Week Ahead FX outlook:

Key FX views:

Next week’s Asia calendar remains data-heavy, with the focus shifting from PMIs toward hard activity and inflation prints. China will dominate early in the week with CPI, PPI and trade data, following earlier PMI releases – these data points may help to provide a clearer read on whether growth momentum remains export‑led while domestic demand stays soft. Export resilience—especially in tech and manufacturing—remains critical for regional spillovers, with South Korea and Taiwan trade data acting as high-frequency proxies for the global tech cycle. Next week’s South Korea’s June exports 10 days yoy and Taiwan’s May exports likely remain strong. At the same time, inflation releases across China and India will be closely watched for signs that higher energy costs are feeding through more materially into various prices including CPIs. We expect a moderate pick up in India’s May CPI inflations, and a slight edge-up for CPI inflation of China. China’s May PPI inflation however likely delivers a noticeable jump to close to 4%yoy.

On the policy front, the Reserve Bank of India decision will be the key anchor early in the week. Today’s RBI keeping the policy repo rate unchanged at 5.25% and maintaining a neutral stance, signaling a wait‑and‑see approach amid elevated global uncertainty and inflation risks. Overall, the message is a cautious “holding pattern”: inflation pressures are building but still manageable, so the RBI prefers to stay on hold for now while keeping future policy data-dependent and flexible. Beyond India, attention will increasingly turn to how incoming inflation data could shape expectations for upcoming meetings in the Philippines, Taiwan, Indonesia and Korea. In particular, any upside surprises in CPI across Asian economies would reinforce the narrative that central banks may need to lean more hawkish to anchor inflation expectations, especially in economies with weaker FX and higher oil import dependence.

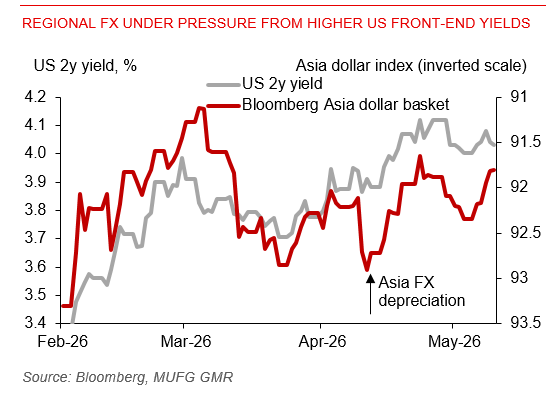

For Asia FX, the near-term outlook remains characterized by divergence rather than a uniform trend, despite still-firm US yields and likely still-firm US dollar. Elevated oil price likely continues to pressure on currencies of those more externally exposed Asia’s net oil importers likely South Korea, Philippines and Thailand. The key for next week is whether inflation surprises shift rate expectations sufficiently to trigger sharper FX moves—particularly in high-beta currencies.

Regional FX under pressure from higher US front-end yields