BoJ readies market as crude oil eases on renewed optimism

JPY: Modest move with a hike priced

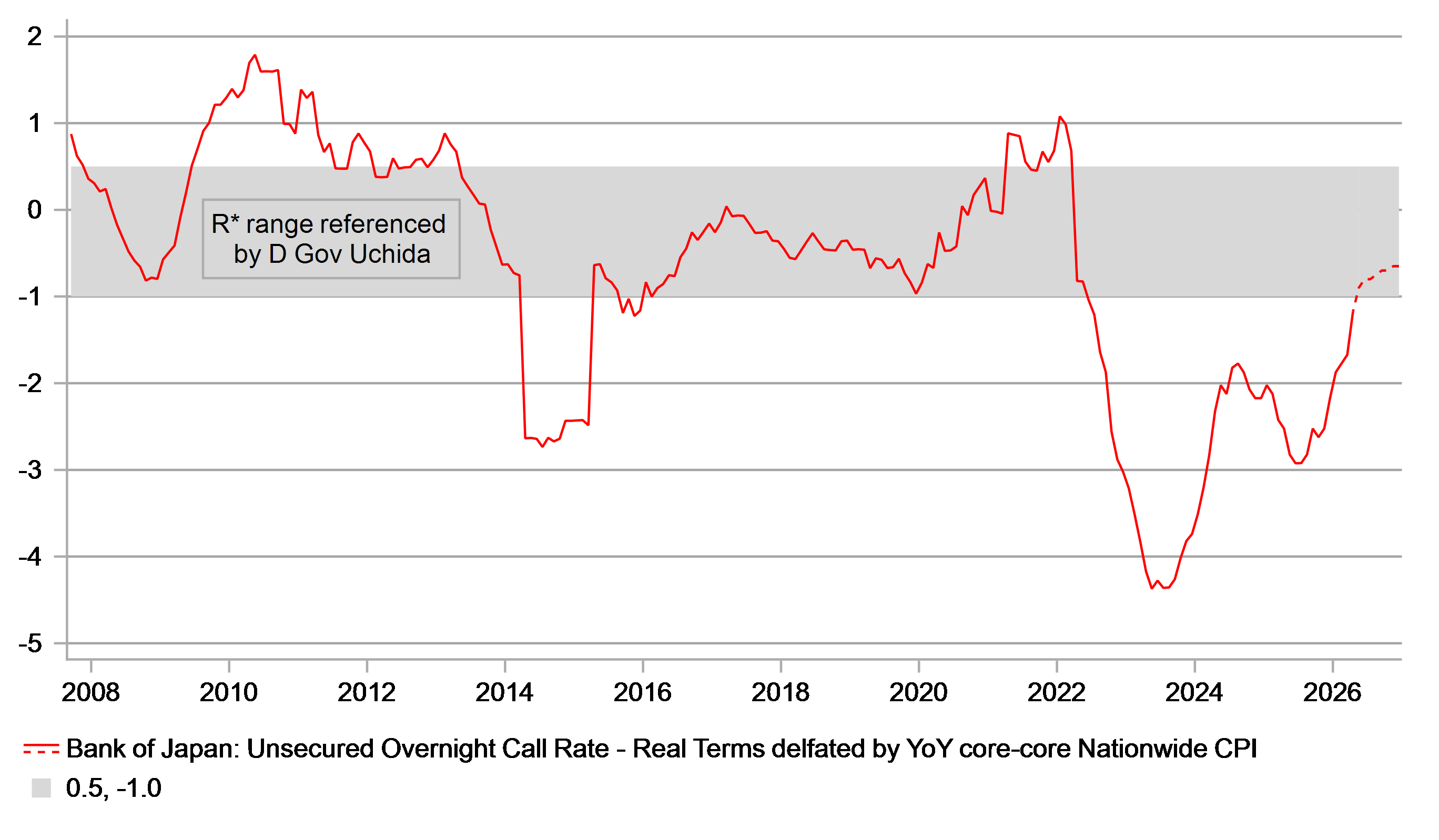

Bloomberg’s usual BoJ article about an upcoming policy meeting sourcing “people familiar with the matter” has been published and adds to the prospect of a rate hike by the BoJ at its meeting on 16th June. The speech by Governor Ueda did not provide a very explicit signal of a hike but there was enough in the speech to make clear that the intention is for the BoJ to hike this month. The message was that the BoJ is focusing more on upside inflation risks than downside growth risks. Ueda also emphasised the importance of credibility. Today’s Bloomberg article also suggested appetite from the BoJ to raise rates a second time later this year – our current view is for the BoJ to hike again in December. That implies that the forward guidance is unlikely to change and the BoJ will continue to signal further hikes. This makes sense given the assumed appropriate R* range (-1.0% to +0.5%) would only just be met based on a 2% CPI.

JGB yields are only modestly higher today and reflects the fact that two rate hikes are broadly priced by year-end and also the fact that crude oil prices are lower today on the back of the news of a ceasefire agreement between Israel and Lebanon. However, the drop in crude oil and market moves generally this morning are modest. We’ve been here before with ceasefire deals and whether Hezbollah is going to join such a deal remains questionable. Still, if this can hold over the coming days it increases the prospect of some progress between the US and Iran. President Trump yesterday stated that discussions are ongoing and that there could be a deal reached as soon as over the weekend.

