US-Iran deal optimism weighs on USD performance

USD: Building investor optimism over US-Iran deal driving FX market

The US dollar has continued to trade at weaker levels overnight reflecting building investor optimism over a potential deal between the US and Iran to end the conflict and re-open the Strait of Hormuz. The ongoing improvement in global investor risk sentiment has contributed to the high beta G10 commodity currencies of the Australian and New Zealand dollars outperforming. There has been a bullish break out for AUD/USD which finally risen decisively above the 0.7200-level and opened the door to further near-term gains for the Aussie. The boost to investor confidence was initially triggered by an Axios report stating that the White House believes it is getting close to an agreement on a one-page memorandum of understanding to end the war and set a framework for more detailed nuclear negotiations. The US expects Iranian responses on several key points within the next 48 hours. The report added it was the closest the two parties had been to an agreement since the war began. The details of the potential agreement are probably as good as one could hope for in the near-term. In its current form the MOU would declare an end to the war and start a 30-day period of negotiations to re-open the Strait, limit Iran’s nuclear program and lift US sanctions on Iran. The US naval blockade and Iran’s restrictions on shipping through the Strait would be gradually lifted during that 30-day period. The report also noted that the duration of the moratorium on uranium enrichment is being actively negotiated with a compromise required between Iran’s proposal for a 5-year moratorium and the US demand for 20 years. It was suggested that Iran could even agree to remove highly enriched uranium from the country.

It has since been reported elsewhere that Iran is expected to send a response via Pakistan in the next two days, although the state media in Iran have signalled that parts of the US proposal remain unrealistic to Iran’s leadership. President Trump acknowledged to the New York Post that it might be “too soon” to think about face-to-face talks dampening hopes a deal is imminent before he is scheduled to meet President Xi of China next week. It has been reported that China’s Foreign Minister Wang Yi has urged Iran to keep negotiating with the US at a meeting with Iranian Foreign Minister Abbas Araghchi in Beijing. Overall, the latest developments add to investor confidence that the US and Iran continue to make progress to find a diplomatic solution to end the conflict and re-open the Strait. However, it remains unclear how long it will take for the Start to re-open. The price of Brent has fallen sharply back towards USD100/barrel in anticipation that the Strait could start to re-open soon. The improvement in global investor risk sentiment and drop in energy prices is providing a tailwind for emering market currency performance.

