USD/JPY back at 160 as conflict escalates

JPY: Ueda to signal a hike as broad support builds

The largest single month of intervention by the MoF/BoJ (JPY 11.7trn) has had a brief impact on the yen highlighted by the fact that USD/JPY traded the 160-level today for the first time since intervention took place, probably on 30th April & 6th May. The success of intervention is always determined by whether the fundamental backdrop can reinforce the intervention – and that hasn’t happened. The 2-year UST bond yield has jumped 20bps from the level on the days the intervention took place. That fact alone explains much of why USD/JPY has rebounded so quickly. Although the price of crude oil has fallen since intervention took place, it is on the rise again and the continued reports of escalation in military conflict is placing some serious doubts over the prospects of a near-term reopening of the Strait of Hormuz. We could be close to a tipping point that sees some renewed sharp increases in crude oil prices.

The BoJ at least, now looks to be trying to play its part in providing yen support. The OIS pricing for a rate hike on 16th June has increased by about 5-6bps since intervention took place with the probability of a hike now over 80% and the highest since mid-April. BoJ Governor Ueda is scheduled to speak shortly, and we suspect he will be more forthcoming on the prospect of a rate hike – there is still just under two weeks until the policy announcement but as much as possible Governor Ueda seems likely to lay out the building need for a rate hike given the inflation backdrop.

Part of nearly all BoJ policy guidance planning of a rate hike is using the media to prepare the market. The Nikkei ran a story yesterday that the BoJ is readying to hike rates this month and that crucially it has the backing of the government. Jiji Press ran a similar story and today Finance Minister Katayama stated that the BoJ had the same views, which is telling during a time of media reports of a rate hike being likely.

The increased speculation on a hike has come after a series of strong JGB auctions – yesterday’s 10-year auction bid-to-cover ratio was 3.53 versus a 12mth average of 3.35. Recent 20-year and 30-year auctions also went well. Increased rate hike speculation has not damaged JGB demand and indeed the view that a more credible BoJ could enhance JGB support could well strengthen. The 10-year yield fell 11bps yesterday although some of this has reversed today on Middle East fears and higher crude oil prices. We expect the BoJ to hike although US yields will remain important and USD/JPY could still gain although BoJ action will help contain any move. We still see upside USD/JPY scope as limited to a few big figures. Governor Ueda’s speech takes place at 0930 BST this morning. New tariffs announced by the Trump administration in our view underlines the capacity for renewed US dollar selling once the Middle East conflict is resolved and the Strait of Hormuz reopens.

