Limited FX impact as US & Iran clash

JPY: Limited FX fallout with USD/JPY stable

We now have a reasonable idea that the BoJ spent in the region of JPY 10trn buying the yen in at least two bouts of intervention since 30th April. This is roughly similar to the amount spent in Apr-May 2024 that ultimately failed to strengthen the yen and by July that year the MoF / BoJ were intervening again. The risk with this latest intervention is that the broader global backdrop again does not support yen selling (in Apr/May 2024 front-end US yields remained elevated between 4.75% - 5.00%). The reports of clashes between the US and Iran in the Strait of Hormuz certainly raises the risk of a renewed jump in crude oil prices that scuppers Japan’s efforts to halt a move in USD/JPY through the 160-level. But for now, Brent crude oil remains close to the lows for the week, down 12% from the high on Monday. Trump referred to the clashes while the UAE stated that it had intercepted Iranian missiles and drones. Crucially though the US confirmed that the ceasefire remains intact.

Data released in Japan today could also add to risks that this bout of intervention fails. Labour cash earnings increased by 2.7% in March from a year earlier, down from 3.4% and below the consensus of 3.2%. Full-time base pay, excluding recent sample changes increased by 2.6%, down from 3.0%. With the growth definitely on the weaker side it could certainly reinforce the current cautious stance of the BoJ. Tokyo CPI data for April, released last week, also came in weaker than expected which could add to BoJ caution. The OIS curve indicates 18bps of hikes priced by the next meeting in June and we currently maintain our view that the BoJ will hike at that meeting. However, we assume there will be greater clarity on de-escalation and a peace deal between the US and Iran by then also.

Furthermore, the data released now only partially captures the inflation impetus from the conflict and without action from the BoJ the level of real yields is likely to decline over the coming months as the inflation impact broadens. With the MoF intervening, but without notable success, and JGB yields close to record or cyclical highs, the pressure on the BoJ to act to anchor inflation expectations will be high. Next week the Summary of Opinions from the April BoJ meeting will be released (12th) and there’ll be a speech from policy board member Kazuyuki Masu (14th). Deputy Governor Himino will speak next weekend (16th) and if by then we have had progress in reaching a negotiated deal between the US and Iran we would see Himino as the key person to potentially signal a greater prospect of a rate hike. A combination of Middle East de-escalation and a more hawkish BoJ is the most plausible route to the MoF’s recent intervention having any sustained follow-through.

