USD derives support as Middle East tensions pick-up

USD: Middle East tensions pick-up while Fed leadership remains dovish

The US dollar has traded at stronger levels overnight reflecting more investor unease over the Middle East conflict. It follows renewed tensions yesterday between the US and Iran which have lifted the price of Brent up to a high overnight of USD114.07/barrel. It follows reports that the US military fought off attacks from Iranian drones, missiles and armed small boats as it facilitated the passage of two US-flagged vessels through the Strait of Hormuz according to US Central Command chief Admiral Brad Cooper. CBS reported that US destroyers USS Truxton and USS Mason transited the strait supported by Apache helicopters and other aircraft. President Trump posted that “we’ve shot down seven small boats. At the same time, it has been reported that the UAE intercepted Iranian cruise missiles and blamed an Iranian drone strike for a large fire at its Fujairah port. An oil tanker owned by the UAE’s state oil company Abu Dhabi National Oil Company was also reportedly struck by Iranian drones outside the Strait of Hormuz. It is the first major test of the ceasefire that has already held since going into effect on 8th April. The renewed pick-up in military tensions have started since President Trump announced Operation Project Freedom to escort merchant vessels and ensure the freedom of navigation of the Strait of Hormuz. Iran has clearly stated that anu US interference under Project Freedom would be treated as a breach of the ceasefire, and insisted that navigation through the Strait must be coordinated with itself. The renewed tensions have added to concerns that the Middle East conflict will prove more prolonged and it will take longer to full re-open the Strait. Market participants are not optimistic that the US will be able to fully re-open the Strait on its own, and the retaliatory strikes from Iran could increase the risk of more disruption to energy production facilities in the region. The negative developments have put a dampener on investor risk sentiment at the start of this week helping to support the US dollar.

Upside from US rates and the US dollar from higher energy prices was partially offset yesterday by some dovish comments from New York Fed President Williams who stated that he remains open to the idea of lowering rates further although the timing of the next rate cut has been delayed. He stated “we will at some point need to be lowering interest rates to reflect the fact that inflation is lower. However, with “inflation higher this year than previously expected, so that pushes off a date of lowering rates, in my view, but it doesn’t change that basic story”. He also added that he was “very comfortable” with the current language in the statement because he doesn’t “see anything in the day-to-day” suggesting there’s an argument for a rate hike in the near-term. It follows the decision by three regional Fed presidents to dissent at the last FOMC meeting over the decision to maintain an explicit easing bias in the statement. He highlighted that unlike the supply disruption following the COVID shock, the labour market is not adding to inflation pressures this time around. He is reassured that underlying inflation outside of imported goods and energy have so far remained stable, and still sees no significant second-round effects from tariff hikes. The relatively dovish leadership of the Fed continues to encourage expectations that it will look through the energy price shock while European central banks are more likely to tighten policy creating a headwind for US dollar performance.