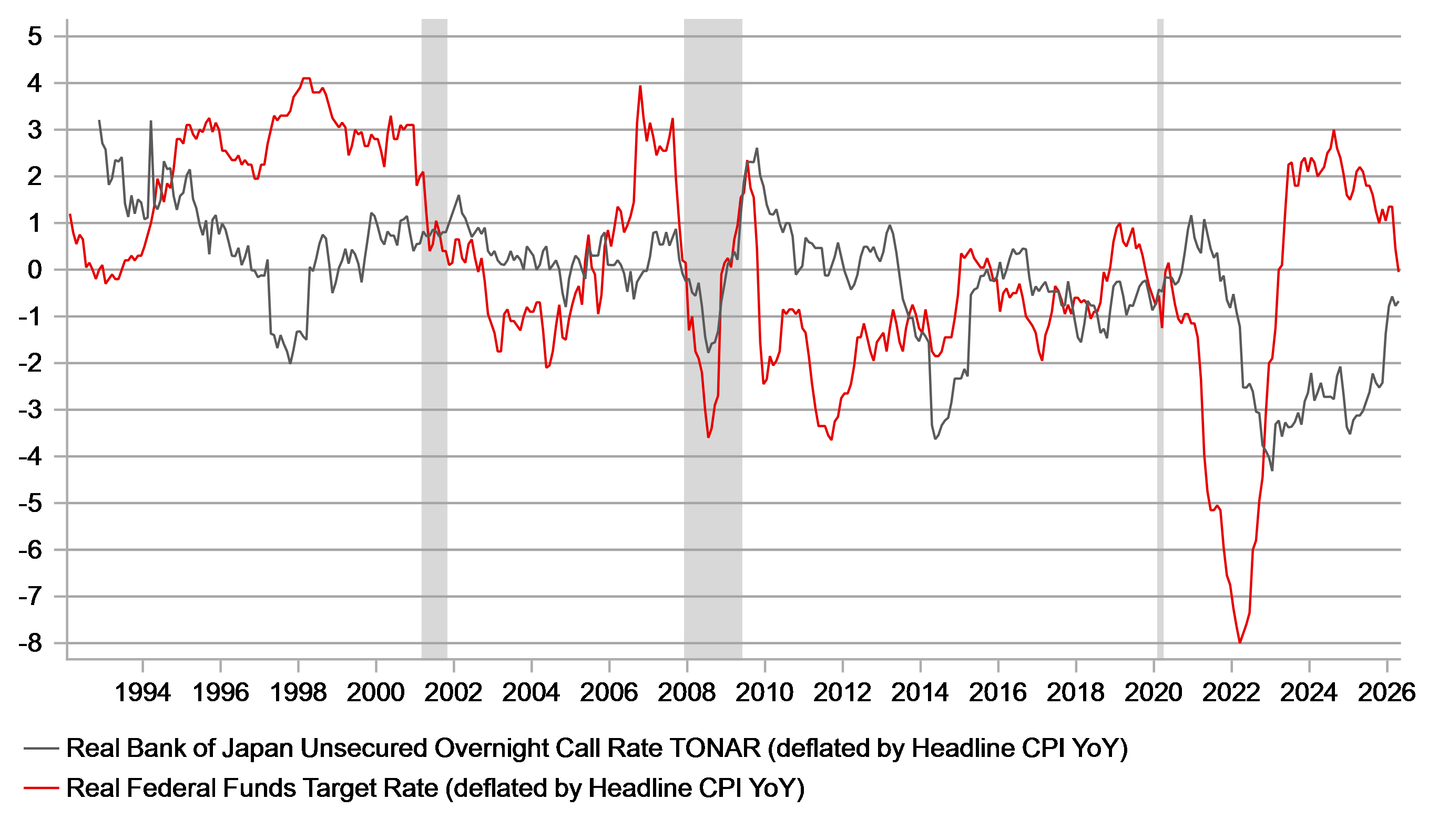

REAL POLICY RATE GAP BETWEEN THE US AND JAPAN IS CLOSING

Source: Bloomberg, Macrobond & MUFG Research

GBP: MPC divisions to persist as market rates do the work

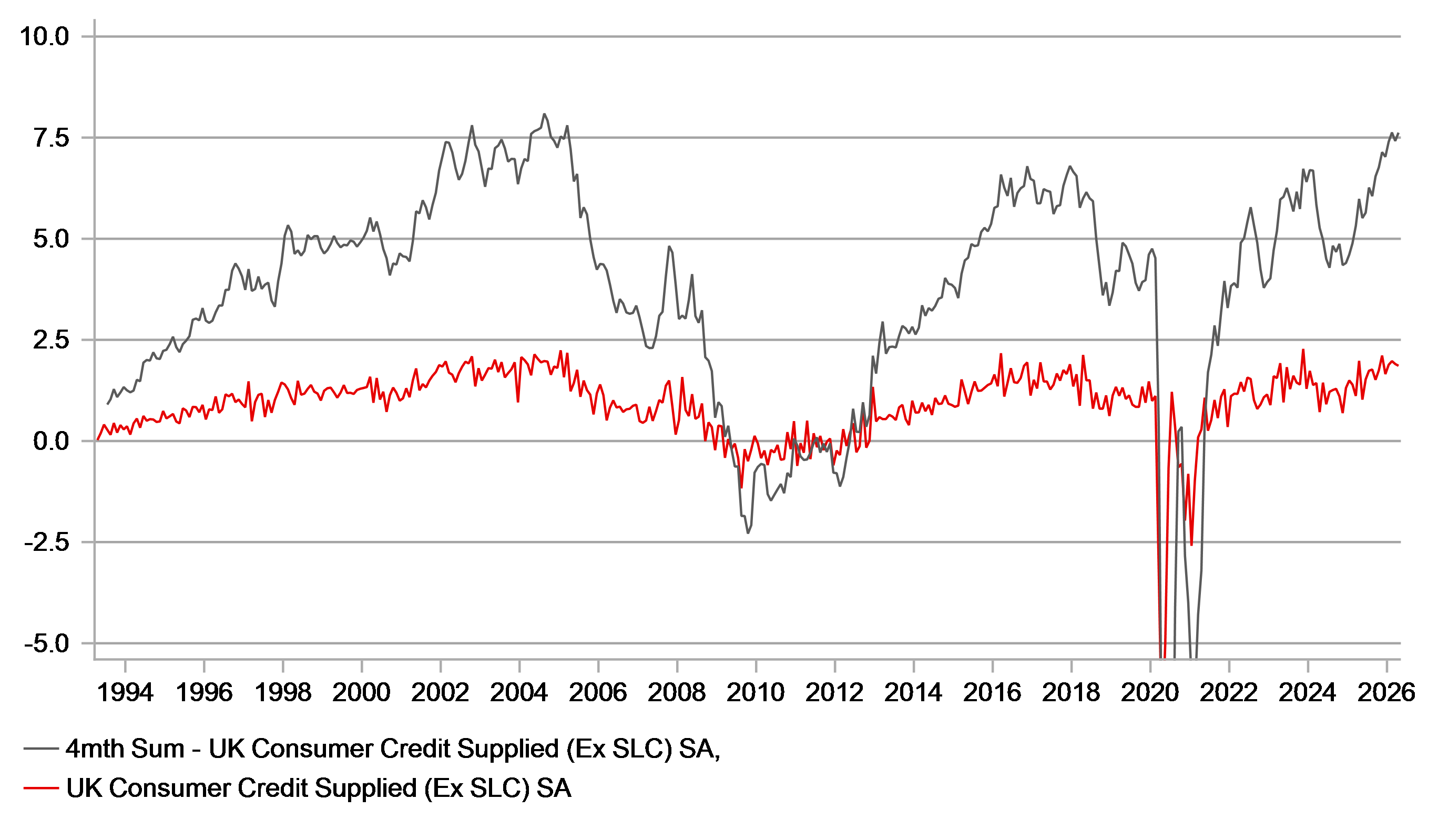

The inflation data released yesterday in Europe was as expected and therefore is unlikely to alter the strong expectations of a rate hike by the ECB at its upcoming meeting on 11th June. The headline YoY CPI rate increased to 3.2% in May as expected although the core rate was a little stronger at 2.5% (expected 2.4%). A rate hike remains fully priced. UK data also pointed to a pick-up in mortgage approvals with buyers possibly bringing forward decisions in anticipation of higher rates to come – mortgage approvals increased to 65.9k in April, the third consecutive increase and the biggest total since January 2025. In other data, net borrowing of consumer credit by individuals totalled GBP 1.9bn in April, stronger than expected while net borrowing by private non-financial corporations totalled GBP 5.5bn, up from GBP 3.7bn in March. Higher rates haven’t yet stifled demand for mortgages or borrowing in general. The 2-year yield in the UK remains around 100bps higher than prior to the start of the US-Iran conflict. That compares to 68bps in the US; 60bps in Germany and 15bps in Japan.

The lack of progress on getting the Strait of Hormuz reopened looks like it has increased concerns for one of the most hawkish members of the MPC. Megan Greene spoke yesterday in Derby (titled : “Here we go again? Assessing the inflation risks of the recent energy shock”) and made clear that the MPC should not rely on the financial market tightening to keep inflation in check. You could argue that yesterday’s UK borrowing data backs Megan Greene’s view up. If households and companies anticipate higher borrowing costs it could fuel demand in anticipation of future rises. Greene also added that acting sooner is as important as its size in attempting to keep inflation expectations anchored.