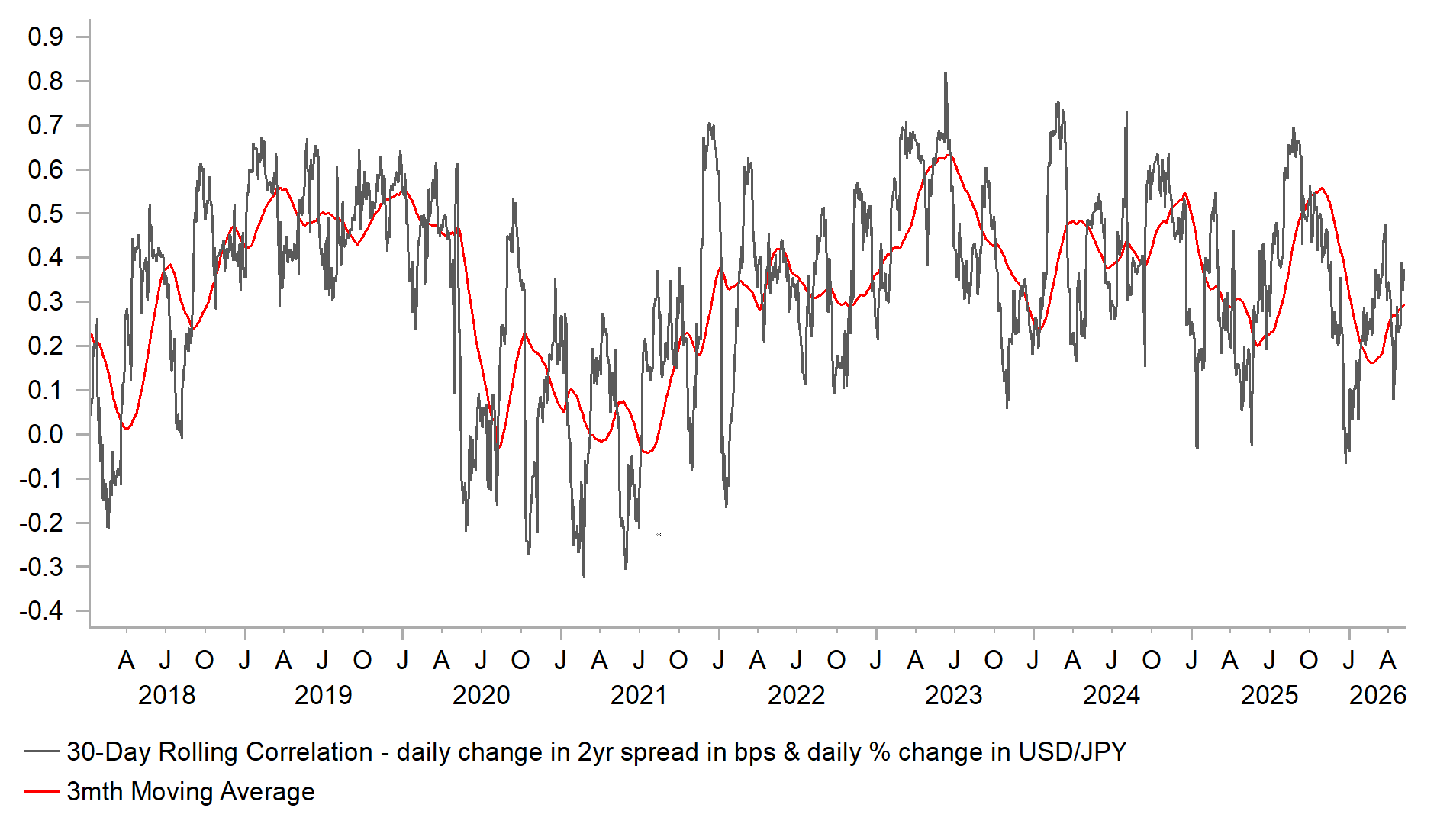

USD/JPY US-JP RATE SPREAD CORRELATION WEAKEST SINCE COVID

Source: Bloomberg, Macrobond & MUFG GMR

USD: Jobs data in focus – will FOMC divisions grow?

The world awaits a response from Iran on whether it will accept the MoU proposed by the US for pushing forward with a peace deal by taking steps to reopen the Strait of Hormuz. The prospect of a reopening and seen crude oil prices decline notably this week and further declines will be required to ease inflation risks that are building by the day. The US dollar remains close to post-conflict lows and close to fully retracing the dollar gains since the conflict began.

If there’s a data release that can avert attention away from the Middle East uncertainties it is the monthly payrolls report, released this afternoon. The consensus is for a 65k gain in payrolls after a solid gain of 178k last month. But that followed a 129k drop with distortions creating added volatility. The 6-month average to March was 53k, broadly similar to the consensus for today’s gain for April. The 12-month average is currently 42k and the unemployment rate has drifted higher by 0.4ppt over that period and suggests that the current pace of NFP gain is not enough to keep the unemployment rate stable. If the labour market is loosening we would argue that the FOMC will continue to lean more toward scope to ease the monetary policy stance going forward. That loosening is evident in the wage growth data as well with the annual average hourly wage growth rate slowing from 4.1% to 3.5% over the last year – the 3.5% growth rate in March was the weakest since the covid-related plunge.

A consensus reading today would certainly provide justification for FOMC members to argue that monetary policy can be eased if a peace deal is achieved and crude oil prices can decline further. The FOMC does look more divided currently with three dissenters to the meeting statement text implying the next move would be an “additional adjustment” but the partial driver of division (the uncertainty over energy prices) would at least diminish if a peace deal is achieved. A consensus and/or a weaker reading today in the context of further falls in crude oil on a resolution to the conflict (over the coming days) will likely open up expectations of a divergence in monetary policy between the ECB/BoE and the Fed. Under a dual-mandate policy framework weak labour market conditions would likely take precedence in circumstances of falling energy prices even assuming some degree of higher risk premium would keep oil prices higher than before the conflict. But for the ECB and potentially the BoE, the added geopolitical risk premium in oil prices would likely mean tighter monetary policy.

It is certainly feasible in a scenario of a peace deal and a further USD 10-15pbl drop in crude oil prices that the ECB/BoE could tighten monetary policy sooner rather than later while the Fed possibly eases policy toward year-end. Hikes in Europe versus cuts in the US is unusual though not unprecedented (2011 ECB hiked twice during Fed QE) but would certainly fuel renewed upside momentum for EUR/USD. Relative macro and yield spreads as a driver of FX has weakened due to the US-Iran conflict but if resolved that dynamic would likely strengthen once again.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 08:00 | ECB President Lagarde Speaks | - | - | - | !!! |

EU | 08:05 | ECB's De Guindos Speaks | - | - | - | ! |

US | 10:45 | Fed's Governor Cook Speaks | - | - | - | !!! |

US | 12:30 | Fed's Bowman Speaks | - | - | - | !!! |

GB | 13:20 | BoE Gov Bailey Speaks | - | - | - | !!!! |

US | 13:30 | Nonfarm Payrolls | (Apr) | 65K | 178K | !!!!! |

US | 13:30 | Unemployment Rate | (Apr) | 4.3% | 4.3% | !!!! |

US | 13:30 | Average Hourly Earnings (MoM) | (Apr) | 0.3% | 0.2% | !!!! |

US | 13:30 | Average Hourly Earnings (YoY) (YoY) | (Apr) | 3.8% | 3.5% | !! |

CA | 13:30 | Unemployment Rate | (Apr) | 6.7% | 6.7% | !! |

CA | 13:30 | Employment Change | (Apr) | 12.9K | 14.1K | !!! |

CA | 13:30 | Avg hourly wages Permanent employee | (Apr) | - | 5.1% | ! |

US | 15:00 | Michigan Consumer Sentiment | (May) | 49.7 | 49.8 | !! |

US | 15:00 | Michigan 1-Year Inflation Expectations | (May) | - | 4.7% | !! |

US | 15:00 | Michigan 5-Year Inflation Expectations | (May) | - | 3.5% | !! |

US | 15:00 | Wholesale Inventories (MoM) | (Mar) | 1.4% | 0.8% | ! |

EU | 17:00 | ECB's Schnabel Speaks | - | - | - | !!! |

Source: Bloomberg & Investing.com