US jobs data to help reset market pricing on Fed policy

USD: Reverting to reality

We have stated here recently and in the Foreign Exchange Outlook released on Wednesday (here) that market pricing on Fed policy had become excessive with close to two rates hikes priced by March 2027. The nonfarm payrolls data for June, released yesterday, should be a key catalyst for market pricing reverting to what we believe is a more realistic outcome – pricing a greater risk of a rate cut rather than rate hikes. The 3-month average for NFP prior to yesterday’s data looked excessive at 188k and after the June data and downward revisions to April and May the 3-month average has fallen back to 111k. This is still well above the 12mth average of 42k but we see the 12mth level as more reflective of the current state of the labour market and further slowing of jobs growth looks likely going forward.

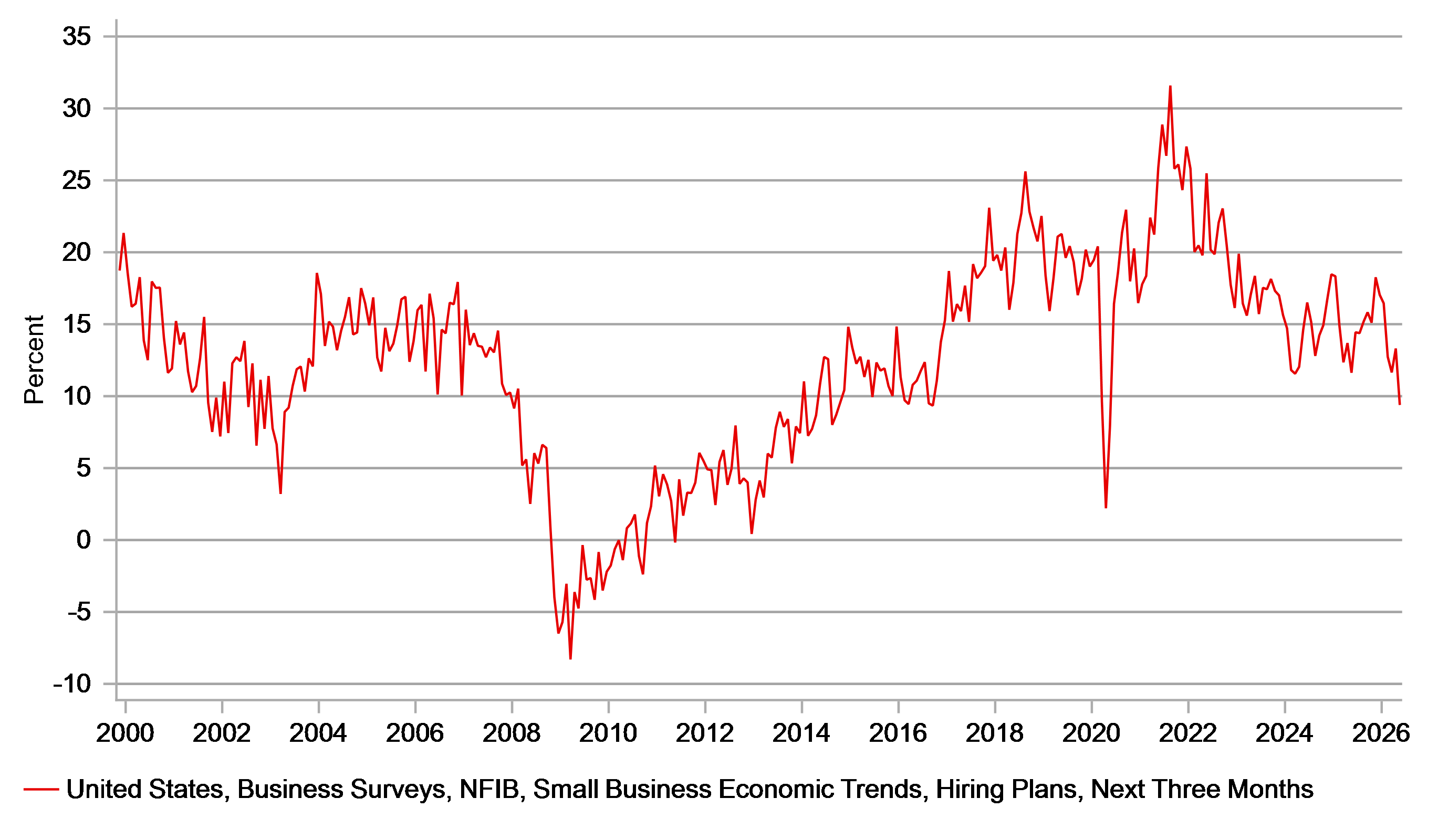

Nearly every labour market sentiment data is pointing to a jobs market that is weaker than the recent NFP prints suggest, even after yesterday’s weaker report. The NFIB Hiring Plans index is falling notably and is now at the lowest level since 2016. The Consumer Confidence labour market index dropped to the lowest level since the post-covid period in 2021 and the household survey data continues to point an unfavourable mix keeping the unemployment rate low. The household survey yesterday revealed a 720k drop in the labour force and a 507k drop in employment. Employment has declined by 1.728mn so far in 2026 and the labour market has shrunk by 2.137mn.

