Strong Tankan report but can the yen continue to gradually weaken?

JPY: Scope for continued inaction

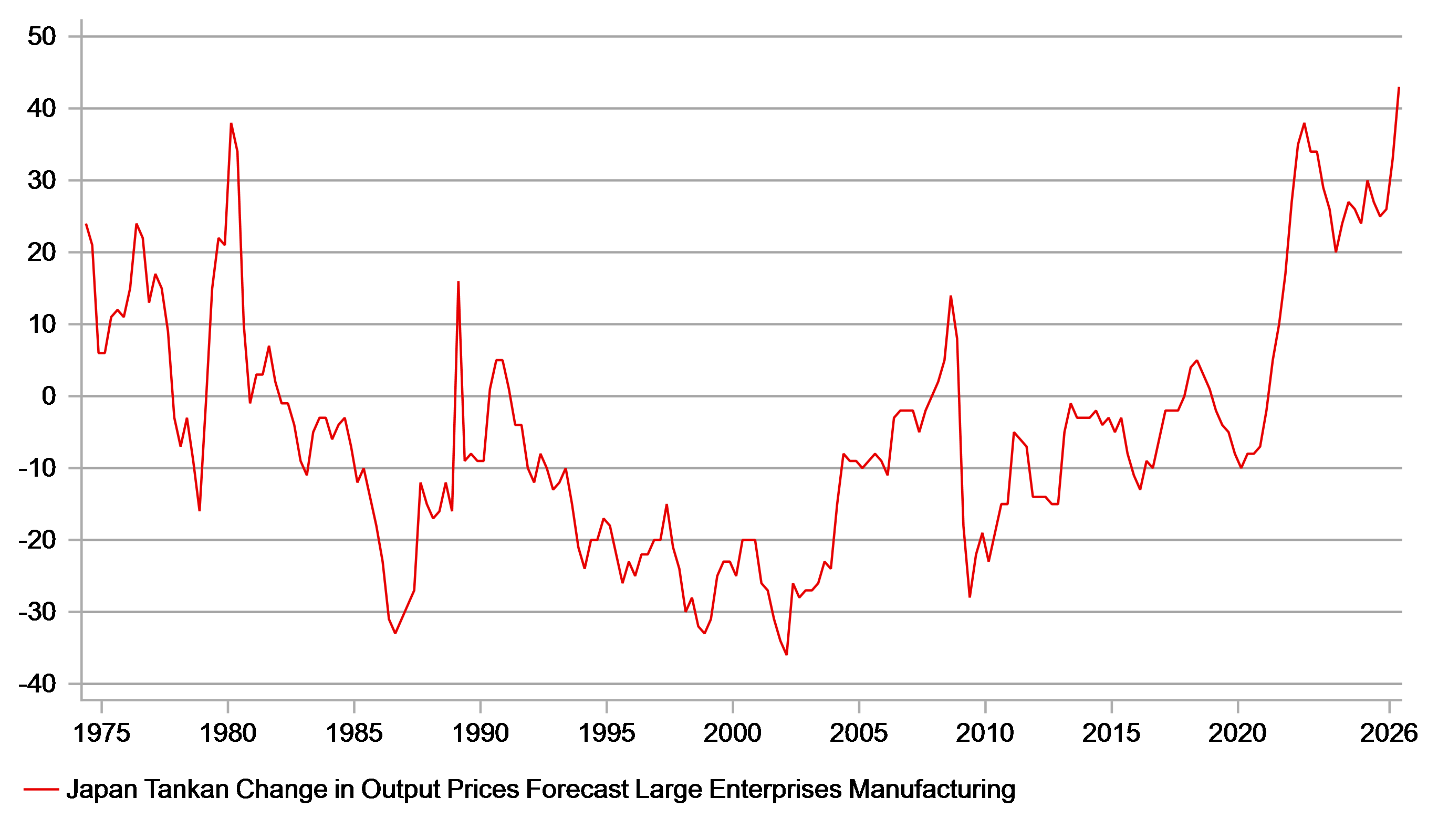

The quarterly Tankan report, released from the BoJ today was stronger than expected and certainly endorses the rate hike by the BoJ in June and strengthens the case for further hikes going forward. The large manufacturers’ diffusion index jumped 5pts to 22, the highest level since Q1 2018 the biggest q/q increase since the recovery period following covid. The BoJ, in particular, will likely take note of the indices on output price forecasts that suggests stronger inflation pressures ahead. The forecast for output prices jumped to 43 in the latest survey, surpassing the peak during the 2022 global inflation shock and to a new record level set in 2022 and matched back in 1980. The BoJ places a lot of weight on its quarterly corporate sentiment survey and will potentially strengthen the case for considering a faster pace of tightening.

