US dollar risks skewed stronger ahead of key jobs data

USD: Will labour market data show continued stability?

The US dollar remains closer to the top end of the recent trading range after on Wednesday hitting the highest level (DXY basis) since the ceasefire deal was announced on 8th April. The financial markets appear to have become immune to the constant back-and-forth on whether a deal is imminent or breaking down but that can’t last long and there are surely growing risks that we could see a bigger lurch higher in crude oil prices if the Strait of Hormuz remains closed. President Trump continues to portray negotiations as productive and in the final stages while Iran states that no negotiations are taking place. With Hezbollah showing no appetite for a ceasefire in Lebanon, the prospects of a credible and lasting breakthrough look bleak. But hope continues to keep the financial markets in check and that is limiting the FX moves but risks are building of a more notable strengthening of the US dollar.

While we await whether there is any meaningful development in negotiations, the focus will shift to the key economic data point of the week – the nonfarm payrolls report. The data this week is part of the reason why the dollar is at the higher end of recent trading ranges with labour market data, in particular, not showing much evidence of deterioration. With rate spreads more influential once again in driving FX, EUR/USD is now more vulnerable to a stronger employment print given the OIS curve in Europe is now well priced or even overpriced for what the ECB will deliver. The 2-year UST bond yield is up 21bps since the beginning of May while the equivalent yield in Germany is just 2bps higher. The ECB now has three hikes close to fully priced over the next 12mths – a hike too many in our view with investors underestimating the negative implications in Europe from higher energy risks. For the Fed one hike is priced over the same period.

The Beige Book this week revealed a mixed consumer picture with conditions diverging – high income earners are driving consumption for higher-end products but middle- and low-income earners are struggling. But labour market conditions were described as stable while inflation pressures were broadening.

