Week Ahead FX outlook:

Key FX views:

The week ahead is a pivotal one for FX markets, with a flurry of central bank meetings across the US, Japan, and key Asian economies set to reinforce a “higher-for-longer” global rates backdrop. The combination of firmer US inflation and resilient labour market conditions should support the US dollar, while driving greater differentiation within Asia FX amid geopolitical risks in the Middle East.

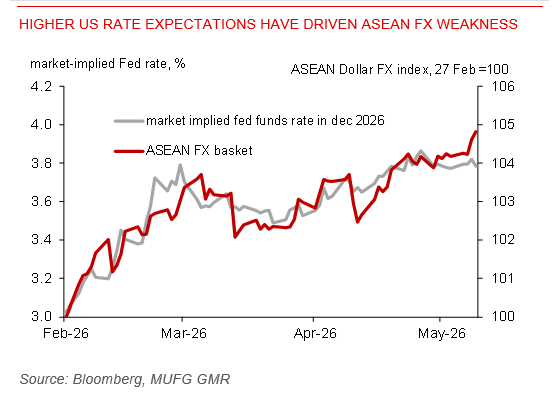

While US retail gasoline prices have eased modestly, they remain elevated relative to pre-conflict levels, continuing to feed through into inflation. With US headline CPI rising above 4%yoy and 1-year inflation expectations firming further, the risk of second-round effects is increasing, limiting the Fed’s scope to ease. US 2-year yields held above 4%, with higher US rate expectations driving recent Asian FX weakness. The upcoming FOMC meeting will be critical, not for policy change - we expect the Fed to remain on hold - but for forward guidance. In particular, markets will closely watch new Fed Chair Kevin Warsh’s communication, which will be crucial in shaping USD direction and, by extension, the outlook for Asian currencies.

In Japan, the Bank of Japan is widely expected to deliver a 25bp rate hike to 1%. However, with this move largely priced in, the yen’s reaction is likely to hinge on forward guidance rather than the hike itself.

Across ASEAN, the policy bias for Bank Indonesia remains tilted towards further tightening to support the rupiah, although the timing of any additional hike - particularly coming soon after the recent off-cycle 25bp move - remains uncertain in our view. For now, spot USDIDR has eased back below the 18,000 level, though near-term volatility continues to rise, suggesting that external pressures remain elevated and could keep BI on a tightening footing next week. In the Philippines, the policy bias is also toward further tightening, as the BSP seeks to counter inflation pressures and support the peso. Elsewhere, Taiwan’s central bank is likely to remain on hold. While the economy continues to benefit from a strong global electronics cycle, inflation currently at around 2.2%yoy and gradually firming points to a potential hawkish hold.

Higher US rate expectations have driven ASEAN FX weakness