But we have also heard that before and this back and forth on prospects of a deal or a breakdown is having less and less impact on market moves with the US dollar remaining more elevated – the dollar yesterday reached the highest level since 7th April just ahead of the ceasefire being agreed.

Part of the reason is the signs that FOMC members are starting to turn less tolerant to the idea of ‘looking through’ the energy price shock. That was always a risk and Dallas Fed President Lorie Logan stated yesterday that the labour market is “broadly balanced”, AI-related activity is booming and financial conditions are “accommodative”. That means the current policy rate is “not restraining the economy” and that a rate hike by year-end may be required. Regional Presidents are turning more hawkish and that is going to put further upward pressure on front-end yields. Status-quo in the Middle East will continue to put upward pressure on the US dollar and intervention risks will only help keep USD/JPY contained over the short-term.

BOJ POLICY STANCE COULD SOON ENTER RANGE OF R*

Source: Bloomberg, Macrobond & MUFG Research

USD: Labour market resilience & higher crude supports dollar

This week is one of those weeks in the month when the macro backdrop of the US economy takes on a little more importance given the economic data releases, mainly on the labour market culminating with tomorrow’s NFP report. The ADP report was released yesterday and along with the 2% advance in crude oil prices helped to lift UST bond yields further. The 2-year UST bond yield is up 20bps since the beginning of May, even though crude oil prices have dropped by around 14% over the same period. Front-end yields in Europe are up by a lot less or even down, in Germany up 2bps and in the UK down 7bps. But yields are rising everywhere again as Middle East optimism from recent weeks start to unravel on the lack of ceasefire deal.

US labour market data is also reinforcing the relatively higher move in the US. The ADP employment gain of 122k, broadly in line with the consensus that has reinforced expectations of a reasonably close to consensus (85k) print in tomorrow’s NFP release. The ISM Services report was clearly stronger than expected with new orders strong and prices paid jumping modestly further, remaining above the 70-level for the third consecutive month, for the first time since August 2022. The services economy doesn’t yet look impacted by higher energy prices. The Beige Book was released last night, and the key takeaways were that the labour market was stable, inflation pressures were intensifying but that there were signs of weakening consumer spending.

So, we would still certainly expect the negative impact of higher energy to come through, so we would be cautious reading too much into the stronger data this week as an indication of what’s to come. The Richmond Fed on Tuesday released a report analysing the impact on income from gasoline price rises (“How much more are drivers paying for gas”) and based on the AAA gasoline price of $4.56 per gallon on 21st May and using the Federal Highway Administration’s data on average annual mileage travelled (13,735 miles in 2024) and average fuel economy rates, the pre Middle East conflict versus the current cost of driving equates to an increase of $845, a not insignificant hit to real disposable income for the average US household.

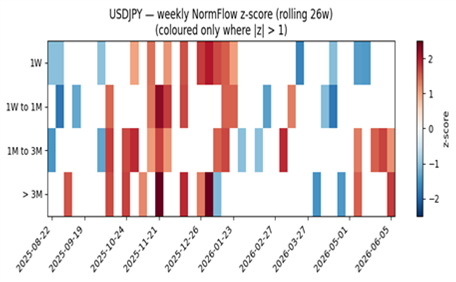

That’s an annual figure and hence if this gasoline price increase holds it will start to have a bigger impact in disposable income and spending. Jobs data today and tomorrow will be key ahead of Fed Chair Kevin Warsh’s first monetary policy meeting and press conference. How influential will Warsh be? And what will his initial leaning be regarding inflation risks? Whether tomorrow’s NFP is strong and whether the SoH has reopened by then will be important. If the escalation in clashes in the Middle East persist, the pricing of a rate hike this year will increase further and with the data holding up the positive momentum for the US dollar looks set to continue. The above chart indicates increased USD call option demand despite the threat of intervention.

LATEST BLOOMBERG OPTION FLOW DATA INDICATES GROWING USD/JPY BULLISHNESS WITH CALL DEMAND INCREASING FOR 1-3MTH AND BEYOND

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EC | 09:00 | ECB President Lagarde Speaks | - | - | - | !!! |

EC | 10:00 | Retail Sales (YoY) | (Apr) | - | 1.2% | ! |

EC | 10:00 | Retail Sales (MoM) | (Apr) | -0.3% | -0.1% | ! |

US | 10:30 | Challenger Job Cuts | (May) | - | 83.387K | ! |

US | 10:30 | Challenger Job Cuts (YoY) | - | - | -20.9% | ! |

US | 13:30 | Initial Jobless Claims | - | 211K | 215K | !!! |

US | 13:30 | Nonfarm Productivity (QoQ) | (Q1) | 0.8% | 0.8% | !! |

US | 13:30 | Unit Labor Costs (QoQ) | (Q1) | 2.3% | 2.3% | !! |

US | 13:30 | Continuing Jobless Claims | - | 1,780K | 1,786K | !! |

US | 13:30 | Fed's Barkin Speaks | - | - | - | !! |

UK | 16:40 | BoE Gov Bailey Speaks | - | - | - | !!! |

US | 18:10 | Fed's Daly Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com