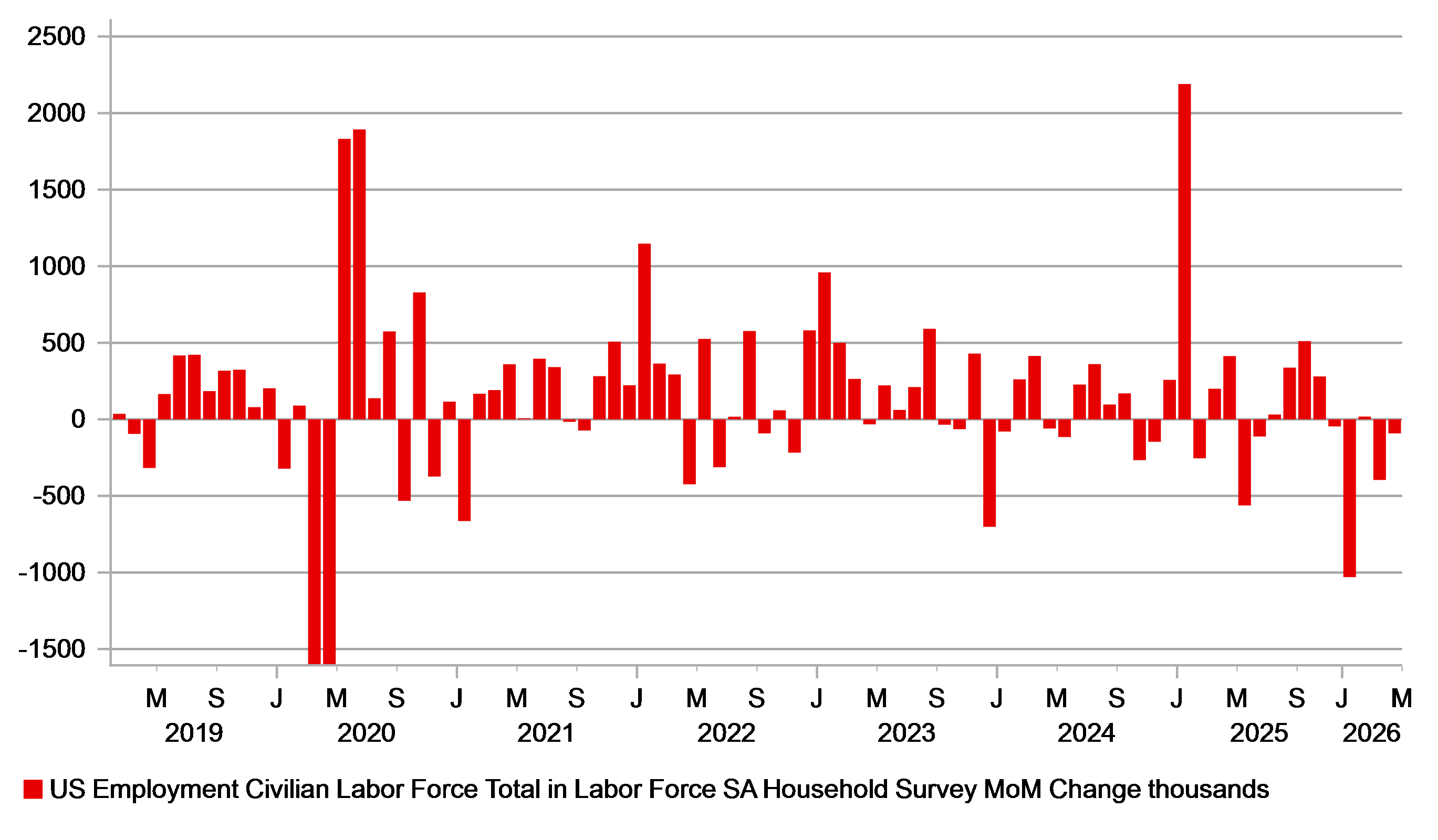

A consensus print today (+88k NFP; 4.3% unemployment rate) will be enough to keep the US dollar well supported and primed for an extension stronger if we do not get progress over the short-term in the Middle East. While the US consumer paints a weak picture outside of high-earners, labour market stability and increased inflation pressures will compel the Fed to highlight increased risks of monetary tightening – exactly what Dallas Fed President Logan did this week. But risks today are two-way and given consumer sentiment is weak and confidence in labour markets are mixed a weak print could see a lot of the tightening priced in the curve evaporate quickly. It is notable that the household survey shows a much weaker employment backdrop. However, given the seeming lack of progress in Middle East negotiations the appetite for US dollar selling on a weak report is probably less than appetite for buying on a stronger report.