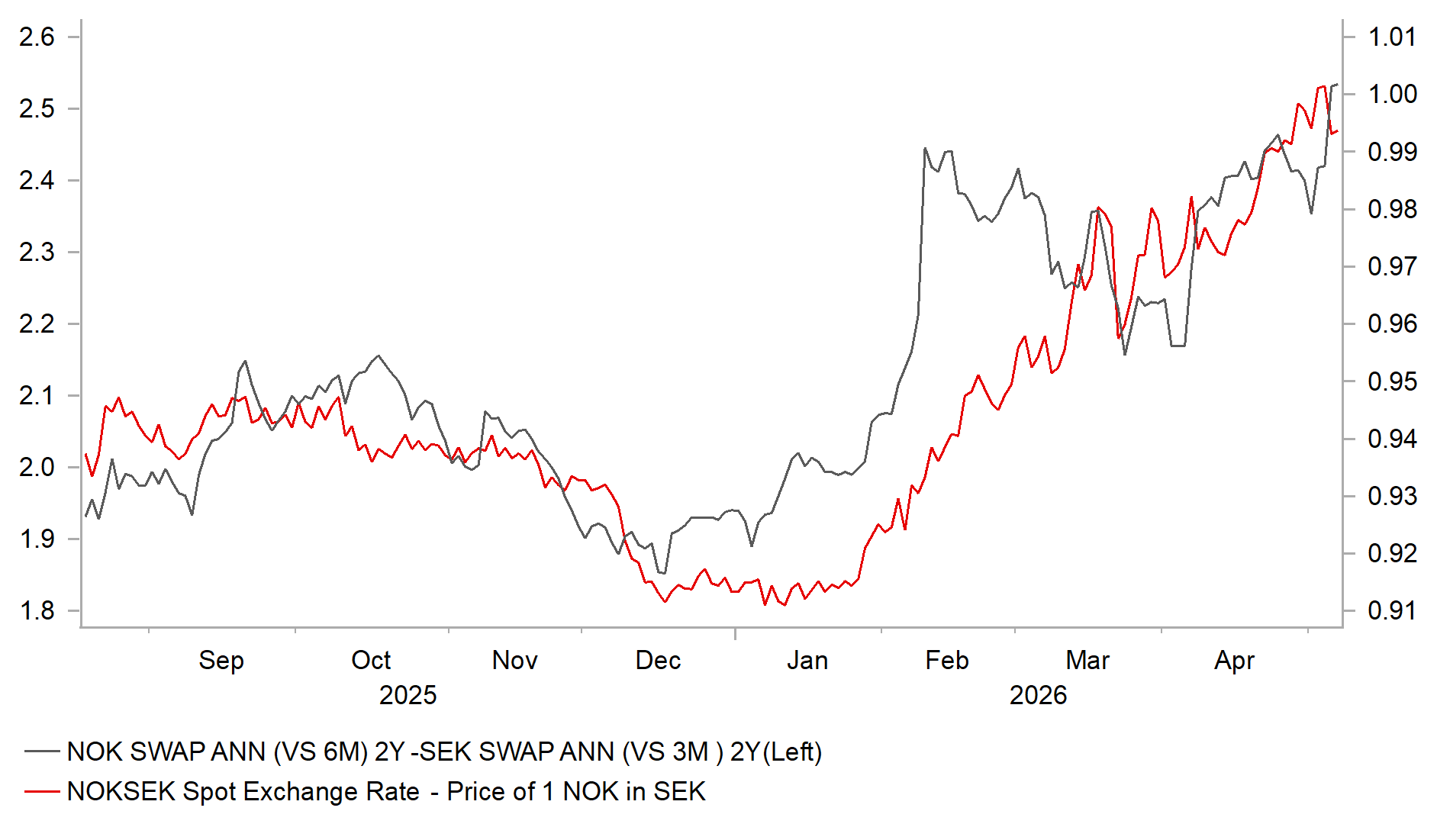

NORGES BANK & RIKSBANK POLICY DIVERGENCE HELPS LIFT NOK/SEK

Source: Bloomberg, Macrobond & MUFG GMR

NOK/SEK: Norges Bank in more of a rush to tighten than Riksbank

The sharp sell-off for the price of oil has triggered a correction lower for the Norwegian krone ahead of today’s Noges Bank policy meeting. Even after yesterday’s correction lower, the Norwegian krone is still the best performing G10 currency since the Middle East conflict started in late February. In contrast, the other Scandi currency of the Swedish krona has been the worst performing G10 currency over the same period. If the Middle East conflict continues to de-escalate and the Strait of Hormuz re-opens, we would expect yesterday’s reversal lower for NOK/SEK to extend further. The pair had already risen by almost 10% year to date prior to yesterday’s sell-off.

The Norwegian krone has benefitted in recent months both from higher energy prices and the hawkish repricing of Norges Bank policy expectations. At the last policy meeting in March, the Norges Bank provided a hawkish policy update by signalling that they planned to raise rates at one of the forthcoming policy meetings. It opened the door for a hike as soon as at today’s policy meeting. Market participants and Norwegian economists are unsure though whether they will wait a little longer until the following meeting in June. The Norwegian krone could strengthen further if a hike is delivered today as it is far from fully priced in. However, we would still expect the Norges to stick to plans to deliver one to two rate hikes by the end of this year.

In contrast, the Riksbank in Sweden appear to have more room to leave rates on hold in the near-term. The Riksbank’s ability to look through the energy price shock was boosted by the release yesterday of another weak inflation report from Sweden. The latest reading for the annual rate of core inflation (CPIF excluding energy) fell to just 0.0% in April while the headline rate moved into negative territory at -0.1%. At the last meeting in March, the Riksbank indicated that the policy rate is expected to remain at the current level for some tie to come while acknowledging that the war in the Middle East makes forecasting very uncertain. Market participants will be watching closely today to see if the Riksbank signals that it is considering raising rates in response to the energy price shock. The softer inflation readings should dampen the need for imminent rate hikes. We expect the near-term policy divergence between the Norges Bank and Riksbank to continue to provide support for NOK/SEK.

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 09:00 | ECB's Lane Speaks | - | - | - | !! |

NO | 09:00 | Interest Rate Decision | - | 4.00% | 4.00% | !! |

GB | 09:30 | Construction PMI | (Apr) | 45.8 | 45.6 | !!! |

EU | 10:00 | Retail Sales (MoM) | (Mar) | -0.3% | -0.2% | ! |

US | 12:30 | Challenger Job Cuts | (Apr) | - | 60.620K | ! |

US | 13:30 | Initial Jobless Claims | - | 205K | 189K | !!! |

US | 13:30 | Nonfarm Productivity (QoQ) | (Q1) | 0.7% | 1.8% | !! |

US | 13:30 | Unit Labor Costs (QoQ) | (Q1) | 2.6% | 4.4% | !! |

EU | 13:40 | ECB's Lane Speaks | - | - | - | !! |

US | 15:00 | Construction Spending (MoM) | (Mar) | 0.3% | -0.3% | !! |

EU | 18:00 | ECB's Schnabel Speaks | - | - | - | !! |

US | 20:30 | FOMC Member Williams Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com