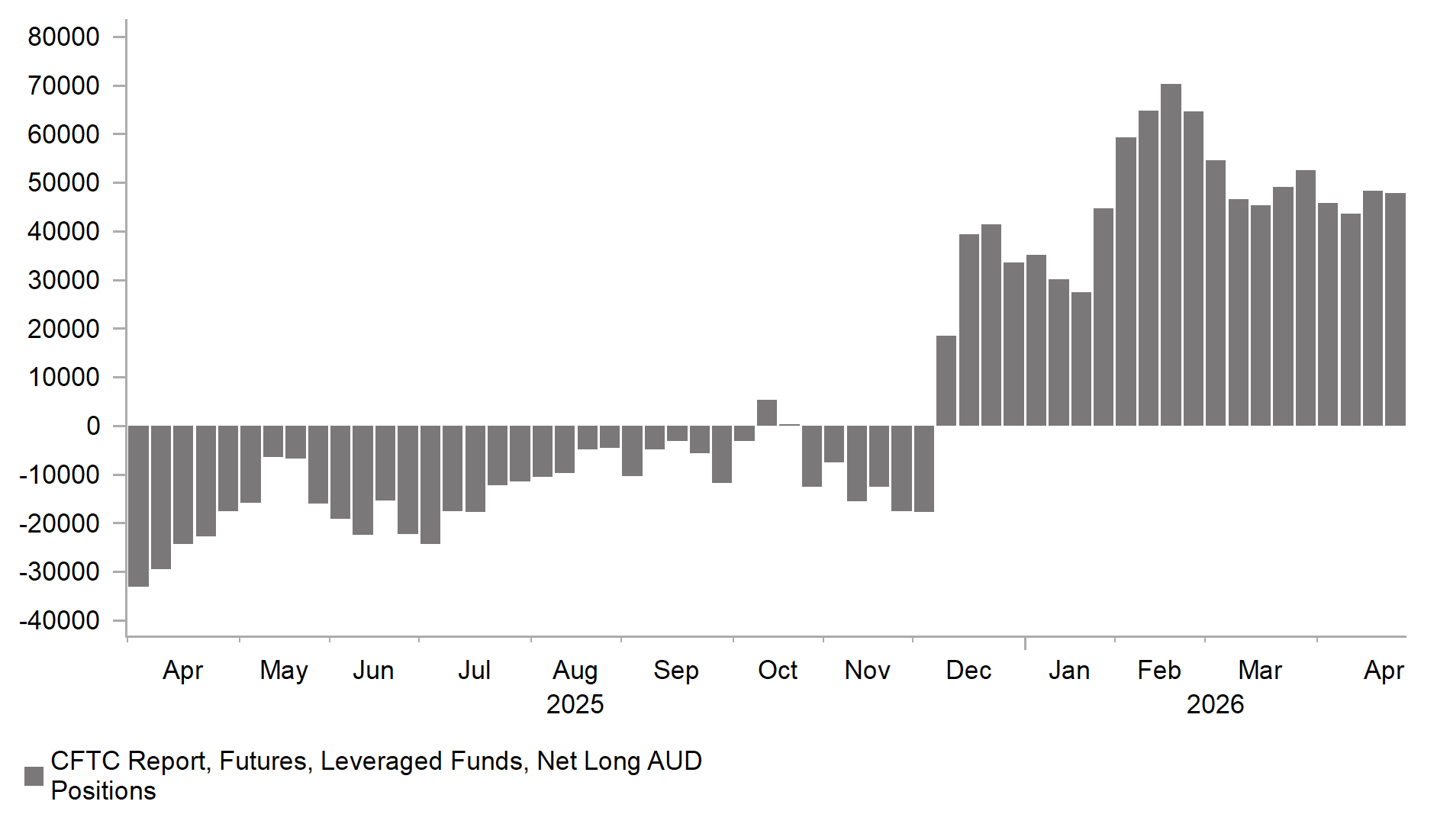

LONG AUD POSITIONS HAVE BEEN POPULAR

Source: Bloomberg, Macrobond & MUFG GMR

AUD: RBA delivers third hike but unlikely to hike again as soon as June

The development overnight was the RBA’s latest policy meeting. The RBA decided to raise their policy rate by 25bps for the third consecutive meeting although it was not a unanimous decision (8-1 in favour). The updated statement indicated that the RBA was concerned that inflation is likely to remain above target for some time and judged that risks remain titled to the upside. Having raised the policy rate three times, monetary policy is “well placed” to respond, and they “will do what’s necessary” to deliver price stability. The Middle east conflict has added to upside risks for inflation. The RBA noted that higher fuel prices are adding to inflation and there are indications that this is likely to have second-round effects on prices of goods and services more broadly. The RBA voiced concern that a longer or mor severe conflict could put further upward pressure on global energy prices, pushing up near-term inflation and increasing inflation further out as these costs are passed through and get built into longer-term inflation expectations. The RBA’s updated inflation forecasts were raised to show a peak of 4.8% in June and then easing to 4.0% by year end. The trimmed-mean core forecast is now expected to remain above 3.0% until 2H of next year.

In the accompanying press conference, Governor Bullock stated that the oil shock has worsened the trade off between inflation and growth. After the recent rate hike, the RBA judges that the policy rate is “a bit restrictive” leaving room for further hikes if required. The current hike though “gives space to see how things unfold” and they are in a good space to watch how the war impacts inflation and jobs. The comments indicate that the RBA is not in a rush to hike at the fourth consecutive meeting in June but the door remains open for further tightening. We expect still expect the Australian dollar to perform strongly in the near-term unless there is a bigger correction lower for risk assets in response to the Middle East conflict.

KEY RELEASES AND EVENTS

|

Country |

BST |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

EC |

09:00 |

ECB's Panetta Speaks |

!! |

|||

|

US |

13:30 |

Trade Balance |

Mar |

-$61.0b |

-$57.3b |

!! |

|

CA |

13:30 |

Int'l Merchandise Trade |

Mar |

-2.50b |

-5.74b |

!! |

|

US |

14:45 |

S&P Global US Services PMI |

Apr F |

51.3 |

51.3 |

!! |

|

US |

15:00 |

Fed's Bowman Speaks |

!! |

|||

|

US |

15:00 |

ISM Services Index |

Apr |

53.7 |

54.0 |

!!! |

|

US |

15:00 |

JOLTS Job Openings |

Mar |

6850k |

6882k |

!!! |

|

EC |

16:40 |

ECB's Lane Speaks |

!!! |

Source: Bloomberg & Investing.com