Week Ahead FX outlook:

Key FX views:

The main macro focus in our region next week will be on the FOMC minutes, China’s inflation and credit data, Japan wages, and several regional inflation and central bank decisions across Asia. In particular, China’s June CPI and PPI will be closely watched for signs of an improvement in nominal activity, even as some of price increases is likely driven by supply-side and energy-related changes. Meanwhile, aggregate financing data will also be watched for signs of domestic demand trends, but with government financing so far appearing softer than what we saw last year. Japan’s May labor cash earnings are expected to remain robust at around 3.4%yoy. Overall we are expecting Bank of Japan to hike rates by another 50bps through our forecast horizon, and we think the timing will likely be faster than what markets are currently pricing in. Elsewhere in Asia, Thailand, the Philippines and Taiwan release CPI data, with Philippine inflation expected to ease slightly but remain above the BSP’s inflation target, and for inflation in Thailand and Taiwan to inch higher. We think the BSP should continue to raise rates by another 50bps in 2026 to help manage inflation expectations, while we see both Thailand and Taiwan as biased to keep rates on hold for an extended period, and as such anchoring the front-end of the TWD and THB rates curve.

Policy decisions in New Zealand and Malaysia should add to the regional rates narrative. We expect Bank Negara Malaysia to hold its policy rate at 2.75% as benign inflation and fuel subsidies thus far offset external price pressures. The broader Asia calendar includes Singapore retail sales, Malaysia industrial production, Taiwan trade, Japan’s current account, and China’s foreign reserves.

Globally, next week’s market focus should be on US services activity and Fed communication after the latest US payrolls. The US ISM services index is due, while the FOMC minutes out on July 9 will be scrutinized for how policymakers are weighing inflation risks, labor-market trends and the path toward the July 29 FOMC meeting, and especially given the big changes in Fed communication strategy from Fed Chair Kevin Warsh. In Europe, investors will monitor ECB communication and guidance including from several speakers and the June account, and this will be important both from a EUR and also Dollar perspective.

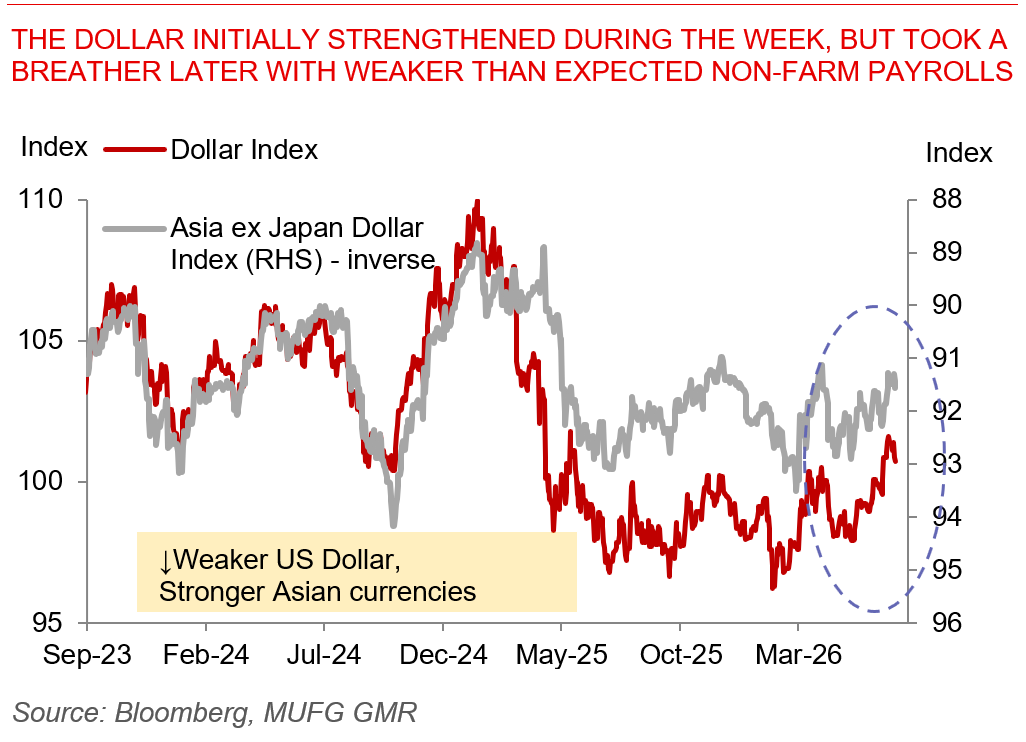

The Dollar initially strengthened during the week, but took a breather later with weaker than expected non-farm payrolls