Week Ahead FX outlook:

Key FX views:

The week ahead will be pivotal for global FX markets, with the focus firmly on whether US inflation will be softer than market expectation, which could in turn challenge the market's current pricing for higher fed funds rate.

The key event risk remains US CPI inflation on 14 July. A softer inflation outcome could trigger a retracement lower in US yields and provide room for a rebound in selective Asian currencies. However, unless US inflation slows materially enough to shift Fed expectations, any Asia FX rally may still prove short-lived. Conversely, another upside inflation surprise would likely reinforce the market's bullish USD bias and keep pressure on most regional currencies.

The second major catalyst will be China's June activity data and Q2 GDP. Markets are expecting growth to slow to 4.5%yoy from 5% in Q1, with continued weakness in domestic demand offset only partly by exports. For investors, China remains the most important driver of regional growth sentiment. A weaker-than-expected GDP print would likely strengthen the case for maintaining defensive positioning in Asia FX, particularly against currencies most exposed to China demand.

Among regional currencies, KRW could be one of the more interesting opportunities. The combination of a potentially hawkish BoK, continued strength in the semiconductor cycle, and already-depressed KRW valuations provides scope for outperformance if US inflation undershoots expectations.

For SGD, Singapore's Q2 GDP and NODX data should continue reinforcing the narrative of a strong electronics cycle. Strong growth data would be consistent with Singapore's relatively resilient economy and could support SGD on a relative basis within ASEAN FX.

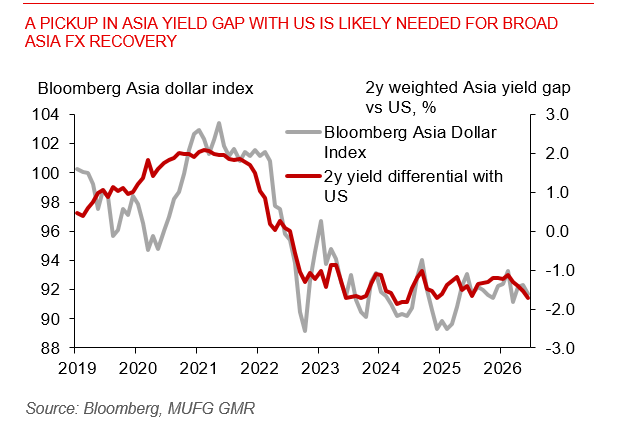

For a broad sustained Asia FX recovery, we believe this would likely still require a combination of softer US inflation and a meaningful decline in US Treasury yields.

A pickup in Asia yield gap with US is likely needed for broad Asia FX recovery