Ahead Today

G3: Eurozone CPI

Asia: Bank Indonesia policy meeting, Malaysia Trade, China Loan Prime Rate

Market Highlights

The dominant macro driver across Asian markets is the ongoing Iran conflict and Strait of Hormuz closure, which kept oil prices elevated, coupled with risk-off mood across EM currencies amidst rising global yields. President Trump confirmed he called off a planned strike on Iran following appeals from Gulf allies, providing some intraday relief to oil, although NATO is reportedly considering a Hormuz deployment if the waterway remains closed by early July. In Japan, USD/JPY probed 159 for a seventh session, with Finance Minister Katayama reiterating readiness to take "bold action" on FX at the G-7 in Paris, and BOJ Governor Ueda acknowledging long-term yields are "rising quickly." Japan's Q1 GDP came in at +2.1% annualised, above the 1.7% consensus, reinforcing the case for further BOJ tightening. The South Korean won fell 1% to 1,509 per dollar on 19 May — its weakest since 7 April — on foreign equity outflows from chip stocks. In China, bond markets were a relative bright spot, with 10-year futures rising to their highest since July 2025 and the 10-year yield dipping 1 bp to 1.74% on ample liquidity.

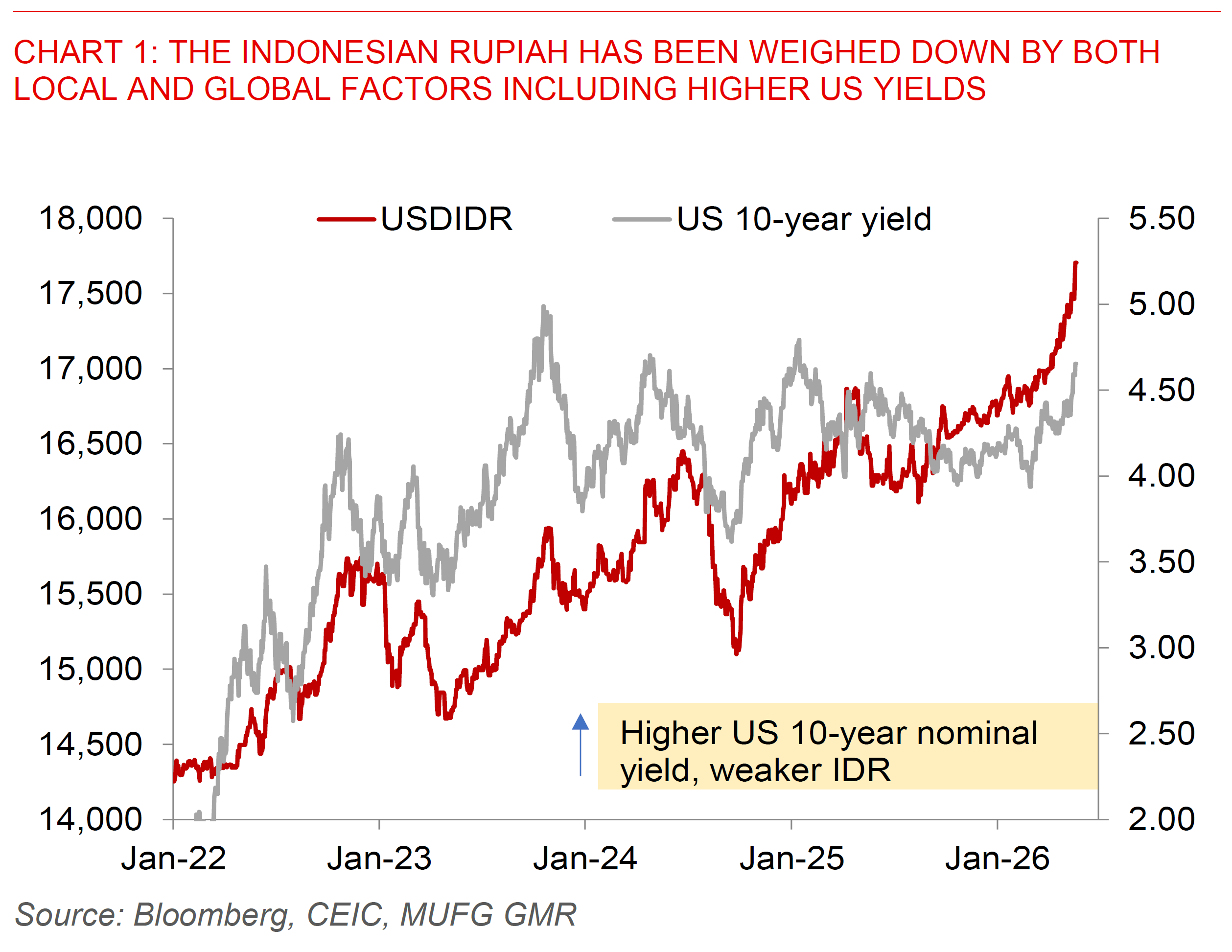

Indonesia coupled with the likes of oil importers such as India and the Philippines sit at the centre of regional stress. The rupiah touched a fresh record low of 17,705 per dollar on 19 May — down over 5% year-to-date — while the Jakarta Composite Index fell 3.5% to 6,371, extending its year-to-date loss to more than 26%. The 10-year government bond yield stands at 6.75%. The pressure reflects accelerating portfolio outflows, and weaker perceived investor confidence in the policy direction under President Prabowo. The government has responded with a daily IDR 2 trillion bond buyback programme active since 12 May, and launched a $2–3 billion global bond offering in dollars and euros on 19 May. What moved markets was also news reports that Indonesia plans to create a new state entity — supervised by sovereign wealth fund Danantara — to centralise control over commodity exports including coal, palm oil, nickel, tin, and copper, ostensibly to curb under-invoicing and capture more export dollar receipts. Markets reacted negatively, with energy and materials stocks leading the JCI decline and nickel spiking on the LME.

The Bank Indonesia rate decision is the pivotal event for today, 20 May. A slim majority of economists expect a 25 bps hike to 5.00%, which would end a pause in place since September 2025, though the outcome is quite close. The case for a hike rests on rupiah defence as a core BI mandate. BI Governor Warjiyo has signalled caution on aggressive intervention, preferring to raise SRBI yields — the 12-month rate now at 6.45% — to attract foreign capital. Indonesia's April budget data showed a deficit of 0.64% of GDP, with tax revenue up 16.1% year-on-year, providing some fiscal headroom. The accompanying statement's tone on further tightening and currency defence will be as important as the decision itself. Elsewhere today, China's LPR fixing is expected to be held steady, and Japan's 20-year JGB auction is a key test of demand given the ongoing super-long selloff. Any further developments on the Hormuz situation remain the primary tail risk for the session.