Ahead Today

G3: US CPI

Asia: China CPI and PPI

Market Highlights

A key focus today is the upcoming US CPI print, where inflation could rise above 4.0%yoy in May vs. 3.8%yoy in April. A hot inflation print would reinforce “higher-for-longer” US rate expectations, supporting broad USD strength, particularly with the US–Iran conflict showing no signs of a swift resolution.

Middle East tensions remain front and centre, weighing on global risk sentiment. US equities have come under renewed pressure, while safe-haven demand continues to anchor DXY near the 100.00 level. While our base case still assumes eventual geopolitical de-escalation, the timing remains highly uncertain. Diplomatic efforts between the US and Iran have yet to deliver meaningful progress. At the same time, shipping activity through the Strait of Hormuz remains subdued, reinforcing concerns over sustained disruptions to global energy flows.

This is increasingly feeding through into macro fundamentals in the Asia region. Trade balances are deteriorating most visibly among net oil importers such as Thailand, the Philippines, and Indonesia. In contrast, Malaysia, being a net gas exporter, has seen rising trade surplus, while it also benefits from resilient electronics exports.

Several Asian currencies have remained under pressure against a firm dollar, including the Indonesian rupiah. Notably, however, the rupiah led regional gains yesterday, following further policy action by the central bank to support the currency.

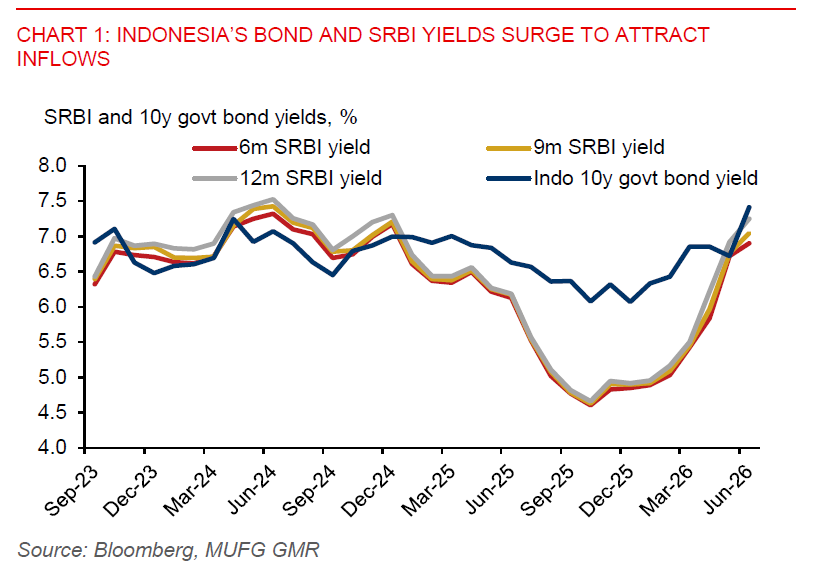

Bank Indonesia raised its policy rate by 25bps to 5.50% in an off cycle move and introduced several accompanying FX stabilisation measures, including higher SRBI yields, holding SRBI auction twice weekly, and a 10% reduction in hedging swap rates for foreign investors. This signals a stronger focus on supporting the rupiah amid rising external pressures and tight dollar liquidity. Despite headline inflation remaining contained for now, rising energy price risks and a closing output gap point to a continued policy tightening bias in our view, with another 25bps BI hike likely by Q3.

Policy support, including improved nominal carry and a 10% reduction in hedging swap rates, could help attract foreign participation in IDR assets and cushion near-term rupiah weakness, particularly as Indonesia’s 10y government bond yields return to fair value. However, persistent headwinds from elevated US yields, Middle East tensions, tight USD liquidity, and weakening external buffers are likely to constrain rupiah’s recovery. Our modelling suggests near-term support range for USDIDR around 17,500–17,800, broadly consistent with our end-Q2 forecast of 17,650, which is conditional on geopolitical de-escalation. However, with Middle East tensions flaring up again, the risk is that the conflict drags into Q3, with USDIDR trending modestly higher back toward 18,200. Near-term event risks include the 18 June FOMC meeting and the upcoming MSCI review of Indonesian equities.