Hope contains US dollar rebound

USD: US dollar remains range-bound despite oil rebound

Yesterday Iran’s semi-official Tasnim news agency reported that Tehran has suspended negotiations in response to Israeli operations in Lebanon. Notably, Iranian officials have long pushed for Lebanon to be explicitly included in any US-Iran ceasefire framework, but this demand has been sharpened considerably following the latest developments. The reported suspension came shortly after President Trump requested amendments to the draft agreement, including changes related to Iran’s highly enriched uranium (HEU) and oversight of the Strait of Hormuz. In response, Iranian officials, via state-affiliated Fars News, flagged “concerns” over the proposed revisions, reiterating that HEU will not be transferred to the US and that Iran must retain control over the Strait. As a result, Tehran appears to have re-emphasised its maximalist positions, particularly that any deal must extend to Lebanon.

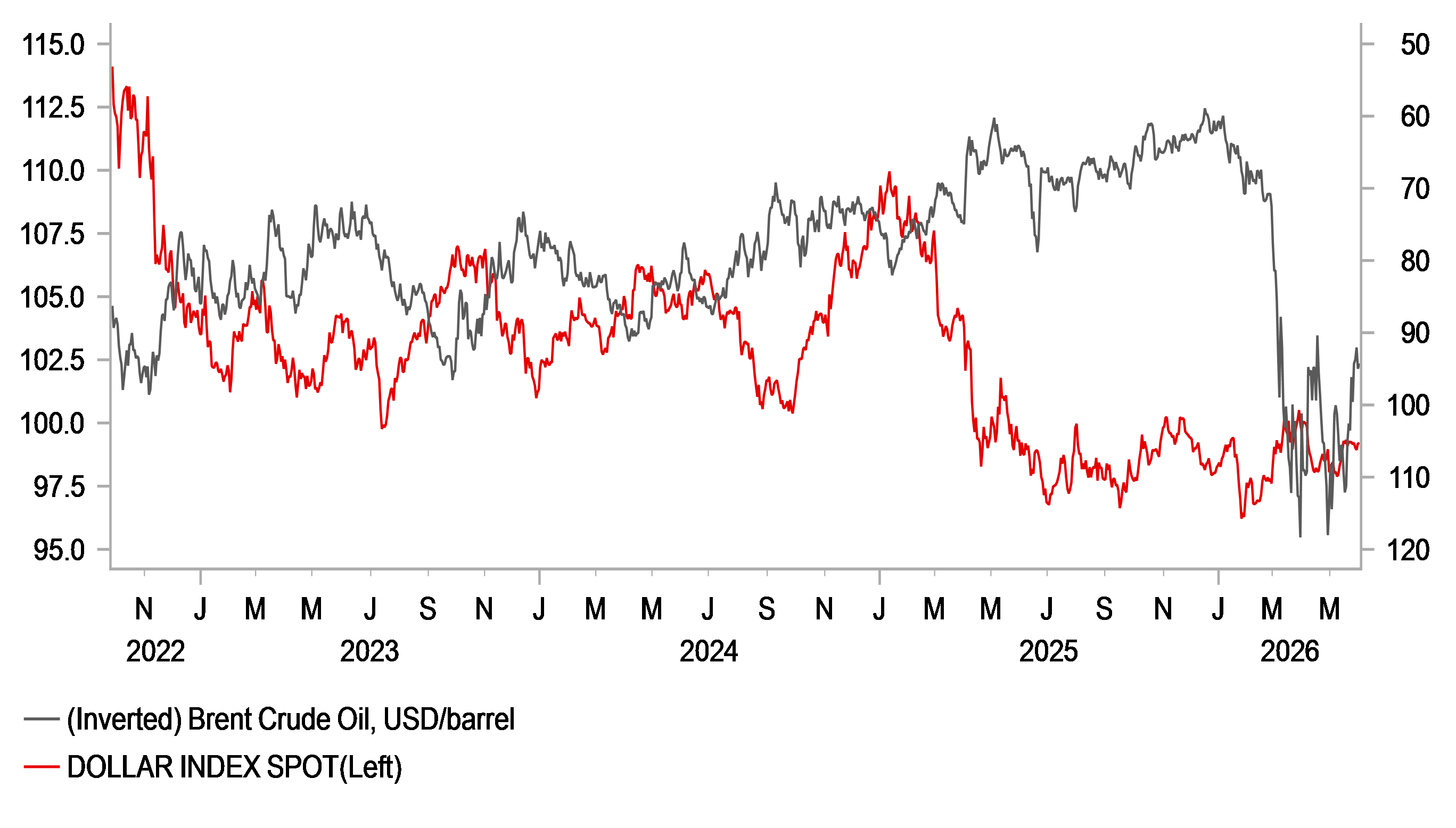

As a result, Brent surged 4.2% on Monday to settle at $94.98/bbl, marking its largest daily gain in a month. President Trump moved quickly to calm nerves, signalling that Israel and Hezbollah are moving towards a halt in fighting and that negotiations are continuing “at a rapid pace.” Net-net, markets continue to price this as a live but contained situation, enough to keep oil elevated, but not enough to disrupt markets. Oil has dropped today on the hope that the pause in hostilities between Israel and Lebanon will be enough to keep negotiations alive. US yields are lower as a result the dollar rebound will likely remain curtailed.

From a geopolitical standpoint attention today turns to US Secretary of State Rubio, who testifies before Congress for the first time since the conflict began. His remarks could provide further clarity on the diplomatic outlook going forward.

In Europe, the policy outlook has firmed definitively, there is now little doubt the ECB will deliver a rate hike at its 11th June meeting, with markets once again fully pricing a move for the first time since early May. Eurozone CPI is expected to rise to 3.2% y/y in May, reinforcing the ECB message for action. The rebound in oil yesterday drove yields higher in Europe with front-end spreads moving in favour of EUR, a key factor in the US dollar rebound yesterday being contained.