That remains a low-priced scenario in the markets with OIS pricing indicating just 6bps of tightening priced for September but close to a full hike by December. The risk to inflation stemming from further yen depreciation is building and hence given the inflation readings in this Tankan report, the BoJ may turn further hawkish. Vice Finance Minister for International Affairs, Atsushi Mimura, today gave an in-depth interview to Bloomberg and clearly used this interview to counter the view that the intervention by the MoF in April/May was a failure. Of course, if you reconsider the objective of intervention that case can be credibly made. It’s quite likely that at the time the MoF did not view the intervention as enough in itself to turn the yen stronger sustainably and that the objective was merely to curtail or slow yen depreciation. On that metric the intervention does look to have had some success. Looking at G10 FX performance, in H1 the yen is the second worst performing G10 currency. But looking at performance since intervention, the yen’s depreciation versus the dollar is the least compared to all other G10 currencies.

However, the danger is that this curtailed yen selling versus the dollar relative to the rest of G10 does not continue. The MoF rhetoric on intervention has subsided – indeed Mimura today did not mention the threat of intervention in his interview and if market participants sense a shift in strategy, the scale of yen selling could pick up quickly.

With USD/JPY volatility still relatively low (1-month implied between 6-7%, the lowest since before Russia’s invasion of Ukraine), the JGB market relatively stable for now and equities at record highs, allowing a slow grind higher could well be the MoF strategy for now. There is always a risk in low-liquid market conditions on Friday when the US is on vacation that you could see intervention especially if the pace of yen selling was to pick up. The current pace of yen selling appears acceptable and if maintained could see the MoF remain on the sidelines.

NEW RECORD SELLING PRICE FORECAST FOR JAPANESE ENTERPRISES

Source: Bloomberg, Macrobond & MUFG Research

USD: Sintra in focus as inflation fears ease

The gathering in Sintra, Portugal comes to an end today with the key event – a panel discussion with Fed Chair Warsh, ECB President Lagarde, BoE Governor Bailey and BoC Governor Macklem at 14:00 BST. The OIS curves for these countries all show differing degrees of rate hike expectations over the next nine to twelve months that largely reflects inflation risks related to energy inflation pass-through. But crude oil prices have fallen markedly and we suspect more quickly than most central bankers had assumed when their last meetings took place just last month.

Given the ECB is one the central bank that has responded to this inflation risk by hiking, we doubt President Lagarde will playing down at this stage the inflation risks from energy prices. As we highlighted here yesterday Philip Lane has pointed out that the 2027 and 2028 crude oil prices were still higher than pre-war levels underlining that energy risks remain more elevated and hence caution continues to be warranted. BoE Governor Bailey too is likely to be cautious over diminishing inflation risks given the BoE Chief Economist remains the most vocal hawk on the MPC.

