Ahead Today

G3: University of Michigan sentiment index, ECB 1y CPI expectation

Asia: Singapore industrial production

Market Highlights

US macro data continues to reinforce a “high-for-longer” US rates environment. US PCE inflation rose to 4.1%yoy in May (from 3.8%yoy in April), with core PCE at 3.4%yoy (from 3.3%), both in line with expectations. Sequentially, headline and core PCE prints remained firm at 0.4%mom and 0.3%mom, respectively. At the same time, growth indicators point to continued resilience in the US economy, with Q1 GDP revised higher to 2.1%, from 1.6% previously, personal income and spending both rising 0.7%mom in May, and initial jobless claims easing to 215k. Together, the data mix suggests a resilient growth backdrop alongside sticky inflation, likely reinforcing the Fed’s cautious stance on easing. Market pricing for the fed funds rate was little changed, with Fed funds futures still pricing one Fed rate hike around October.

That said, US yields edged slightly lower, with the 2-year at 4.12% and the 10-year at 4.39%, while the DXY softened modestly. Nonetheless, the underlying structural support for the dollar remains intact, despite a somewhat softer DXY yesterday.

In FX, USDJPY remains a key focal point, hovering near 162 and close to its 2024 highs, where the risk of policy intervention from Japanese authorities is elevated. A sustained break higher would likely generate broader negative spillovers across Asia FX via sentiment and positioning channels.

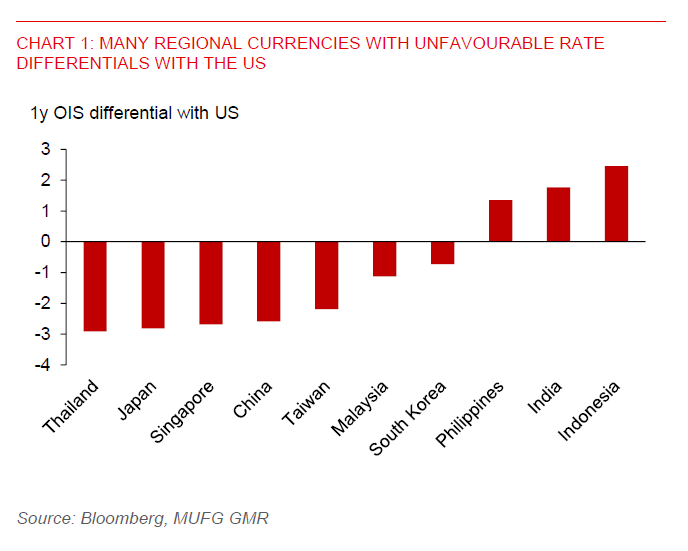

More broadly, the combination of strong US data and delayed Fed easing continues to underpin the dollar through favourable rate differentials. Most Asian currencies still face relatively lower, and in some cases widening, yield differentials versus the US, limiting scope for sustained appreciation. Capital flow dynamics under a high-for-longer US rate environment could be a key factor shaping Asia FX performance.

Against this backdrop, the Malaysian ringgit stands out yesterday, strengthening by 0.4% against the US dollar. This was likely supported by Bank Negara Malaysia’s reintroduction of a 2024-style FX support measure encouraging the repatriation and conversion of offshore earnings by government-linked corporates. USDMYR has retraced from around 4.15 level, possibly indicating early traction from the policy move. However, the sustainability of gains is likely to be more contained compared to the 2024 episode, given the different macro backdrop. Unlike earlier periods when markets were pricing Fed easing, current conditions are characterized by expectations of further rate tightening, which could continue to exert external pressure on the currency. As such, while policy support should help stabilize the ringgit in the near term, the scope for sharp appreciation appears limited.