed rate hike expectations. The US rate market has moved to price in multiple Fed rate hikes in the year ahead moving market expectations for the Fed policy outlook more into line with other major central banks such as the ECB who are expected to begin their own tightening cycle this week. It has resulted in yields spreads moving back in favour of the US dollar over the last couple of months. The next key test for the Fed rate hike expectations will be the release tomorrow of the latest US CPI report for May. The report is expected to reveal that headline inflation rose further above the Fed’s target to 4.2% in May as the impact of higher energy prices continues to feed through. At the same time core inflation is expected to move closer to 3.0% in May. While the pick-up in inflation is well anticipated in the coming months, it could add to investor unease over the Fed’s willingness to continue looking through higher inflation by leaving rates on hold. The next FOMC meeting on 17th June is likely to be an important pivot point for Fed policy expectations and the US dollar as it will be the first time that new Fed Chair Kevin Warsh will outline his thoughts on how the Fed should respond to the energy price shock. Last week’s stronger nonfarm employment report has made it more likely that the Fed will at least drop their easing bias at the June FOMC meeting.

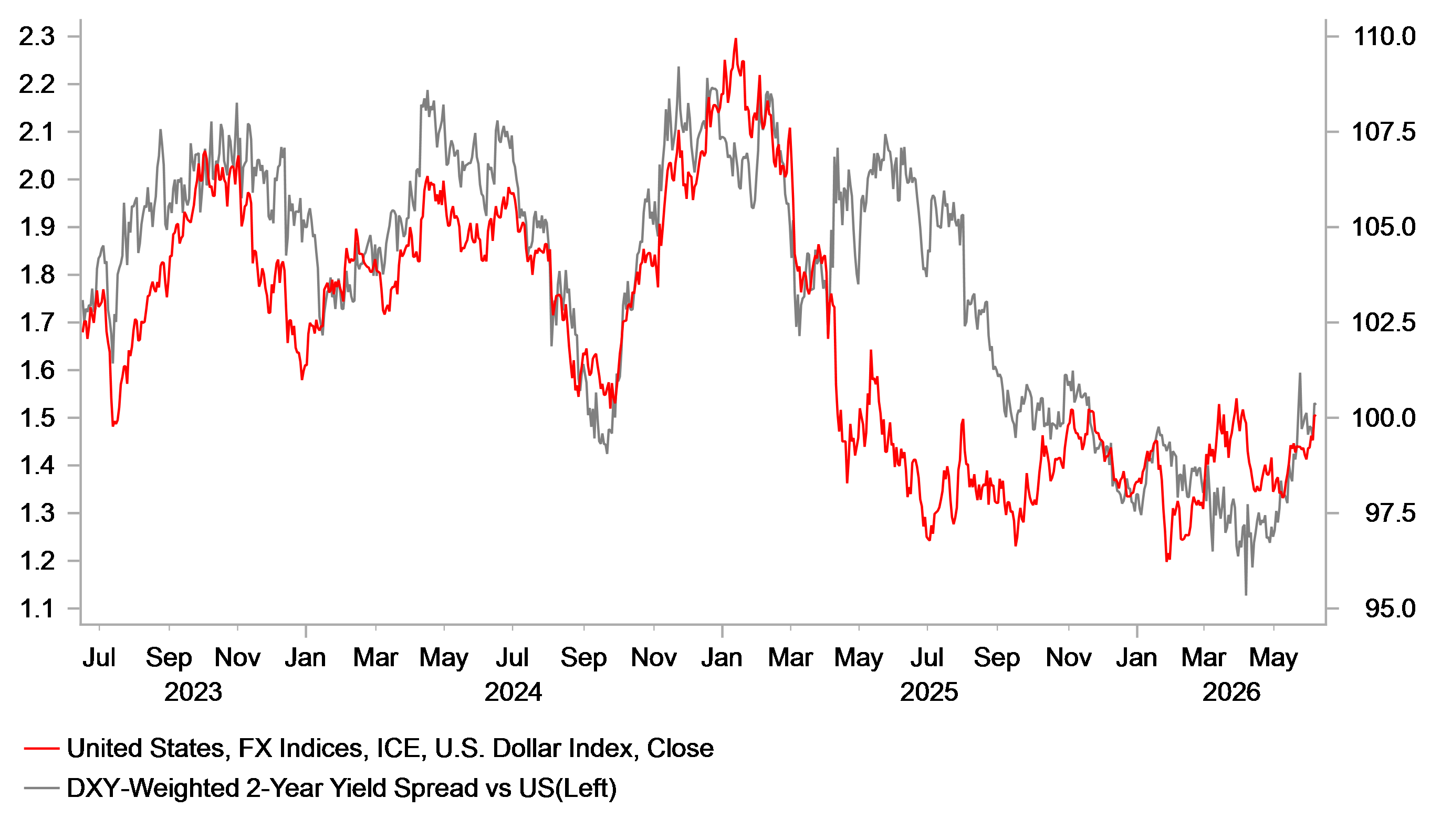

YIELD SPREADS MOVING BACK IN FAVOUR OF USD

Source: Bloomberg, Macrobond & MUFG Research

JPY: BoJ set to hike rates & pause JGB tapering from FY2027

The yen has continued to trade on a weaker footing at the start of this week after USD/JPY rose back above the 160.00-level. The continued weakness of the yen keeps pressure on Japanese policymakers to provide more support through further intervention and/or by the BoJ tightening monetary policy. A BoJ rate hike at the upcoming policy meeting on 16th June is almost fully priced in now so is unlikely to trigger a significant reversal of yen weakness on its own if delivered. Failure to follow through and hike rates again would trigger a much bigger negative market reaction for the yen adding to investor concerns that the BoJ is behind the curve in fighting inflation risks in Japan. As a result, it appears highly unlikely that the BoJ will not raise rates this month.

A Nikkei report released overnight stated that they have learned that the BoJ is set to raise its key interest rate to 1.00%, and is also considering pausing the tapering of its government bond purchasing program starting in April 2027. Under current plans, the BoJ is reducing the size of monthly JGB purchases by around JPY200 billion per quarter from April 2026 to March 2027. Before that JGB purchases had been reduced by around JPY400 billion per quarter from mid-2024 through to March 2026. A decision to pause tapering from the next fiscal year would help to ease selling pressure in the JGB market. 10-year and 30-year JGB yield have both fallen sharpy overnight by around 6bps and 9bps respectively. Overall, the latest developments have not changed our view that the yen is likely to remain weak in the near-term until the worst of the energy price shock begins to fade.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

US | 11:00 | NFIB Small Business Optimism | (May) | 96.0 | 95.9 | ! |

CA | 13:30 | Trade Balance | (Apr) | 2.50B | 1.78B | !! |

US | 13:30 | Trade Balance | (Apr) | -56.20B | -60.30B | !! |

US | 15:00 | Existing Home Sales | (May) | 4.07M | 4.02M | !!! |

EU | 17:30 | ECB President Lagarde Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com