We continue to see grounds for the BoE hiking and suspect that Megan Greene’s views will grow in popularity the longer the Strait of Hormuz remains closed. Based on this speech there is certainly a risk that Megan Greene could join Chief Economist Huw Pill in voting for a 25bp hike at the next meeting on 18th June. Governor Bailey also spoke (in the House of Lords) and stated that the BoE “had time” to assess given tighter financial conditions. A hike certainly seems unlikely in June based on Bailey’s comments but if uncertainty persists much longer it appears likely that the MPC will vote to hike on 30th July. That is currently only priced as a 50-50 prospect so there is scope for market yields to move higher, especially at the front-end. All else equal that should provide support for the pound, more against the euro where monetary policy pricing looks more realistic than potentially in the US. Political and associated fiscal uncertainties though could still get in the way of any rate driven pound strength.

UK CONSUMER CREDIT – 4MTH ROLLING SUM TOTAL UNDERLINES STRONG START TO 2026 & LIMITED IMPACT IN MARCH/APRIL FROM HIGHER RATES

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

GE | 08:55 | German Services PMI | (May) | 47.8 | 46.9 | !! |

GE | 08:55 | German Composite PMI | (May) | 48.6 | 48.4 | !!! |

EC | 09:00 | Services PMI | (May) | 46.4 | 47.6 | !! |

EC | 09:00 | S&P Global Composite PMI | (May) | 47.5 | 48.8 | !!! |

UK | 09:30 | Composite PMI | (May) | 48.5 | 52.6 | !!! |

UK | 09:30 | Services PMI | (May) | 47.9 | 52.7 | !!! |

JP | 09:30 | BOJ Gov Ueda Speaks | - | - | - | !!! |

EC | 10:00 | PPI (YoY) | (Apr) | 4.8% | 2.1% | ! |

EC | 10:00 | PPI (MoM) | (Apr) | 0.6% | 3.4% | ! |

EC | 10:50 | ECB's Elderson Speaks | - | - | - | !! |

US | 13:15 | ADP Nonfarm Employment Change | (May) | 116K | 109K | !!!! |

US | 14:45 | Services PMI | (May) | 50.9 | 51.0 | !!! |

US | 14:45 | S&P Global Composite PMI | (May) | 51.7 | 51.7 | !! |

US | 15:00 | ISM Non-Manufacturing PMI | (May) | 53.7 | 53.6 | !!! |

US | 15:00 | ISM Non-Manufacturing Prices | (May) | - | 70.7 | !!! |

US | 15:00 | Factory Orders (MoM) | (Apr) | 4.6% | 1.5% | ! |

US | 15:00 | Durables Excluding Transport (MoM) | (Apr) | - | 1.1% | ! |

US | 19:00 | Beige Book | - | - | - | !! |

US | 21:00 | Fed Logan Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com