FOMC minutes & Middle East risks provide cross currents for USD

USD: FOMC minutes dampen support from renewed Middle East tensions

The US dollar has continued to consolidate at stronger levels so far this week with the dollar index oscillating around the 101.00-level. The US dollar initially attempted to regain upward momentum yesterday after the latest round of military strikes between the US and Iran. The US Central Command has confirmed that its forces targeted sites in Iran for the second consecutive day yesterday “to further degrade” Tehran’s ability to attack commercial shipping in the Strait of Hormuz. The US targeted and hit about 90 sites including air defence systems, coastal surveillance assets, and missile and drone storage sites. In response the Islamic Revolutionary Guard Corps have stated that they struck US bases in Kuwait and Bahrain and have threatened to expand the attacks. The renewed hostilities in the region have reported resulted in traffic through the Strait of Hormuz coming to a near standstill. The latest developments pose the biggest threat yet to the ceasefire that was extended by the memorandum of understanding signed on 17th June. They even prompted President Trump to state “I think it’s over. I don’t want to deal with them anymore”. He added that further negotiations with Iran were likely a “waste of time”. On the other hand, he noted that he’d let “our wonderful negotiators keep talking if they want”. Talks between the US and Iran could resume as soon as next week once Iran’s funeral proceedings for Ayatollah Ali Khamenei conclude.

The heightened risk of further disruption to energy supplies through the Strait of Hormuz has triggered a bigger reaction in the oil market. The price of Brent briefly rose back above USD80/barrel yesterday moving further above the recent low if USD70.14/barrel recorded on 2nd July. The price action is more in line with our initial thinking that the price of oil would continue to trade above pre-conflict levels to reflect the ongoing risk of negotiations breaking down along the way to finalizing a more sustained long-term peace deal. The spillovers so far into the foreign exchange market have been limited. The Norwegian krone has rebounded modestly after its recent correction lower. If tensions in the region were to intensify further and the price of oil continue to rise sharpy, it could reinforce the USD’s recent upward momentum especially now that the Fed has indicated that it is open to raising rates this year. US yields moved back towards recent highs yesterday.

However, the positive catalyst for the USD from the latest developments in the Middle East were partly offset yesterday by the release of the June FOMC minutes which were less hawkish than feared. The minutes revealed that the Fed does not appear to be in a rush to begin raising rates as soon as this month. At the June FOMC meeting, only “a few” participants commented that there was a case for raising rates at that meeting despite the updated DOT plot showing 9 participants now favoured hiking rates this year. The committee discussed various scenarios for how the US economy might evolve, including one in which inflation remains elevated and “some policy firming would likely be warranted”. But there was no clear indication that they were weighing up delivering a rate hike as soon as at the next policy meeting in July. Overall, the minutes support our view that the new Fed Chair Warsh will favour leaving rates on hold if energy prices remain at lower levels. We expect the US dollar to give back recent gains (click here) if Fed rate hike expectations are disappointed, although acknowledged that renewed tensions in the Middle East pose upside risks.

