USD regains upward momentum on back of higher oil price & US yields

USD: Fed rate hike expectations & military strikes reinforce upward momentum

The US dollar has continued to trade at stronger levels overnight after rising sharply at the end of last week. It has resulted in the dollar index moving back above the 100.00-level for the first time since the start of April. The main trigger behind the US dollar’s renewed upward momentum was further evidence that the US labour market has strengthened at the start of this year. Stronger employment growth alongside upside risks to the inflation outlook from the energy price shock in the Middle East has encouraged market participants to price in multiple rate hikes from the Fed in the year ahead. There are now almost 50bps of Fed rate hikes priced in by April and June of next year with the first hike expected by the autumn. The hawkish repricing of Fed rate hike expectations has lifted the 2-year US Treasury yield up to the highest level since February of last year. Higher US yields and the stronger US dollar were encouraged by the latest nonfarm payrolls report that revealed the US economy added 172k jobs in May on top of upward revisions to prior months of 93k. Employment growth has been robust over the last three months averaging 188k/month marking a significant improvement from average monthly job losses of -4k in the prior three months. At the very least, the report should give Fed officials even more confidence that downside risks for the labour market continue to ease. A favourable development that increases the likelihood that the Fed will drop their easing bias at the next FOMC meeting in June after three participants dissented against keeping it at the last meeting in April. If employment growth continues to remain as strong going forward it could also begin to add to upside inflation risks alongside higher energy prices which is already fuelling Fed rate hike expectations. However, the stable unemployment rate at 4.3% and slowing hourly earnings growth at 3.4%Y/Y should help to dampen pressure on the Fed to raise rates in response to concerns over inflation risks related to labour market tightening. We continue to believe that the Fed will leave rates on hold this year by looking through the energy price shock but acknowledge that the risks of Fed policy action are increasing.

At the same time, the US dollar’s upward momentum has been reinforced at the start of this week by renewed military tensions between Israel and Iran. Israel and Iran both exchanged missile strikes despite President Trump calling on both sides to halt fighting and give peace talks a chance to succeed. Iran launched a fresh wave of attacks just hours after firing ballistic missiles at Israel on Sunday. Israel responded with strikes on military targets in western and central Iran, while Iranian state media reported multiple explosions in Tehran according to Bloomberg. The latest strikes follow an escalation between Israel and Hezbollah. Lebanese militia attacked targets in northern Israel prompting a strike by the Israeli military in Beirut’s southern suburbs. Hezbollah and Israel had just agreed last week to a partial ceasefire. The latest military strikes have put a dampener on market expectations for an imminent peace deal to end the Middle East conflict and reopen the Strait of Hormuz. In response the price of Brent crude oil has jumped higher by almost 5%. President Trump had claimed in an interview with Fox News over the weekend that deal could have been signed early this week prior to the latest military strikes.

