Jobs data in focus as year-to-date low holds

USD: NFP expected to remain resilient

The UST bond yield hitting 4.88% this week, the highest since 2007, underlines the current pricing in the market for a continuation of resilient economic data that is required to allow the Federal Reserve to persist with the communication of “higher for longer”. The correction lower from that 4.88% high was triggered by the weak ADP data (+89k vs 150k expected) shows the importance of labour market data in keeping the US economy on a firm footing. It also highlights the increasing importance of incoming economic data in keeping yields and the dollar stronger going forward.

It certainly underlines our view that we may well be in the last leg of this move higher in yields and the dollar. The labour market has generally been a consistent positive although there have been signs of softening demand building. That was put into some doubt this week after the JOLTS data revealed a rebound in job openings from 8.9mn to 9.6mn. The initial claims data yesterday also remained at recent lows suggesting limited fresh firing from jobs.

But when recession comes it tends to show up quite suddenly in the labour market data. For sure, initial claims in the low 200k’s does not suggest recession is imminent. But the GFC recession began in December 2007 and the initial claims data remained in a range mostly between 300-350k throughout most of 2006 and into 2007 and only started to clearly trend higher in October 2007, just two months before the recession began. NFP had weakened through 2007 but November and December NFP readings were north of 100k before suddenly diving at the start of 2008.

If today’s NFP data was to reveal an acceleration in payrolls it would certainly push further back the expectations on the timing of a downturn, reinforce the “higher for longer” mantra and fuel renewed UST bond selling and dollar buying. It’s difficult to forecast NFP month-to-month and ADP has not been a great predictor and while the trend of weakening demand is clear, it does not mean that will be reflected today.

The only observation to note going into the NFP print is evidence of possible exhaustion in the rates/FX move. The fed funds futures curve has seen some modest increase in rate cut expectations for next year from 60bps to about 75bps which may be a sign that we have reached the limits for now and hence the NFP hurdle for triggering higher rates and a stronger dollar is a little higher. In other words an in-line print this afternoon may be greeted with some relief that extends the correction in yields a little further lower from here which would allow the dollar to adjust a little further weaker too. The Fed’s Summary of Economic Projections in September revealed expectations of the labour market being stronger (unemployment rate revised down from 4.1% to 3.8% for Q4 2023 - the current level) which means any disappointment in the data like another jump in the unemployment rate has the potential to influence rate expectations that bit more.

