Week Ahead FX outlook:

Key FX views:

Shifting Middle East geopolitics and central bank signals remained the key drivers of Asia FX this week. Early optimism around a potential US–Iran de escalation briefly lifted risk appetite and supported most Asian currencies, but this quickly faded as renewed US–Iran tensions and the naval blockade in the Strait of Hormuz revived safe haven demand for the US dollar, putting renewed pressure on the region. The Taiwan dollar was the best performer, supported by resilient tech export momentum, strong equity market performance, and expectations that the domestic central bank will maintain a relatively hawkish stance. In contrast, high beta EM currencies underperformed, particularly those with greater exposure to Middle East–driven energy shocks, such as the Philippine peso and the Korean won. The BSP’s rate hike this week provided limited support, as the peso’s weakness reflected market concerns over the growth impact of a series of modest rate hikes ahead signalled by the BSP chief. The yen also lagged after the BOJ pushed back against near term rate hike expectations. The yuan weakened modestly, with the PBOC tolerating depreciation amid broad USD strength. Overall, Asia FX ended the week mixed, caught between short lived risk on bursts driven by geopolitical optimism and renewed US dollar support as tensions resurfaced.

Next week, Asia FX will face a heavy policy and macro calendar. Key events include the Bank of Japan meeting (Apr 27–28), with markets watching closely for any guidance on the pace of policy normalization amid persistent yen weakness, and the FOMC decision (Apr 29), where the USD outlook will hinge on whether the Fed reiterates a “higher for longer” stance. In Asia, attention will turn to China’s monthly data—covering industrial profits, PMIs and the LPR fixing—which will help gauge the impact of the Iran war on China’s economy and shape policy expectations and the CNY outlook. Singapore’s inflation data, following MAS’s recent tightening, will also be watched for signals of imported inflation pressure. Alongside regional PMIs, developments in Middle East tensions will remain a key swing factor, leaving Asia FX sensitive to both policy signals and energy driven terms of trade shocks.

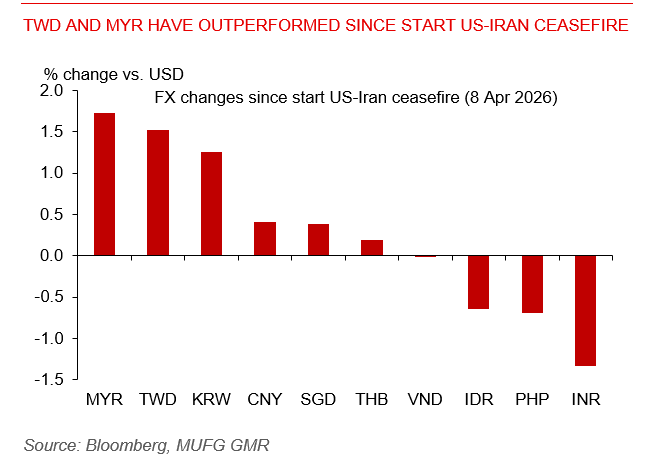

TWD and MYR have outperformed since start US-Iran ceasefire