Ahead Today

G3: US PCE inflation, initial jobless claims, durable goods orders, personal spending; Japan leading index

Asia: Thailand and HK trade data

Market Highlights

US PCE inflation for May is likely to remain elevated, although it is also likely approaching a peak as the recent sharp decline in oil prices begins to feed through. That said, the pass-through to US gasoline prices has been slower, suggesting that any moderation in inflation could be slow rather than abrupt. Even if gasoline prices were to normalize back to pre-conflict levels, PCE inflation is likely to remain sticky and above the Fed’s target. Near-term US rate cuts remain unlikely.

At the same time, US labour market conditions continue to hold up, with improving nonfarm payrolls in recent months. This resilience should reinforce the Fed’s patient stance and keep front-end yields elevated. Meanwhile, Fed Chair Kevin Warsh’s decision to step back from the dot plot could keep term premia elevated. With the US 2-year yield still above 4% and the 10-year around 4.4%, the rate backdrop continues to support carry demand for the dollar.

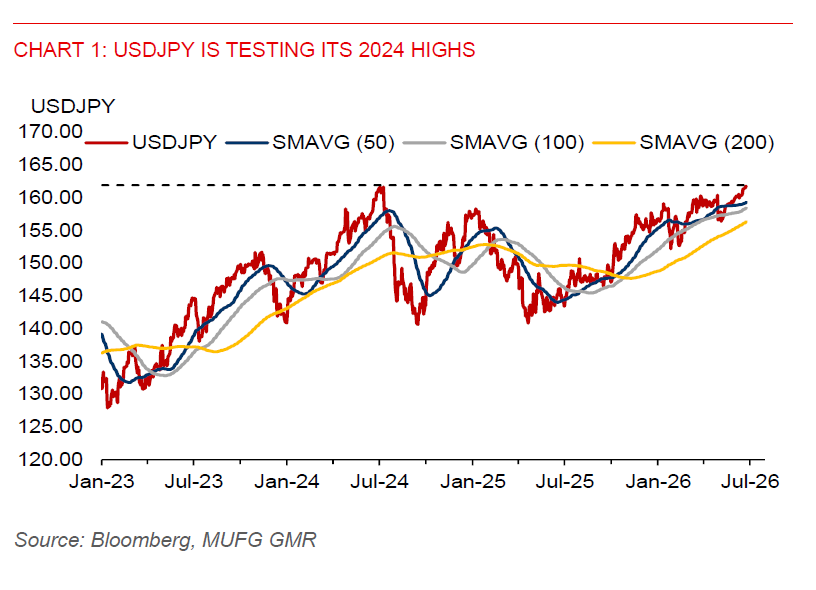

Against this backdrop, USDJPY is trading near its 2024 highs. However, given the elevated risk of policy support for the yen at current levels, participation in further upside in USDJPY is perhaps best approached with downside protection.

Asia FX has come under broad-based pressure against the US dollar, with several ASEAN currencies leading losses since last week’s FOMC meeting. A high-for-longer US rates environment is likely to remain a near-term headwind for regional currencies, particularly lower-yielding ones.

We maintain a near-term negative bias on the baht. The Bank of Thailand kept its policy rate unchanged at 1% yesterday, in line with expectations. While policymakers now anticipate firmer growth this year, concerns remain that growth is still low and uneven. Credit growth has been subdued, and loan asset quality in the SME segment has deteriorated. Thailand’s relatively low yield profile, coupled with easing inflation pressures amid lower oil prices, should allow the central bank to maintain an accommodative, growth-supportive stance. However, elevated US yields will weigh on portfolio flows, with net foreign outflows from Thailand in June following inflows in May, despite the relief from lower oil prices. This shift in flows represents an additional headwind for the baht.