Week Ahead FX outlook:

Key FX views:

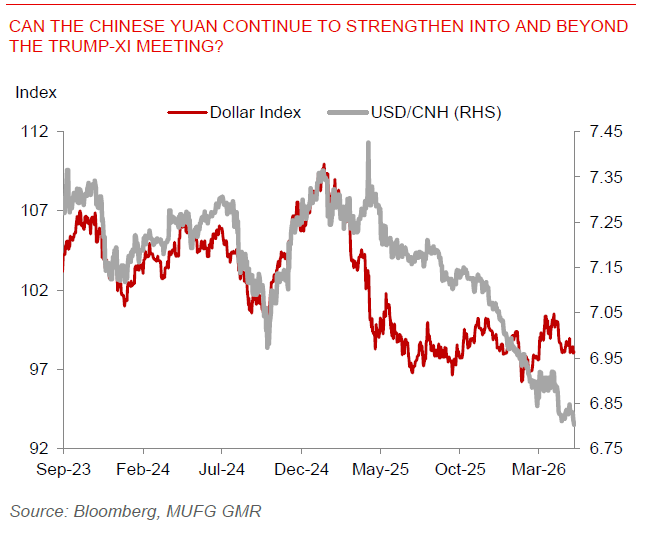

The key event in the week ahead is President Trump’s visit to Beijing for talks with President Xi on 14-15 May. This is Trump’s first visit to China since 2017, and also comes on the backdrop and shadow of the Iran conflict and Strait of Hormuz closure. While there are certainly many ways this meeting could pan out, we tend to be cautiously optimistic on potential outcomes, even as we don’t think that there will be meaningful agreements on the most difficult topics at play between the two superpowers such as semiconductors. Areas of potential agreement include agriculture purchases, and possible verbal commitments around keeping supply chains open, but the key goal as with all complicated relationships is to do no harm and make sure communication lines remain open.

This geopolitical backdrop makes China’s domestic data particularly important. China’s April trade figures are expected to show exports still holding up, helped by shipments being redirected toward non-US markets, while imports should remain firm on stockpiling and AI-related demand. However, the bigger question is whether higher energy and logistics costs from the Iran conflict are starting to feed into China’s price dynamics. Overall the general trend for China seems to be some gradual pick-up in producer price pressures in part driven by this external supply shock, but whether this is positive for a China weighed down by deflationary impulses also depends on the success of authorities in curbing race to the bottom through reducing involution-driven competition pressures.

Across the rest of Asia, the Iran shock will be filtered mainly through oil prices, inflation expectations and external balances. Markets will also closely watch on whether negotiations between the US and Iran make any meaningful headway. India’s CPI is expected to rise modestly helped by continued implicit and explicit energy subsidies by the government and Oil Marketing Companies, although food-price risks and higher crude prices keep the balance of risks tilted upward. India’s trade deficit is also expected to widen, but with import disruptions to gold since April 2026 likely to cap the extent of widening in the near term.

Can the Chinese Yuan continue to strengthen into and beyond the Trump-Xi Meeting?