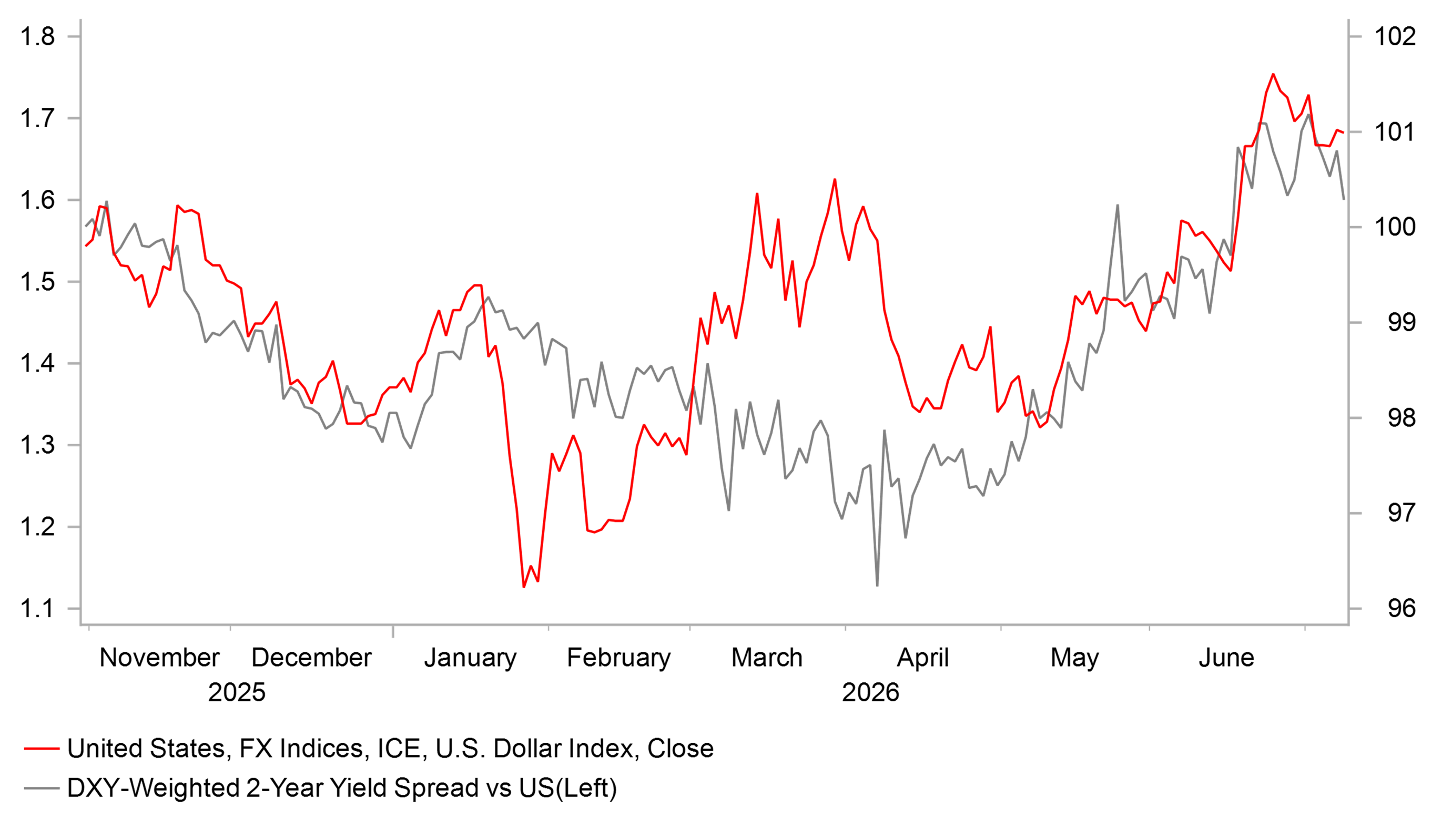

FED RATE HIKE EXPECTATIONS REMAIN KEY DRIVER FOR USD

Source: Bloomberg, Macrobond & MUFG Research

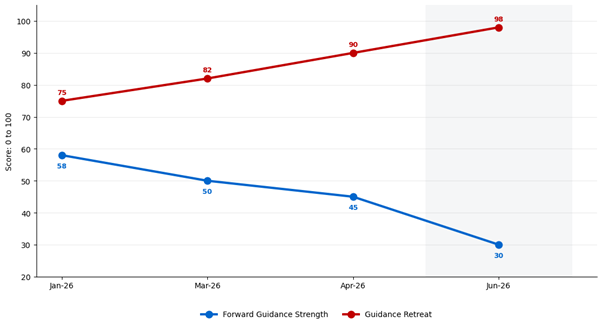

There was also a notable change in how the Committee communicated future policy. References suggesting a future path for rates faded considerably, while language emphasising flexibility and avoiding directional commitments intensified. Policymakers remained exceptionally clear about the factors that would influence decisions but became substantially less willing to signal what those decisions were likely to be. The change in communication style is consistent with Kevin Warsh’s desire to move away from providing forward guidance. It has been replaced by more scenario-based discussion.

FOMC MINUTES SHIFT AWAY FROM PROVIDING FORWARD GUIDANCE

Source: Federal Reserve & MUFG Research

EUR: ECB rate hike expectations & French political risks in focus

After attempting to break below the 1.1400-level again yesterday, EUR/USD has since risen back up to within touching distance of 1.1450 overnight. The euro has benefitted from the pullback for the US dollar after the FOMC minutes were less hawkish than feared, and the price of Brent dropping back below USD80/barrel overnight. At the same time, the euro-zone rate market has moved to price in a higher probability of further ECB rate hikes with the market leaning more towards two rather one final hike. The hawkish repricing has been encouraged by the jump in oil prices yesterday triggered by renewed tensions in the Middle East, and hawkish comments from ECB officials. Governing Council member Joachim Nagel indicated that further hikes maybe required while expressing concern by the renewed tensions in the Middle East. At current energy price levels, we remain comfortable with our call for one final hike in September.

The other development in Europe in recent days was the decision to allow National rally leader Marine Le Pen to run in next year’s presidential election in April. Bloomberg has reported results from an initial poll by Ifop-Fudicial for LCI and Le Figaro conducted after she declared her candidacy. The poll revealed that Le Pen jumped by four percentage points in voting intentions for the first round to 36% compared to 32% in a poll conducted between 22nd and 24th June. In two scenarios pitting Le Pan against former centrist prime ministers Edouard Philippe or Gabriel Attel, she also well ahead by 36% compared to 19% for Philippe, and by 36% compared to 15% for Attal. While the presidential election is still some way off, it is understandable that the initial financial markets and euro reaction has been muted but it should add to downside risks for the euro as we move closer to the election at the start of next year.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 11:00 | Eurogroup Meetings | - | - | - | !! |

EU | 12:30 | ECB Publishes Account of Monetary Policy Meeting | - | - | - | !! |

US | 13:30 | Initial Jobless Claims | - | 218K | 215K | !!! |

US | 14:00 | FOMC Member Williams Speaks | - | - | - | !! |

US | 15:00 | Existing Home Sales | (Jun) | 4.19M | 4.17M | !!! |

US | 18:30 | Fed Logan Speaks | - | - | - | ! |

Source: Bloomberg & Investing.com