MARKETS TREAT ELEVATED OIL CAUTIOUSLY

Source: Bloomberg, Macrobond & MUFG Research

USD: US economic resilience on show again

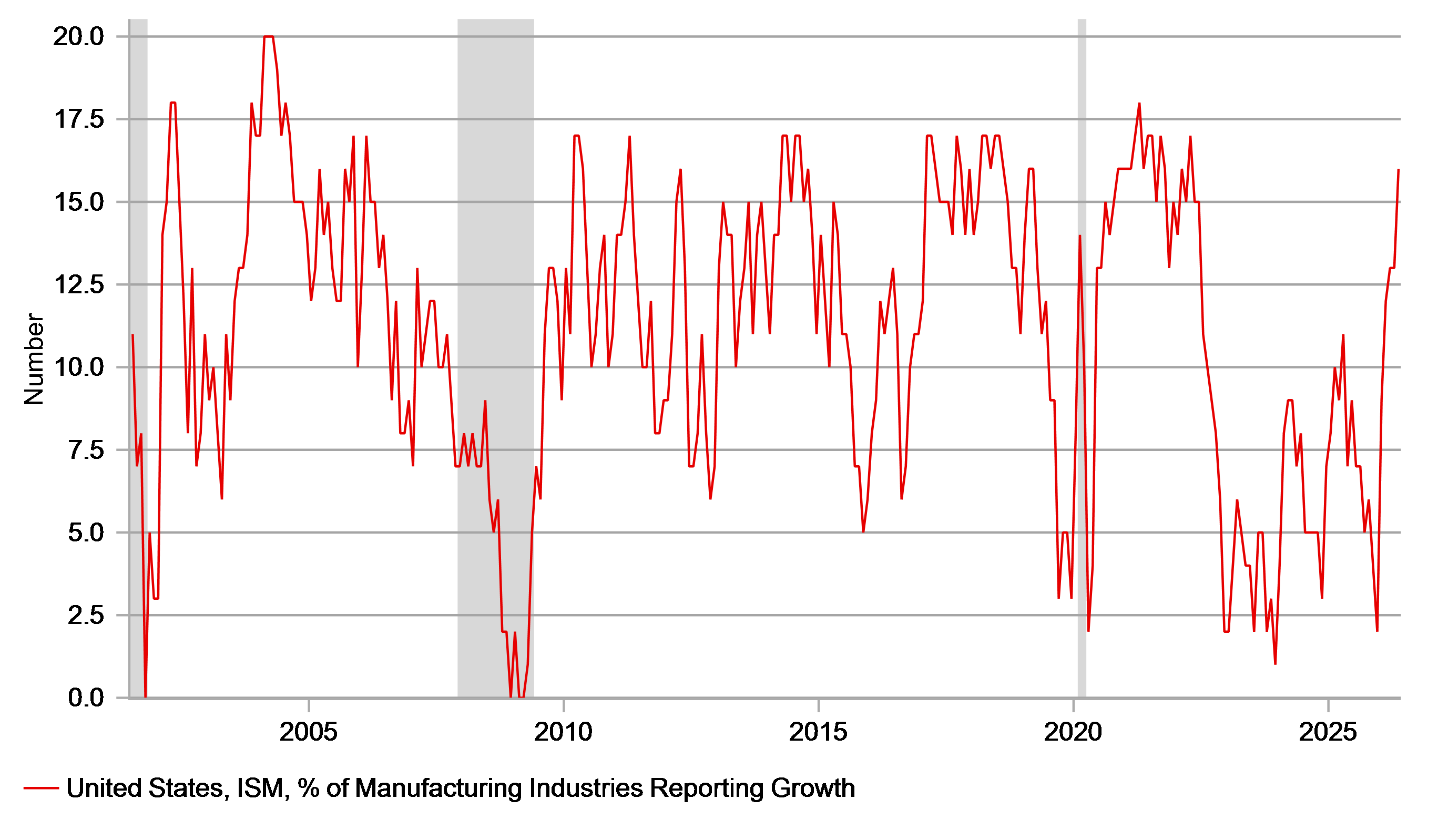

The renewed pessimism over finding a resolution in the US-Iran conflict after two weeks of optimism highlights the back and forth in expectations over the path forward in the Middle East. That uncertainty is generally bad for business, but the ISM Manufacturing report yesterday suggested US companies are managing to deal with this uncertainty that has now existed for three months. The overall index jumped to 54.0 in May, the highest in four years with four of the five sub-indices that contributes to the headline index all rising. There is certainly limited evidence here of any slowdown and that will add to upside inflationary risks. The chart above highlights the percentage of manufacturing industries reporting growth (respondents mostly tend to respond that conditions are unchanged) – the total is close to the post-covid high.

The reason for possible caution here is that given US companies’ experience of supply-chain problems in the post-covid era that this strength is more a reflection of stock-building to prepare for such problems remerging again and that may well mean this scale of strength is not sustained but the AI-related tech demand is likely another factor that is helping fuel the resilience. The fact that the New Orders index jumped does point to this strength potentially being sustained. There are also signs of momentum that pre-dates the conflict – the production index increased 0.9ppts to 54.3, the seventh consecutive month of increase. Supplier delivery times lengthened showing supply constraints, the index remained at 60.6, the highest since June 2022. The fact that the index didn’t increase does suggest those constraints may be easing.

The ISM respondent comments section there were numerous mentions of tech-related demand with price rises related to data-centre demand one example where tech also is likely playing a role in the overall resilience in manufacturing.

The rise in yields yesterday was certainly more related to the possible breakdown in negotiations between the US and Iran but the economy is continuing to show evidence of economic weakness that will make it more difficult for the Fed to argue that looking through the energy price shock is a credible strategy. If the Strait of Hormuz remains closed and the employment data this week does not show any deterioration, yields and the dollar look set to strengthen further.