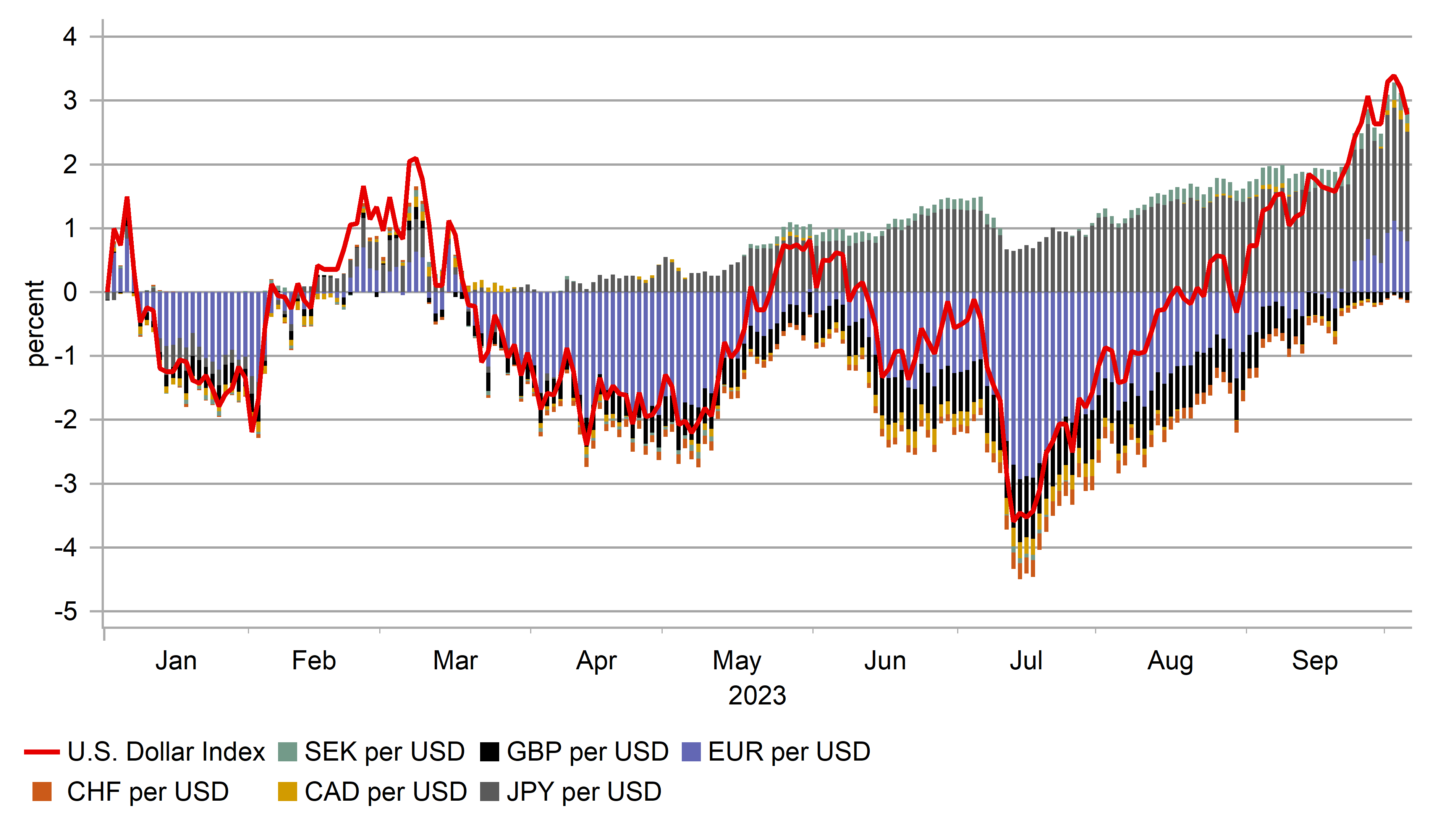

JPY THE DOMINANT SOURCE OF DXY STRENGTH THIS YEAR

Source: Bloomberg, Macrobond & MUFG GMR

JPY: The MoF changes tune

The rhetoric from Japan on foreign exchange has taken a different direction with comments from Finance Minister Suzuki today suggesting that the threshold for intervening to halt yen depreciation may be lower than previously assumed. Today, Suzuki stated that various factors are looked at to determine “excessive moves” and that “gradual one-directional moves” could be viewed as excessive by the authorities. This clearly could place the current moves in USD/JPY in scope for “excessive moves” given since the BoJ meeting at the end of July when the YCC framework was altered,USD/JPY has gained 10 big figures It’s been mostly one-directional and in any case, the removal of “disorderly price action” as the justification of intervention means in reality intervention could now take place at any point in time.

Key economic data released today will also keep the MoF focused on trying to halt the slide of the yen with the cash earnings data coming in weaker than expected. The annual increase in cash earnings was unchanged at 1.1% in August, weaker than the 1.5% expected. The underlying data also disappointed. One of the key measures monitored by the BoJ that we track – contractual pay for full-time employees (so exbonus and ex-overtime) – slowed from 2.0% to 1.5%, the weakest reading since April.

Given that wages will be such a key determinant in assessing whether price stability has been achieved, this data certainly lowers the probability of any near-term surprise removal of NIRP or another change in YCC. It seems therefore more likely that we will see USD/JPY grind higher and retest that level just above the 150-level that prompted a sharp reversal. That of course could come as soon as this afternoon if the US jobs report was to prove stronger than expected. As stated here before, we’d still expect a clearer break higher well through 150.00 before the MoF would intervene.

UNDERLYING WAGE GROWTH SLOWED IN AUGUST

Source: Macrobond & Bloomberg

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensu s |

Previous |

Mkt Moving |

|

IT |

09:00 |

Italian Retail Sales (YoY) |

Aug |

-- |

2.7% |

! |

|

IT |

09:00 |

Italian Retail Sales (MoM) |

Aug |

0.0% |

0.4% |

! |

|

US |

13:30 |

Average Hourly Earnings (MoM) |

Sep |

0.3% |

0.2% |

!!!! |

|

US |

13:30 |

Average Hourly Earnings (YoY) (YoY) |

Sep |

4.3% |

4.3% |

!! |

|

US |

13:30 |

Average Weekly Hours |

Sep |

34.4 |

34.4 |

! |

|

US |

13:30 |

Nonfarm Payrolls |

Sep |

170K |

187K |

!!!!! |

|

US |

13:30 |

Participation Rate |

Sep |

-- |

62.8% |

!! |

|

US |

13:30 |

Private Nonfarm Payrolls |

Sep |

160K |

179K |

!!! |

|

US |

13:30 |

U6 Unemployment Rate |

Sep |

-- |

7.1% |

!! |

|

US |

13:30 |

Unemployment Rate |

Sep |

3.7% |

3.8% |

!!!! |

|

CA |

13:30 |

Avg hourly wages Permanent employee |

Sep |

-- |

5.2% |

! |

|

CA |

13:30 |

Employment Change |

Sep |

20.0K |

39.9K |

!!! |

|

CA |

13:30 |

Participation Rate |

Sep |

-- |

65.5% |

! |

|

CA |

13:30 |

Unemployment Rate |

Sep |

5.6% |

5.5% |

!!! |

|

US |

15:00 |

Total Vehicle Sales |

-- |

-- |

15.00M |

! |

|

US |

17:00 |

Fed Waller Speaks |

-- |

-- |

-- |

!! |

|

US |

20:00 |

Consumer Credit |

Aug |

11.70B |

10.40B |

! |

Source: Bloomberg