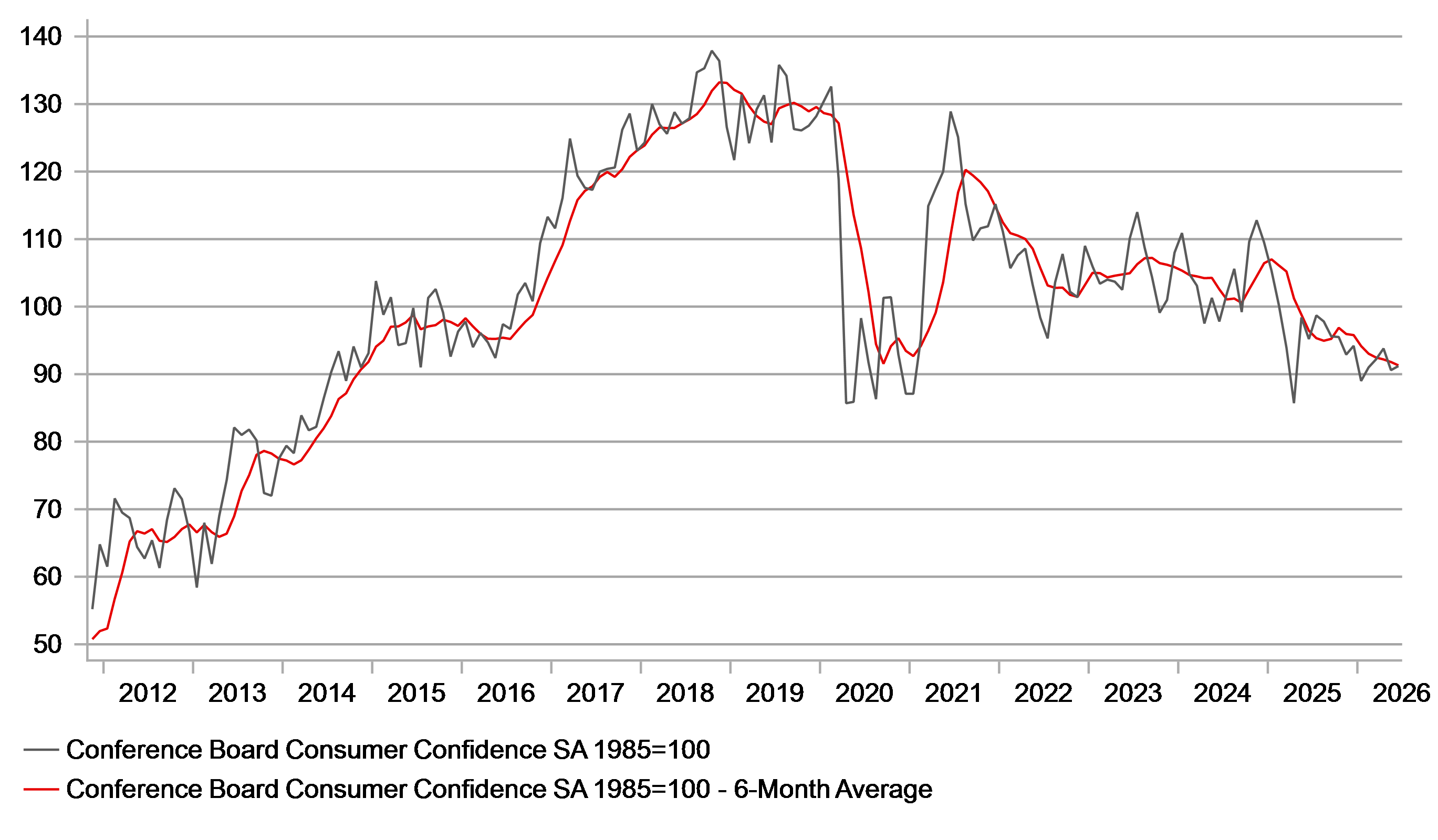

The words from Fed Chair Warsh will be most interesting. Given his dislike of forward guidance, we are unlikely to get much in terms of policy bias but he will still be free to express his views on the economy and inflation. Data released yesterday certainly points to an economy weaker than some of the official data implies. The Conference Board Consumer Confidence report was much weaker than expected – the weaker reading and the downward revision to May meant that the 6-month average reading fell below the covid low and to a level not seen since 2014. This at a time of record highs for US equity markets and underlines the fact that not everybody is benefiting. The overall drag comes from the Present Situation index which fell to the lowest level since February 2021. That index is closely tied to the labour market, and the Labour Market Differential (jobs plentiful minus jobs hard to get) fell to the lowest level also since February 2021, when the unemployment rate was at 6.2%. The deterioration in labour market sentiment is certainly not consistent with a continued improvement in nonfarm payrolls and the 188k 3mth average looks likely to slow over the coming months.

The JOLTS job opening data was certainly more positive and near-term sentiment will be determined by the NFP print tomorrow. But consumers generally remain grim and that points to the non-AI economy remaining subdued. With inflation set to fall, we see current Fed rate hike pricing reversing and hence see limited scope for much extension to this period of US dollar appreciation.

US CONSUMER CONFIDENCE CONTINUES TO TREND WEAKER WITH 6-MONTH AVERAGE BACK AT 2014 LEVELS

Source: Bloomberg, Macrobond & MUFG Research

KEY RELEASES AND EVENTS

Country | BST | Indicator/Event | Period | Consensus | Previous | Mkt Moving |

FR | 08:50 | French Manufacturing PMI | (Jun) | 50.7 | 49.7 | !! |

GE | 08:55 | German Manufacturing PMI | (Jun) | 50.0 | 50.1 | !! |

EZ | 09:00 | Manufacturing PMI | (Jun) | 51.3 | 51.6 | !! |

UK | 09:30 | Manufacturing PMI | (Jun) | 53.1 | 53.9 | !!! |

EZ | 10:00 | CPI (MoM) | (Jun) | 0.10% | 0.1% | !! |

EZ | 10:00 | CPI (YoY) | (Jun) | 3.0% | 3.2% | !!! |

EZ | 10:00 | Core CPI (YoY) | (Jun) | 2.5% | 2.6% | !! |

EU | 11:15 | ECB's Lane Speaks | - | - | - | !! |

US | 13:15 | ADP Nonfarm Employment Change | (Jun) | 118K | 122K | !!! |

US | 14:00 | Sintra Panel Discussion - Warsh; Lagarde; Bailey | - | - | - | !!!! |

US | 14:45 | Manufacturing PMI | (Jun) | 55.7 | 55.1 | !! |

US | 15:00 | ISM Manufacturing PMI | (Jun) | 53.8 | 54.0 | !!! |

US | 15:00 | Construction Spending (MoM) | (May) | 0.1% | 0.4% | !! |

US | 15:00 | ISM Manufacturing Prices | (Jun) | 77.7 | 82.1 | !!! |

EZ | 15:30 | ECB President Lagarde Speaks | - | - | - | !! |

Source: Bloomberg & Investing.com