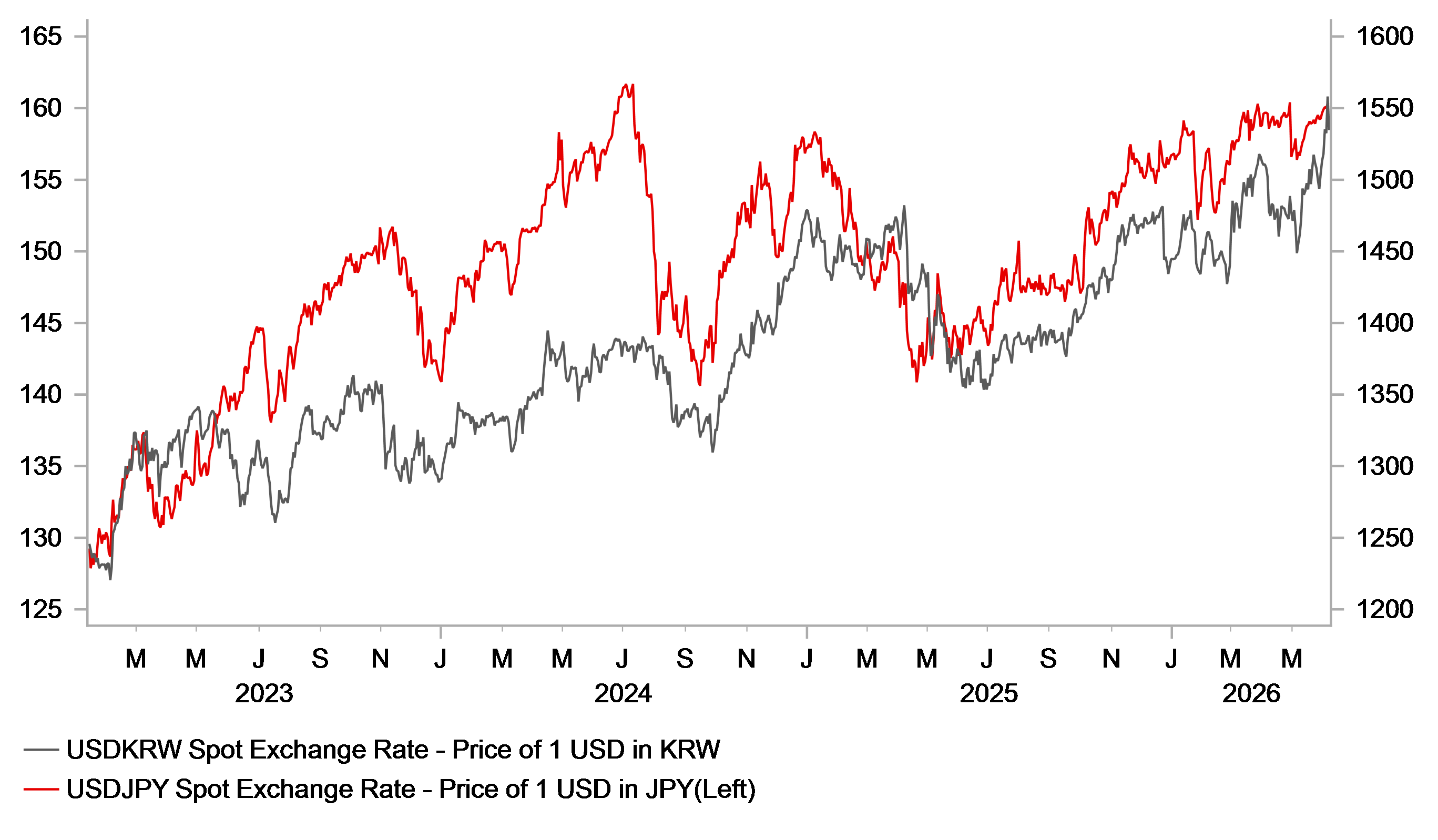

PERFORMANCE OF JPY & KRW HAVE BEEN TIGHTLY CORRELATED

Source: Bloomberg, Macrobond & MUFG Research

USD/Asia: AI tech sell-off & emergency policy support in Korea

The adjustment higher in US rates has also coincided with a sharp correction lower for AI tech stocks. The Nasdaq composite index closed down by just over 4.0% on Friday giving back almost a quarter of its outsized gains since the recent low point recorded in late March. The sell-off in AI tech stocks has continued overnight during the Asian trading session. South Korea’s Kospi index fell by more than 8% triggering a 20-minute trading halt by the stock exchange shortly after the market open. The Kospi index has since stabilized after reopening. The Kospi has given back over a third of its gains recorded since the recent low point at the end of March.

The sharp correction lower for South Korea’s equity market which is dominated by the AI tech stocks of Samsung Electronics and SK Hynic Inc, could add to selling pressure for the Korean won. Foreign investors have already been heavy sellers of Korean equities so far this year. USD/KRW hit a fresh high of 1,562.3 on Friday after the stronger NFP report but has since dropped by around -1.5% overnight in response to emergency measures announced by domestic policymakers to provide more support for the won. South Korea announced a response plan including tighter oversight of offshore currency derivatives, inspections targeting suspected market misconduct, and probes into potentially illegal foreign exchange transactions after an emergency meeting with the heads of the Bank of Korea and financial regulators. The latest measures build on earlier steps including allowing the National Pension Service to expand FX hedging and easing rules to improve dollar liquidity. The won has traded very closely in line with the yen so far this year. Like in Korea, Japanese policymakers remain under pressure to provide more support for the yen. USD/JPY has drifted back above the 160.00-level at the start of this week as it moves back within touching distance of the year-to-date high of 160.72 from 30th April.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 09:30 | Sentix Investor Confidence | (Jun) | -13.8 | -16.4 | ! |

CA | 11:00 | Leading Index (MoM) | (May) | - | 0.06% | ! |

US | 15:00 | CB Employment Trends Index | (May) | - | 105.77 | ! |

US | 16:00 | Consumer Inflation Expectations | (May) | - | 3.6% | ! |

Source: Bloomberg & Investing.com