Ahead Today

G3: US ISM Services

Asia: Thailand CPI, Singapore Retail Sales

Market Highlights

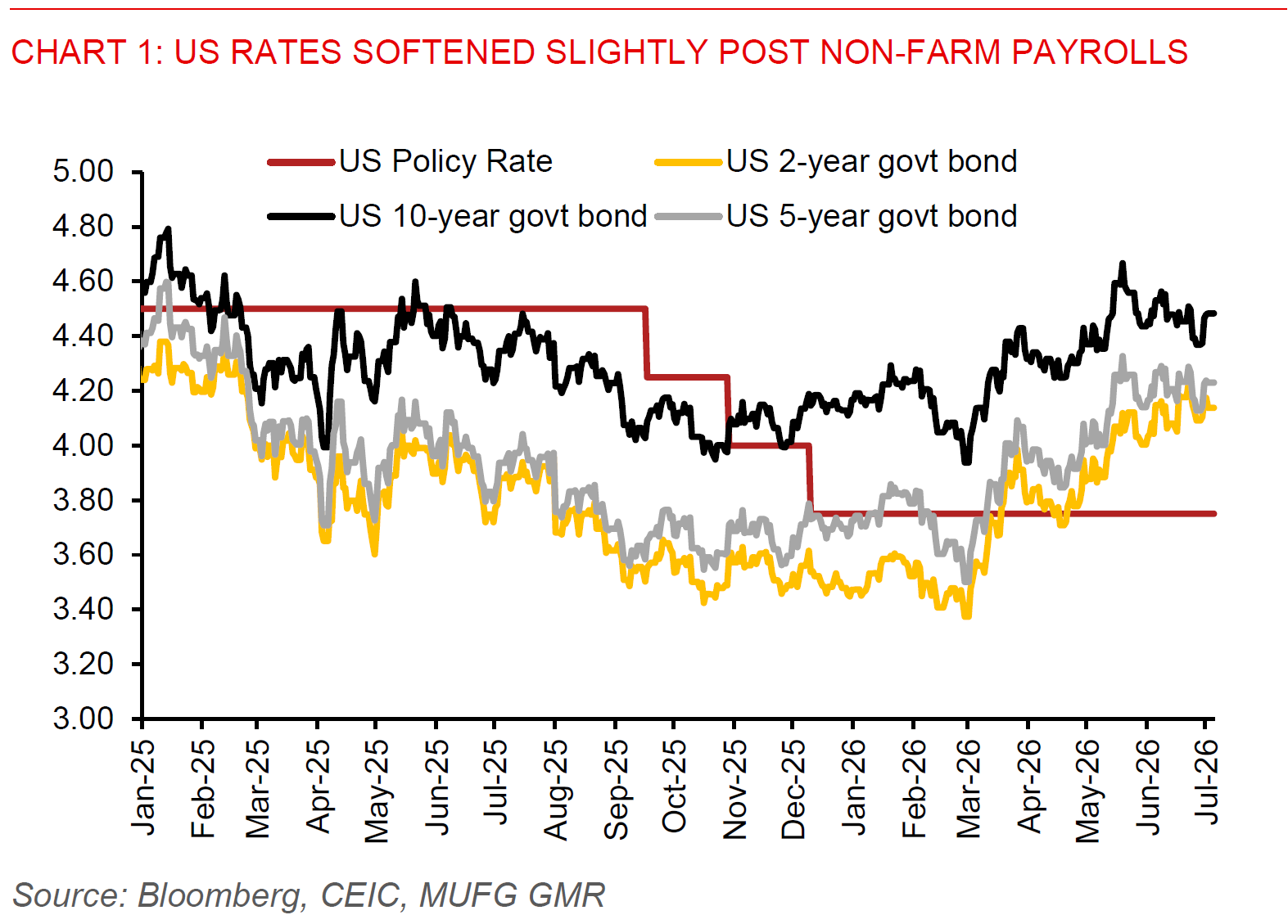

Markets are somewhat in a holding pattern, waiting for the next catalyst for the US Dollar, US rates, while also increasingly buffeted and driven by local Asia factors as well. On the global side, we saw some gradual grind lower in the US Dollar on the back of a follow-through from the softer non-farm payrolls print. There are also key questions around whether Japanese authorities intervened in the FX markets last week to cap JPY weakness, and as such the risk for USD/JPY as it continues to hover around the 162 levels.

Moving forward, global markets will take their cue from key datapoints such as the US ISM Services data and also the FOMC Minutes later this week, coupled with US CPI next week. While the FOMC Minutes are typically not entirely market moving, this time might be different given the fact that we have a new Fed Chair in Kevin Warsh, and with that whether there are any hints around the way he thinks together with the views of the collective FOMC Committee at this point in time. On our end, we think that market pricing for US rates are probably too elevated right now, and as such, if macro data validates there is probably space for US rates to move modestly lower over time.

For Asia, increasingly local factors are also playing a role resulting in divergence across FX pairs. This week, we will have some key inflation data prints, including the likes of China, Thailand, Philippines and Taiwan. In China’s case, markets are looking to see if the recent momentum in nominal growth can continue, even if part of the price increases are driven by supply side factors such as energy prices. For Thailand and Taiwan, we think the prints will for now validate decisions by both central banks to keep rates on hold which will continue to anchor the front-end of the rates curve in both markets. Meanwhile, we think inflation in the Philippines will likely remain elevated at more than 6%yoy, and with risks of El Nino and food price pressures moving forward, we see the BSP remaining hawkish for now. We are forecasting BSP to hike rates two times more, bringing the policy rate to 5.25% by the end of 2026, which should over time provide some support for the currency.