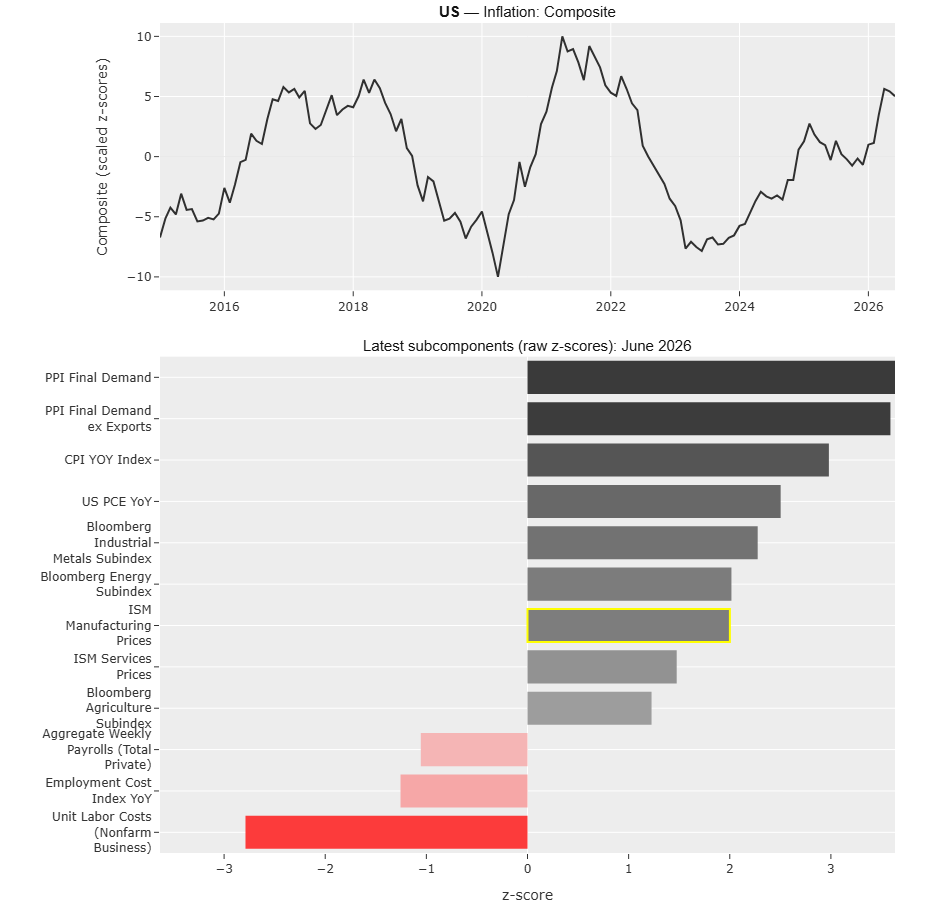

From a modelling perspective, the ISM manufacturing prices index remains a key input into our US inflation composite index. Although the manufacturing PMI has had a diminished direct market impact in recent years, it continues to provide a reliable signal on the cyclical backdrop. On a rolling two-year basis, the latest ISM manufacturing prices index represents a +2 standard deviation shock, adding upward pressure to the overall index. We continue to weigh the component heavily given its leading properties.

Looking at the rest of the components for our US inflation composite index, we see energy and manufacturing inputs continue to drive inflation pressures. Elevated oil and commodity prices are reinforcing upstream price pressures. By contrast, domestic wage dynamics remain contained and are not a key driver of current inflation trends.

THE PERCENTAGE OF ISM INDUSTRIES REPORTING EXPANSION HAS REBOUNDED SHARPLY TO POST-COVID HIGHS

Source: Macrobond, Bloomberg & MUFG Research

US INFLATION COMPOSITE INDEX – SUBCOMPONENT BREAKDOWN

Source: Macrobond, Bloomberg & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

EU | 10:00 | CPI (YoY) | (May) | 3.3% | 3.0% | !!! |

EU | 10:00 | CPI (MoM) | (May) | - | 1.0% | !! |

EU | 10:00 | Core CPI (YoY) | (May) | 2.4% | 2.2% | !! |

UK | 15:00 | BoE Gov Bailey Speaks | - | - | - | !!! |

US | 15:00 | JOLTS Job Openings | (Apr) | 6.870M | 6.866M | !!! |

Source: Bloomberg & Investing.com