HOUSEHOLD JOBS SURVEY – WEAKNESS EVIDENT IN RECENT MONTHS

Source: Bloomberg, Macrobond & MUFG Research

GBP: UK labour market continues to show signs of weakness

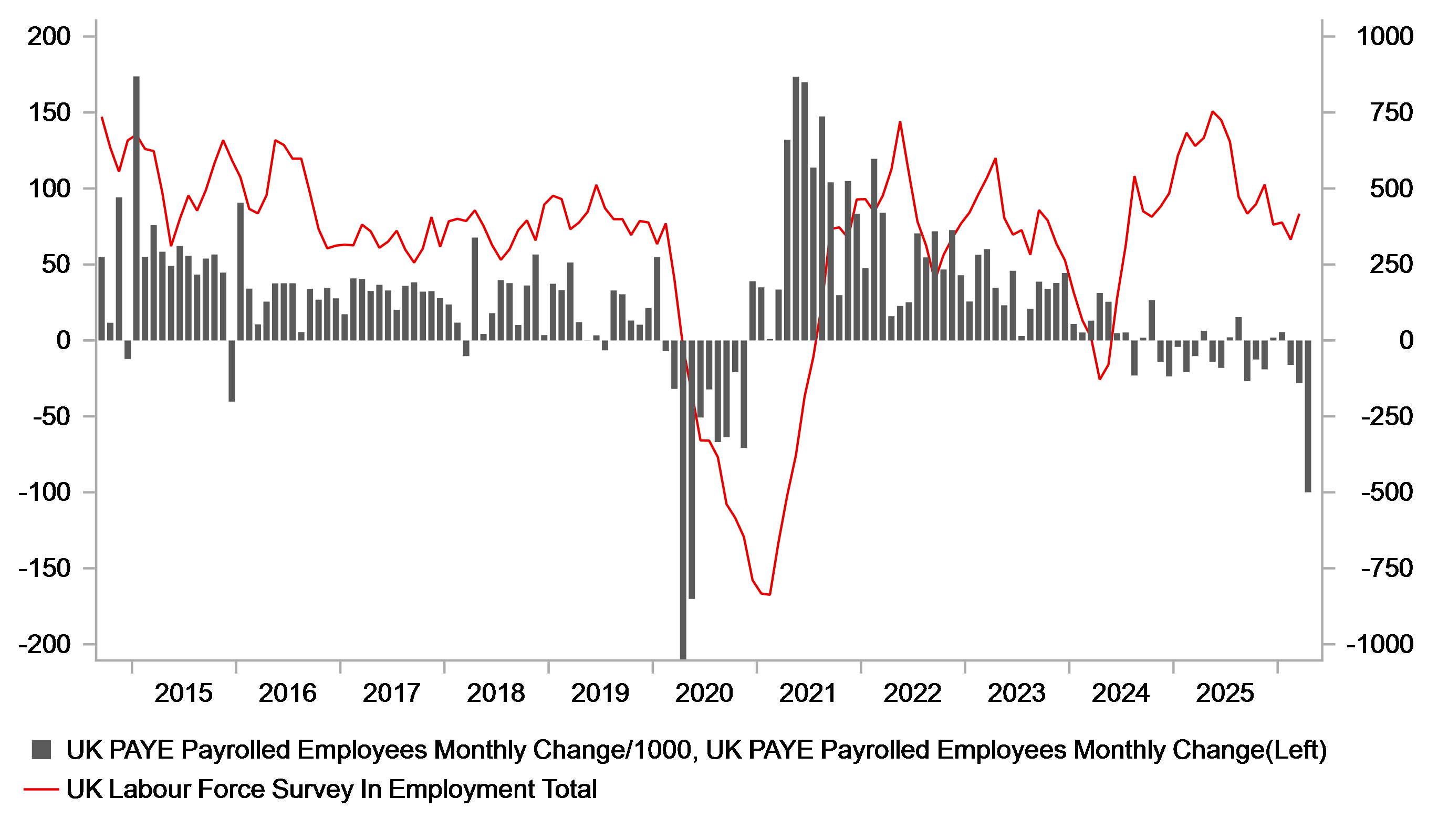

The focus today is very much on the US labour market, but we continue to see evidence that suggest the UK jobs market is weakening that could have implications for the BoE and how aggressively it may need to respond to the building inflation risks. Gilt yields in May declined more notably than elsewhere in part on the weaker than expected labour market and CPI data. The 100k drop in the HMRC monthly jobs data was by far the weakest print since the covid period although the financial market response was somewhat muted given the unreliability of the initial estimate that tends to get revised notably. BoE Governor Bailey also suggested that the MPC will take the data with a pinch of salt given the revision history, especially in the month of April.

However, the deterioration in labour market conditions in the HMRC data looks to have been backed up by data from the UK Insolvency Services that publishes data from HR1 forms that companies submit when 20 or more redundancies are planned at one company. In the four weeks to 24th May there were 37,000 potential layoffs reported, which was the largest since covid. It is a legal requirement for companies to fill out HR1 forms at least 30 days prior to between 20-99 employees potentially being made redundant. Because it is a legal requirement it could be deemed as reliable although those redundancies may not actually transpire. The data is released by the ONS weekly as “official statistics in development” and hence just like the HMRC data could be revised notably.

All that said, a look at the monthly data to April this year compared to the same period in 2025 indicates a roughly similar total of potential redundancies reported through the HR1 form and hence while it is worth monitoring given the latest four-week total, it does not necessarily signal an overall worsening yet to UK labour market conditions. We will likely have to wait for the data later this month on the labour market before FX and rates markets make any conclusions. Another month of weak data would likely place further questions on any imminent rate hike, especially if crude oil prices remain at these lower levels. We still suspect the BoE’s tolerance for looking through the energy price shock will diminish and help provide support for the pound versus the US dollar. One or two MPC members could well join Huw Pill in voting for a hike at the June meeting.

HMRC APRIL DROP OF 100K WAS BY FAR THE LARGEST SINCE 2020 – THE EXTENT OF REVISION WILL BE IMPORTANT FOR MPC & RATES/FX

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EC | 10:00 | GDP (QoQ) | (Q1) | 0.1% | 0.2% | !! |

EC | 10:00 | GDP (YoY) | (Q1) | 0.8% | 1.2% | !! |

EC | 10:00 | Employment Change (YoY) | (Q1) | 0.5% | 0.7% | ! |

EC | 10:00 | Employment Change (QoQ) | (Q1) | 0.1% | 0.2% | ! |

US | 13:30 | Nonfarm Payrolls | (May) | 85K | 115K | !!!! |

US | 13:30 | Unemployment Rate | (May) | 4.3% | 4.3% | !!!! |

US | 13:30 | Average Hourly Earnings (MoM) | (May) | 0.3% | 0.2% | !!!! |

US | 13:30 | Average Hourly Earnings (YoY) | (May) | 3.4% | 3.6% | !! |

US | 13:30 | Participation Rate | (May) | - | 61.8% | !! |

US | 13:30 | Average Weekly Hours | (May) | 34.3 | 34.3 | ! |

CA | 13:30 | Unemployment Rate | (May) | 6.9% | 6.9% | !!! |

CA | 13:30 | Employment Change | (May) | 10.1K | -17.7K | !!! |

CA | 13:30 | Avg hourly wages Permanent employee | (May) | - | 4.8% | ! |

CA | 13:30 | Participation Rate | (May) | 65.1% | 65.0% | ! |

UK | 14:40 | BoE MPC Member Dhingra Speaks | ! | |||

CA | 15:00 | Ivey PMI | (May) | 54.5 | 57.7 | !! |

UK | 19:00 | BoE Gov Bailey Speaks | !!! | |||

US | 20:00 | Consumer Credit | (Apr) | 17.80B | 24.86B | ! |

Source: Bloomberg & Investing.com