So the nine FOMC members that indicated the need for at least one rate certainly do not have the same justifications for that now. The jobs market is weaker than was implied at the FOMC meeting and as Fed Chair Warsh stated in Sintra this week, the inflation risks have receded over the last four weeks. The dots from each member were likely submitted the week before the FOMC meeting June when Brent crude oil was trading above USD 90pbl – we have dropped over USD 20pbl since. As well as energy, other factors will likely contribute to disinflation in H2 – tariff unwind and rents.

Based on OIS pricing, there is still a 20% probability of a 25bp rate hike at the next FOMC meeting on 29th July and a 60% probability of a hike by September. The rates curve remains over-priced and market participants appear to be placing too much emphasis on Warsh’s comments at his first FOMC press conference. Warsh was always going to stress the importance of achieving the Fed’s inflation goal and his acknowledgement in Sintra that inflation risks are receding is important and coupled with the weaker NFP yesterday will allow the Fed to remain on hold, possibly through the remainder of the year.

A retracement of the post-FOMC US dollar rally certainly looks achievable over the near-term with the dollar overbought and positioning indicating longs were quickly extended. There is nothing next week to turn momentum back in favour of the dollar which means the next big event-day will be 14th July when we get the June CPI data and the semi-annual testimony from Fed Chair Warsh.

NFP DATA WAS MORE IN LINE WITH LABOUR MARKET SURVEY DATA

Source: Bloomberg, Macrobond & MUFG Research

EUR: LNG price stickiness underlines inflation risks not fully removed

The rates and FX markets are subdued this morning and that could well continue given the US holiday ahead of Independence Day tomorrow. The bias will favour further US dollar weakness following the payrolls report but EUR could also be supported by the rates curve maintaining pricing for another hikes as US yields fall back on easing Fed rate hike expectations. ECB President Lagarde in an interview in Les Echos stated that “we are convinced we made the right decision” on raising rates in June. She added that a “large majority” were ready to hike in April but needed more information.

