Please download PDF using the link above for the full report

A base case, where the Iran war and the Hormuz disruption unwind approaching end of May, is our core case. We expect:

1) A mild dent on China growth (4.7%yoy for 2026, down from prior forecast of 4.8%yoy); and a broadly resilient activity as the shock remains largely price- and margin-driven rather than supply constraining.

2) PPI rises, but CPI stays anchored due to China’s weak oil price shock pass-through – this will keep the PBOC to remain easing-biased.

3) USDCNY: the pair may range‑bound in most time of May, before declines to 6.75 by Q2 and 6.65 by end‑2026, under our assumption of a deal reached and eventual reopening of the Strait of Hormuz in late May.China’s energy buffers (3–4 months of import cover) provide short‑term resilience but remain finite. With high exposure to Middle Eastern supply, prolonged disruption would shift the shock from price‑ to supply‑driven, worsening terms of trade, weakening the trade balance, and creating a non‑linear drag on growth (toward ~4%yoy in a Severe Scenario). This would likely trigger renewed outflows and tilt the CNY from resilience toward depreciation pressure.

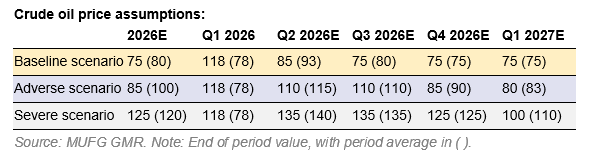

Crude oil price assumptions