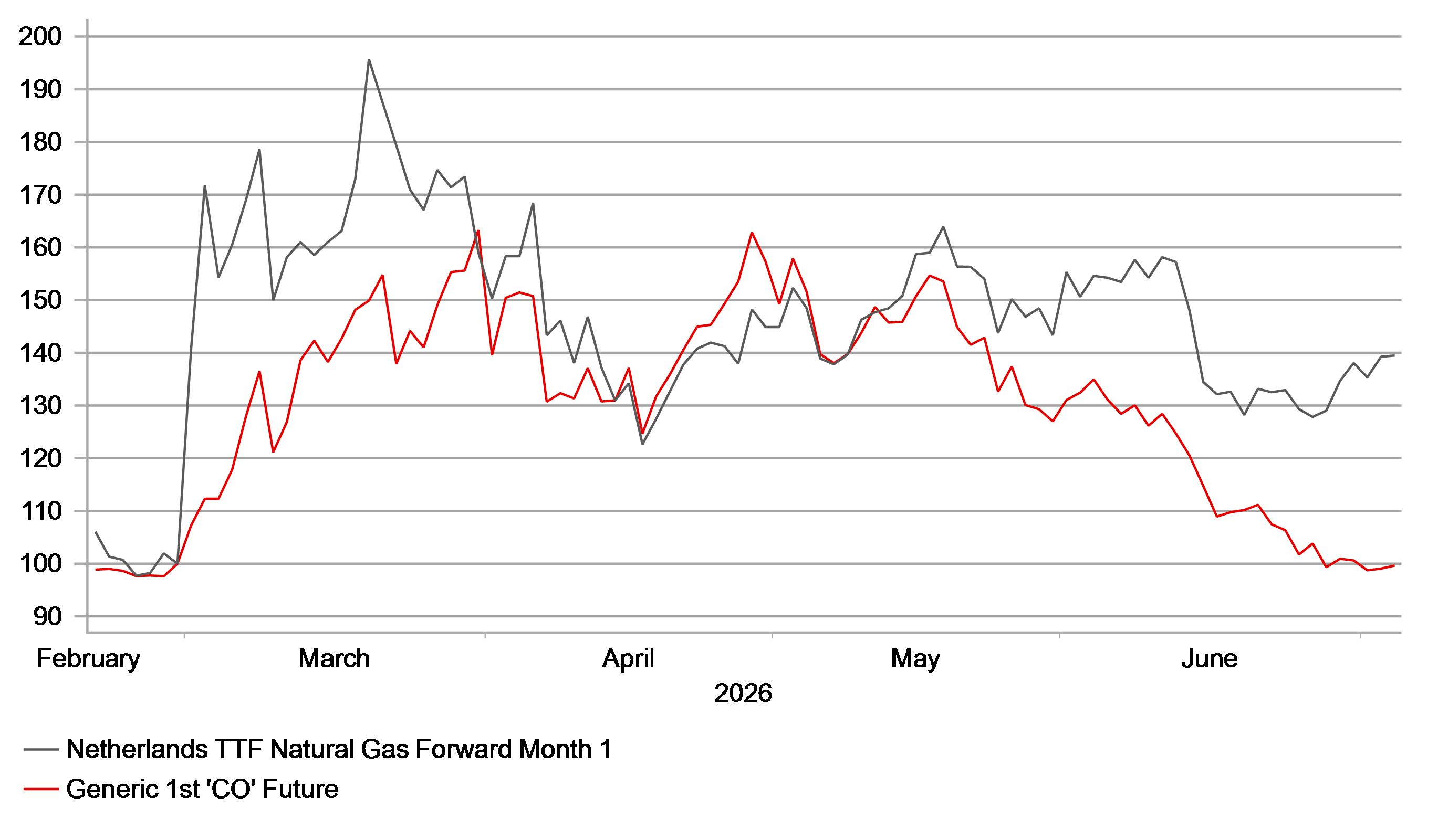

Inflation risks may have subsided in Europe, but the level of risk remains higher than before the conflict. Data this week continued to show crude oil tanker traffic picking up but the same cannot be said for LNG shipments. A US official stated that crude oil through the Strat if at about 10mn b/d, about 50% of pre-conflict levels while Saudi shipments have returned to 90% of pre-conflict levels. Qatar LNG shipments have not picked up in any meaningful way and QatarEnergy extended force majeure on some LNG shipments this week. Bloomberg also reported an LNG tanker being diverted from Europe due to intense competition. While Brent crude oil has completely reversed the post-conflict surge, LNG prices remain more elevated, at 40% above pre-conflict levels. That matters a lot for the ECB in assessing inflation risks in Europe.

The growth backdrop may also see some improvement with the outlook for the German economy helped by the announced plans to overhaul the economy. The government yesterday announced 34 measures, including tax and welfare benefit cuts, a relaxation of labour market rules and the cutting of red tape to help fuel investment. The tax cut measures are estimated to total EUR 10bn but there has already been criticism that the measures didn’t go far enough. At the margin this is positive for economic growth but is unlikely to move the dial in terms of shaping ECB behaviour on monetary policy going forward. That’s reflected by the fact that the bund yield curve has shifted higher by about 1bp today.

More likely the ECB will be monitoring energy prices and the scale of retracement since the ceasefire extension was agreed and the Strait of Hormuz reopened is not yet enough to eliminate energy-related inflation risks. That will keep the ECB biased toward hiking rates again.

WHILE BRENT CRUDE OIL HAS FULLY RETRACED THE POST-CONFLICT PRICE SURGE NATURAL GAS PRICES IN EUROPE REMAIN 40% HIGHER

Source: Bloomberg, Macrobond & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

FR | 08:50 | French Services PMI | (Jun) | 47.4 | 44.3 | !! |

FR | 08:50 | French S&P Global Composite PMI | (Jun) | 47.6 | 44.9 | ! |

GE | 08:55 | German Services PMI | (Jun) | 46.8 | 48.1 | !! |

GE | 08:55 | German Composite PMI | (Jun) | 48.0 | 48.8 | ! |

EZ | 09:00 | Services PMI | (Jun) | 48.9 | 47.7 | !! |

EZ | 09:00 | S&P Global Composite PMI | (Jun) | 49.5 | 48.5 | !! |

EZ | 09:00 | ECB President Lagarde Speaks | - | - | - | !!! |

UK | 09:30 | Composite PMI | (Jun) | 49.4 | 49.7 | !!! |

UK | 09:30 | Services PMI | (Jun) | 48.7 | 49.3 | !!! |

UK | 16:00 | BoE Gov Bailey Speaks | - | - | - | !!! |

Source: Bloomberg & Investing.com